市场波动性并未急剧飙升——芝加哥期权交易所波动率指数(VIX指数)在股票持续下跌的情况下,稳步攀升至近30,随后又有所回落。虽然其盘中波动吸引了日内交易员,但标普500指数的看跌期权偏度趋于平缓,VIX指数的看涨期权与看跌期权比率下降。这些迹象表明,

市场波动性并未急剧飙升——芝加哥期权交易所波动率指数(VIX指数)在股票持续下跌的情况下,稳步攀升至近30,随后又有所回落。虽然其盘中波动吸引了日内交易员,但标普500指数的看跌期权偏度趋于平缓,VIX指数的看涨期权与看跌期权比率下降。这些迹象表明,

The experience left by past stock market crashes for investors is that a lack of liquidity can exacerbate market volatility.

Last week, the S&P 500 Index entered a correction Range, but a notable feature of this round of sell-off is its relative calmness. Now, while investors are carefully examining market sentiment Indicators and key price levels to find clues about the next direction of the market, they also need to pay attention to a more elusive aspect: market liquidity.

From the stock market crash in 1987 to the market crisis during the COVID-19 pandemic, they all share a common theme: liquidity exhaustion exacerbating market volatility. Today, with the rapid development of derivatives, there is a growing focus on how Options Positions affect the symbol's spot market, especially considering the scenarios in which derivative crises tend to come to mind.

Market volatility has not surged sharply—the Cboe Global Markets Volatility Index (VIX Index) has steadily climbed to nearly 30 amid continuous declines in Stocks, before retreating slightly. Although its intraday fluctuations attract day traders, the skew of S&P 500 Index Put Options has flattened, and the ratio of Call Options to Put Options of the VIX Index has declined. These signs indicate that part of the decline in Stocks is due to investors cashing out by selling Stocks and hedging related Options.

Market volatility has not surged sharply—the Cboe Global Markets Volatility Index (VIX Index) has steadily climbed to nearly 30 amid continuous declines in Stocks, before retreating slightly. Although its intraday fluctuations attract day traders, the skew of S&P 500 Index Put Options has flattened, and the ratio of Call Options to Put Options of the VIX Index has declined. These signs indicate that part of the decline in Stocks is due to investors cashing out by selling Stocks and hedging related Options.

The ratio of open VIX Call Options to Put Options has decreased.

While traders may sometimes increase the volatility of the market with hedging operations in reaction to the negative Gamma from selling Options short positions, there is currently no large amount of commentary suggesting that Options Trading has a significant impact on the market. According to a measure of market depth by the Chicago Federal Reserve and the CME Group Inc., this is largely attributed to market liquidity, which has remained stable overall.

Benedicte Lowe, a stock derivative strategist at BNP Paribas, and Georges Debbas, the head of European stock derivatives strategy, stated: "For the symbol's spot market, liquidity is clearly key to absorbing the cash flows generated by the Options Greeks. The primary risk is that when traders' negative Gamma positions increase significantly and liquidity is exhausted, you will see spot prices overshooting dramatically."

Note: The Greeks of Options are indicators used to measure the sensitivity of Options prices to various factors, mainly including Delta, Gamma, Theta, Vega, and Rho.

The decline of the S&P 500 Index mainly occurs during regular trading hours with high liquidity. Moreover, the fluctuations of the index are not driven by any shocking data or announcements but by a series of ongoing tariff statements and trade threat remarks, many of which are retracted within hours.

Investors should pay attention to the Hold Positions of dealers on S&P 500 Index derivatives, but under normal market conditions, the trading volume of near-month Futures contracts linked to the index reaches 500 billion dollars, and the size of the spot market and the trading-open-end Funds (ETF) is substantial enough to absorb the Inflow of hedging funds. The daily non-Delta adjusted nominal Options trading volume for the S&P 500 Index exceeds 2 trillion dollars.

Joe Tigay, portfolio manager of Rational Equity Armor Fund and Catalyst Hedged Equity Fund, stated: "The market is not solely determined by the Hold Positions of dealers—these dynamic factors are just part of a larger puzzle. On some days, they are nearly imperceptible; on others, they may turn a standard pullback into a full-blown crash."

Recent significant volatility in U.S. stocks—triggered either by DeepSeek related news or by drastic fluctuations of the dollar against the yen—started during periods of low liquidity. In a highly risk-averse environment, when market makers withdraw buy and sell orders, smaller Orders can dramatically increase their impact on the market, at least causing intraday price distortions.

An example of the DeepSeek storm: Pre-market trading volume surged along with significant market selling, and the subsequent rebound was equally sharp, indicating that the market was influenced by large transaction orders.

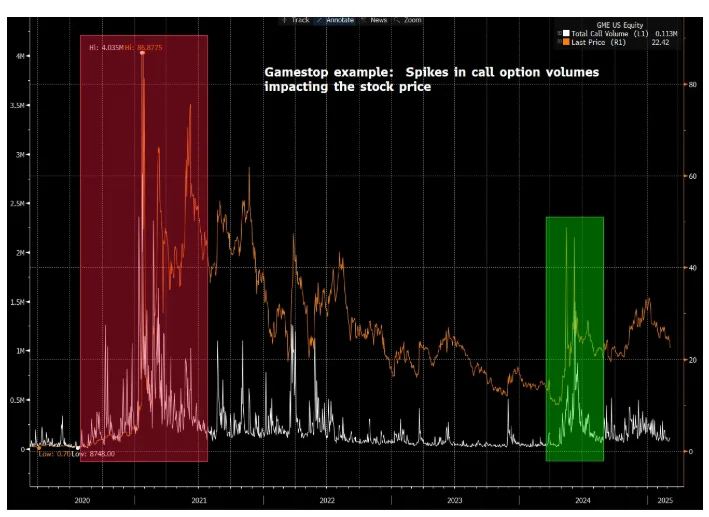

The biggest impact of Options Trading on the stock market may be reflected in individual stocks rather than the Large Cap index, because the overall trading volume in individual stocks is smaller, and when dealers close positions, unilateral Options trading may drive stock price fluctuations. The event of GameStop in 2021 may be one of the most striking cases when the Options Hold Positions seemingly triggered a short squeeze on the underlying stock.

The example of GameStop: The surge in Call Options trading volume impacted the price movements of GameStop shares.

Market makers in the Nordic region sometimes find themselves caught up in large, illiquid customer trades; it is reported that in such cases, the Options trading flow can sometimes drive price fluctuations of the underlying stocks.

One of the most anticipated events on the derivatives calendar is the quarterly Options expiration date, known as 'Triple Witching Day.' Although on these days, there will be options contracts with a notional value reaching trillions of dollars expiring, they rarely have a significant impact apart from brief fluctuations during pricing windows (such as the 10-minute Exchange settlement price window for the Euro Stoxx 50 Index).

Although independent data providers, major brokers, and bank strategists often reach a consensus on the possible positions of traders, disagreements still arise.

This is not to say that Options Trading cannot affect the Large Cap; situations do arise where 'the tail wags the dog.' In February, the trading volume of zero-day expiration contracts reached a record 56% of the S&P 500 Index Options trading volume, and on some days in March, it was even higher. This scale has grown large enough to make buying investors pay attention in the context of other market signals.

Stefano Amato, senior fund manager at M&G's Multi-Asset Group, stated: 'Today, the scale of this Options Trading activity is significant enough to materially affect the trajectory of major stock indices such as the S&P 500 Index or the Nasdaq Index. We view these dynamic factors as sentiment indicators, combined with the increased Inflow of funds into passive products, which may lead to short-term market overreactions.'

Today, after hitting the high near 24,000 in the early session and entering bearish positions, the index fell sharply by nearly over 600 points, immediately recouping yesterday's losses significantly.

Today, after hitting the high near 24,000 in the early session and entering bearish positions, the index fell sharply by nearly over 600 points, immediately recouping yesterday's losses significantly.

Moreover, today it broke the new high again, reaching a maximum of 24,076, but by the end of the market, it fell back by about 70 points, producing a bearish candle. The current trend has not yet been broken, but from the previous low until now, it has risen close to 6,000 points. It is believed that those with positions can continue to hold until there is a clear trend reversal for profit-taking. Those without positions can wait for a pullback to get in. Actually, it is hoped for a quick pullback, as it allows for entry and also provides a healthy breath.

Moreover, today it broke the new high again, reaching a maximum of 24,076, but by the end of the market, it fell back by about 70 points, producing a bearish candle. The current trend has not yet been broken, but from the previous low until now, it has risen close to 6,000 points. It is believed that those with positions can continue to hold until there is a clear trend reversal for profit-taking. Those without positions can wait for a pullback to get in. Actually, it is hoped for a quick pullback, as it allows for entry and also provides a healthy breath. Currently, the outlook remains the same as before. It is believed that even if there is a pullback, it shouldn't be too deep. However, if Futures fail to stabilize and close below 22,350, there may still be room for decline. The chance of Futures falling below 21,400 in the short term should be low, so it is considered that if a significant pullback occurs, it presents a good opportunity to incrementally go long. Recently, there has been a consistent approach to not hold positions overnight, only focusing on immediate trades, as there is no high chasing and no casual short selling.

Currently, the outlook remains the same as before. It is believed that even if there is a pullback, it shouldn't be too deep. However, if Futures fail to stabilize and close below 22,350, there may still be room for decline. The chance of Futures falling below 21,400 in the short term should be low, so it is considered that if a significant pullback occurs, it presents a good opportunity to incrementally go long. Recently, there has been a consistent approach to not hold positions overnight, only focusing on immediate trades, as there is no high chasing and no casual short selling.

Comment(0)

Reason For Report