更令人瞩目的是其"暴利公式":每加息25个基点,将持续带来每年1000亿日元的增量收益。这一逻辑同样适用于三菱日联与瑞穗金融两大巨头,三大行合计占据日本银行总资产半壁江山,其利润飙升幅度可见一斑。

更令人瞩目的是其"暴利公式":每加息25个基点,将持续带来每年1000亿日元的增量收益。这一逻辑同样适用于三菱日联与瑞穗金融两大巨头,三大行合计占据日本银行总资产半壁江山,其利润飙升幅度可见一斑。

In March of last year, the Governor of the Bank of Japan, Kazuo Ueda, pressed the button to end the global era of negative interest rates, initiating the most controversial monetary policy shift in Japan's financial history.

According to Zhitong Finance APP, last March, the Governor of the Bank of Japan, Kazuo Ueda, pressed the button to end the era of negative interest rates globally, initiating the most controversial monetary policy shift in Japan's financial history. A year later, this experiment is revealing a stark economic contrast—Financial Institutions are reaping huge profits, while ordinary families and small to medium enterprises are struggling to survive amid inflation and rising borrowing costs.

The latest Earnings Reports from Sumitomo Mitsui Financial Group act as a mirror, reflecting the direct beneficiaries of the Bank of Japan's interest rate hike policy. Data shows that by the end of this fiscal year (March 2024), the bank gained an additional 90 billion yen (approximately 0.605 billion USD) in interest income solely due to the central bank's interest rate hike.

Even more striking is its "profit formula": for every 25 basis points increase in interest rates, an additional 100 billion yen in incremental revenue will be generated annually. This logic also applies to the two giants, Mitsubishi UFJ and Mizuho Financial, and the three major banks together account for half of the total Assets of Banks in Japan, with their profit surge being quite evident.

Even more striking is its "profit formula": for every 25 basis points increase in interest rates, an additional 100 billion yen in incremental revenue will be generated annually. This logic also applies to the two giants, Mitsubishi UFJ and Mizuho Financial, and the three major banks together account for half of the total Assets of Banks in Japan, with their profit surge being quite evident.

Figure 1

The Capital Markets are staging a more intuitive wealth game. Over the past 12 months, the Japan Bank Stock Index has surged by 29% against the trend, while the TSE Index has only maintained a sideways movement. Behind this unusual strength is the market's frenzied pursuit of the "interest rate spread dividend."

While the central bank maintains a savings interest rate of 0.2%, the three major banks transfer funding costs to businesses and individuals through floating rate loans (which account for over 75%), resulting in a spread differential of up to 3 percentage points.

Behind the financial frenzy lies the chilling reality of the real economy. The account book of 50-year-old Tokyo employee Masashi Fujii is highly representative: "Food prices have risen by 15%, but the wage increase is less than 5%. The rise in mortgage rates has increased monthly repayments by 0.02 million yen." This "wage-price" differential is tearing apart the foundation of consumer spending, with data from January showing that real wages have shrunk by 1.8% year-on-year, and the wave of food price increases in April will further squeeze household spending.

Companies are also facing increased pressure. Shigeru Nozawa, president of a metal fabrication plant in Saitama Prefecture, acknowledges: "Businesses without loans do not benefit from interest rate advantages, yet they must endure the dual squeeze of cost transfer." In 2024, the number of bankruptcies among Japanese companies will exceed 5,000, a ten-year high, with nearly 40% being small and medium-sized enterprises with debts exceeding 1 billion yen.

More seriously, the central bank's interest rate hikes have pushed the yield on 10-year government bonds to 1.7%, exacerbating the snowball effect of government debt—over the next four years, interest payments alone will surge by 25%, swallowing nearly 230 billion dollars from the fiscal budget.

Figure 2

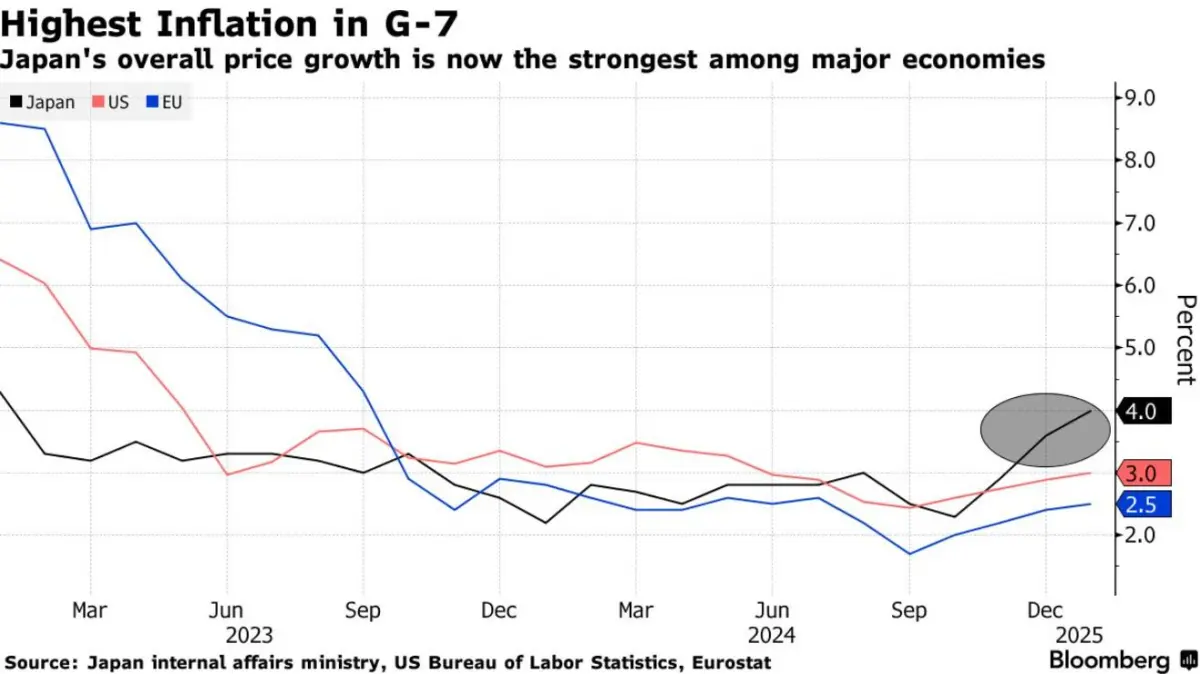

Figure 3 compares the inflation trends of Japan, the USA, and the EU from March 2023 to December 2025, revealing that during the central bank's interest rate hike cycle, Japan's inflation rate significantly soared, consistently operating at high levels after breaking 7% in mid-2023, ultimately surpassing other major economies to become the inflation benchmark among G-7 countries.

Figure 3

Confronted with the pain of people's livelihoods, former Executive Director of the Bank of Japan, Kazuhiro Momose, bluntly stated: "Raising interest rates is like pouring salt on the wounds of low-income groups." This division is turning into political pressure, leading to an 8-percentage-point drop in the support rate for the Shōbō cabinet to 36%. In the upcoming summer House of Councillors election, if the ruling party cannot show effective measures for people's livelihoods, it may repeat last year's defeat in the House of Representatives election.

Monetary policy is also facing a dilemma. Although economists generally expect another interest rate hike in July, Kazuo Ueda must weigh the "ghost of the bubble economy" — the historical lesson of five consecutive interest rate hikes in 1989 that directly burst the asset bubble is still fresh in memory.

More subtly, the yen's exchange rate has rebounded to below the 150 level driven by risk aversion, undermining the last justification for monetary easing.

This interest rate revolution, which began in the Bank of Japan's building, is reshaping the genetic sequence of the Japanese economy. While financial capital revels in the interest rate spread game, the real economy struggles in the chain of cost transfer. This imbalance will ultimately test the wisdom of Japanese policymakers: can a third path be found between controlling inflation and maintaining people's livelihoods? The answer may lie in the direction of policies this summer.

Comment(0)

Reason For Report