瑞穗证券美国公司(Mizuho Securities USA)宏观策略主管多米尼克·康斯塔姆(Dominic Konstam)表示:“鲍威尔需要给出某种信号,表明他们正在关注这一情况。” 他警告称,

瑞穗证券美国公司(Mizuho Securities USA)宏观策略主管多米尼克·康斯塔姆(Dominic Konstam)表示:“鲍威尔需要给出某种信号,表明他们正在关注这一情况。” 他警告称,

In this week's policy meeting, Powell had to convince investors that the USA economy remains solid and robust, while also conveying policymakers' determination to intervene whenever necessary.

This week, Federal Reserve Chairman Powell faces a tricky task of assuring investors that the USA economy is still on a solid growth trajectory while also conveying that policymakers are ready to take action if necessary.

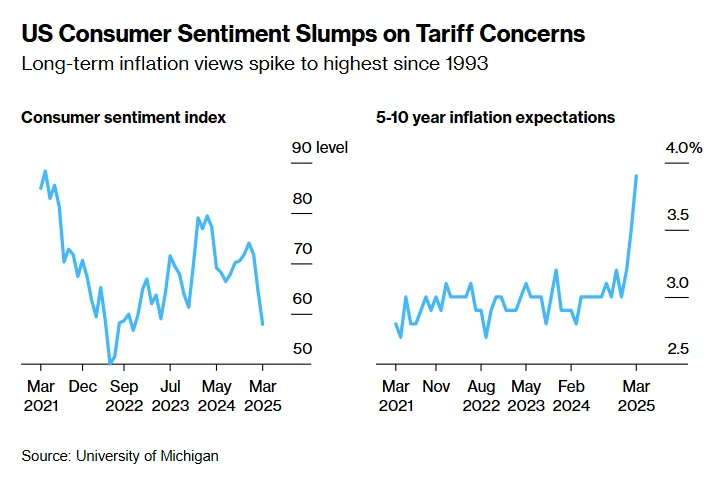

Although this Federal Reserve Chairman has praised the resilience of the USA economy, the rapidly escalating trade war initiated by Trump has raised concerns among investors, leading to a significant decline in the USA stock market over the past month. Bond yields have also decreased, along with a drop in consumer confidence as worries about the economic outlook intensify.

Dominic Konstam, head of macro strategy at Mizuho Securities USA, stated, "Powell needs to give some kind of signal indicating they are monitoring the situation." He warned that while Powell may make it clear that officials are not targeting the stock market, they cannot overlook the recent decline in the stock market.

Dominic Konstam, head of macro strategy at Mizuho Securities USA, stated, "Powell needs to give some kind of signal indicating they are monitoring the situation." He warned that while Powell may make it clear that officials are not targeting the stock market, they cannot overlook the recent decline in the stock market.

The market generally expects the Federal Reserve to maintain interest rates at its meeting on March 18-19; however, traders now believe there is a high probability of three rate cuts this year, most likely starting in June. Economists generally expect two cuts, which roughly aligns with their expectations for the dot plot update from policymakers this week.

Some investors warn that if officials continue to only hint at two rate cuts in 2025, it becomes even more important for Powell to emphasize the central bank's willingness to adjust borrowing costs when issues arise in the labor market.

James Athey, portfolio manager at Marlborough Investment Management, stated: "To some extent, the Federal Reserve's decisions may make the situation slightly better or worse. But it's clear that they can't completely calm the market, as the shock to market sentiment largely comes from the White House."

Apart from the constantly escalating and unpredictable tariff threats to the USA's largest trading partners, the Trump administration has not taken many measures to mitigate the risk of economic recession. On March 9, Trump stated that the USA economy is facing a "transitional period," while his Treasury Secretary Scott Bessent pointed out that both the USA and the market need to "detox."

How will the Federal Reserve respond to market reactions?

The two-year Treasury yield, which is most sensitive to the Federal Reserve's monetary policy, has fallen nearly 60 basis points from its peak in mid-January, reaching a low of 3.83% this month, the lowest level in over five months. Although the stock market rose last Friday, it had previously gone through a round of selling, with the S&P 500 Index plummeting 10% from its peak. The so-called "fear index" on Wall Street, the Cboe Global Markets Volatility Index (VIX), briefly climbed to its highest level since last August last Monday.

The market's tension has heightened the risk of this week's policy meeting, during which officials will release new economic forecasts, which are expected to provide insight into how officials anticipate Trump's policies will impact the economy. Policymakers are expected to slightly lower their growth forecast for this year and raise expectations for core inflation, excluding food and energy prices.

However, Powell may be reluctant to assure investors that the Federal Reserve will act immediately once signs of an economic recession appear, unless there is one key additional condition: officials need to see evidence that inflation is persistently moving towards the 2% target they have set and that inflation expectations remain stable.

Wells Fargo & Co's senior economist Sarah House stated, "We are hearing messages that the situation remains under control and that current policies are in a good position, allowing the Federal Reserve to respond in either direction based on the circumstances—whether addressing stubbornly high inflation or responding to a more apparent economic slowdown. What I would like to hear now is a clearer explanation of how they weigh these two aspects of their responsibilities."

Despite the slowdown in consumer price increases in February, the Producer Price Index remained unchanged from the previous month. However, the components that make up the Federal Reserve's preferred inflation measure—the Personal Consumption Expenditures Price Index—remained largely robust. Previously, a closely watched long-term inflation expectations indicator rose for the third consecutive month, reaching its highest level in over thirty years.

Matthew Luzzetti, the chief economist for Deutsche Bank in the USA, stated that such data limits the Federal Reserve's ability to act and boost the economy before economic weakness is more directly reflected in the labor market—potentially manifesting as sluggish job growth, rising unemployment rates, or a surge in layoffs.

Luzzetti stated, "There is a lot of uncertainty right now that may reflect in actual data, but the Federal Reserve will be in a wait-and-see mode to see if this situation occurs." He predicts that the Federal Reserve will not lower interest rates this year. "Meanwhile, I think they are seeing more evidence that their work on controlling inflation is not yet complete," he said.

A Bloomberg survey revealed that if the Federal Reserve faces economic weakness amid still high inflation, about two-thirds of economists expect officials to maintain borrowing costs unchanged.

Complicating the interest rate outlook are other policies proposed by the Trump administration, such as tax cuts and deregulation, which may boost the economy and inflation in the coming months. Powell and his colleagues emphasize that they are monitoring the "net impact" of Trump’s policies on the economy and hope to have a clearer understanding of their overall effects before adjusting policies.

Earlier this month, Powell stated in his last public speech before the officials' meeting this week: "Despite the high levels of uncertainty, the USA economy is still in good shape. We do not need to rush into action, the policy is in a good position to wait for conditions to become clearer."

Is there a change in the pace of QT?

Wall Street strategists will also closely watch whether the Federal Reserve will give any hints about pausing or further slowing the pace of asset balance sheet reduction, a process referred to as Quantitative Tightening (QT). The minutes from the January meeting indicated that policymakers had discussed the potential necessity of pausing or slowing this process before Congress reaches an agreement on the government debt ceiling.

Blake Gwinn, head of USA interest rate strategy at Royal Bank of Canada Capital Markets, stated: "The rationale for the Federal Reserve to take action in March is that officials have already discussed this issue. So why not just do it directly - because they can pause QT and then restart later."

Editor/jayden

Today, after hitting the high near 24,000 in the early session and entering bearish positions, the index fell sharply by nearly over 600 points, immediately recouping yesterday's losses significantly.

Today, after hitting the high near 24,000 in the early session and entering bearish positions, the index fell sharply by nearly over 600 points, immediately recouping yesterday's losses significantly.

Moreover, today it broke the new high again, reaching a maximum of 24,076, but by the end of the market, it fell back by about 70 points, producing a bearish candle. The current trend has not yet been broken, but from the previous low until now, it has risen close to 6,000 points. It is believed that those with positions can continue to hold until there is a clear trend reversal for profit-taking. Those without positions can wait for a pullback to get in. Actually, it is hoped for a quick pullback, as it allows for entry and also provides a healthy breath.

Moreover, today it broke the new high again, reaching a maximum of 24,076, but by the end of the market, it fell back by about 70 points, producing a bearish candle. The current trend has not yet been broken, but from the previous low until now, it has risen close to 6,000 points. It is believed that those with positions can continue to hold until there is a clear trend reversal for profit-taking. Those without positions can wait for a pullback to get in. Actually, it is hoped for a quick pullback, as it allows for entry and also provides a healthy breath. Currently, the outlook remains the same as before. It is believed that even if there is a pullback, it shouldn't be too deep. However, if Futures fail to stabilize and close below 22,350, there may still be room for decline. The chance of Futures falling below 21,400 in the short term should be low, so it is considered that if a significant pullback occurs, it presents a good opportunity to incrementally go long. Recently, there has been a consistent approach to not hold positions overnight, only focusing on immediate trades, as there is no high chasing and no casual short selling.

Currently, the outlook remains the same as before. It is believed that even if there is a pullback, it shouldn't be too deep. However, if Futures fail to stabilize and close below 22,350, there may still be room for decline. The chance of Futures falling below 21,400 in the short term should be low, so it is considered that if a significant pullback occurs, it presents a good opportunity to incrementally go long. Recently, there has been a consistent approach to not hold positions overnight, only focusing on immediate trades, as there is no high chasing and no casual short selling.

Comment(0)

Reason For Report