不管您是企业家、投资者,还是资本市场的关注者,《IPO直通车》将是您洞悉IPO市场的重要窗口,共同见证资本市场的风云变幻 。

不管您是企业家、投资者,还是资本市场的关注者,《IPO直通车》将是您洞悉IPO市场的重要窗口,共同见证资本市场的风云变幻 。

Spring Future, National Services, Harmony Jinfeng, and RJH Investment are the four institutions that are the first-round investors in Huishuangzhang. Despite Huishuangzhang being crowned as "Industry No. 1", this company, which has been established for nearly ten years, still faces multiple challenges such as a highly fragmented market and an unproven profit model.

Editor’s note: In the waves of the Capital Markets, Initial Public Offerings (IPOs) have always attracted attention as a key milestone in corporate development and a focal point for investors.

Starting from February 28, 2025, Venture Capital Daily will officially launch the "IPO Express" column, where we will dialogue with company founders and angel investors to present a comprehensive view of the ins and outs of IPOs; we will ride the "express train" to delve into companies and attend roadshows, bringing you the latest IPO developments and the most professional interpretations and analyses.

Whether you are an entrepreneur, investor, or a follower of the Capital Markets, the "IPO Express" will be an important window for you to gain insights into the IPO market, witnessing the changing tides of the Capital Markets together.

On March 11, the Star Daily reported (Reporter Chen Mei) that recently, Huishuangzhang Holdings Limited, also known as SATP Holding Inc., submitted a prospectus to the Hong Kong Stock Exchange, intending to list on the Main Board. This is a reapplication following two previous applications that became ineffective on June 30, 2023, and June 14, 2024.

According to disclosures, data from Frost & Sullivan shows that, based on the number of small and micro enterprises directly served in 2023, Huishuangzhang is the largest tax and financial solution provider for small and micro enterprises in China.

However, the Star Daily reporter noted that despite being labeled as "Industry No. 1", this company established nearly ten years ago still faces multiple challenges such as a highly fragmented market and an unproven profit model.

An individual engaged in the accounting industry told the Star Daily reporter that by the end of 2024, the total number of small and medium-sized enterprises in China will exceed 60 million, with more than 60% relying on external tax and financial services. This enormous demand has spawned an accounting market exceeding 200 billion yuan, but the industry's concentration is extremely low.

The prospectus also shows that, as the number one company in the market, Huishuanzhang has a market share of 0.5%. The top five companies combined have a market share of no more than 1%.

The line-up of investors is luxurious.

According to data from Caijing Lianhe, Huishuanzhang has experienced a total of 9 rounds of financing since its establishment, raising over 1.5 billion yuan, with investors including stars like Tencent, Xiaomi, and Sichuan Hexie Shuangma (000935).

In the list of angel round investors, reporters from the Star Daily noticed that Spring Future, National Services, Hexie Jinfeng, and RJH Investment are all participants.

Equity penetration shows that the holders of Spring Future, National Services, and RJH Investment are respectively Wu Xianchun, Zhang Guoxiang, and Zhou Zhibing, all early investors in Huishuanzhang and independent third parties; Hexie Jinfeng is held by Sichuan Hexie, controlled by IDG Capital.

It is worth mentioning that Hexie Jinfeng continued to invest in Huishuanzhang in subsequent rounds—participating in the Pre-A, A+, and B rounds. As of the IPO, Sichuan Hexie held 10.27% of shares through Hexie Jinfeng.

Nevertheless, Sichuan Hexie is not the largest external shareholder of Huishuanzhang. The largest external investor is Gaocheng Capital (GP), founded by Hong Jing, which holds 6.14%, 6.68%, and 4.10% through Shanghai Hongyan, GCHSZ Holdings, and GHSZ Holdings respectively, totaling 16.92%; Xiaomi Software (GP), under Xiaomi Group (01810.HK), holds 14.73% through Shanghai Jiao Zeng, making it the second largest external shareholder.

Reporters from the Star Daily noted that Hong Jing is a seasoned investor. Before founding Gaocheng Capital, Hong Jing worked at several well-known investment institutions, including Hillhouse Capital, General Atlantic LLC in the USA, Warburg Pincus LLC, and McKinsey & Company.

During the Hillhouse period, Hong Jing served as a partner and was responsible for the Private Equity investment business, leading investments in several well-known projects including Meituan, DiDi Global Inc, ZTO Express, and Wind Information.

In addition to the above shareholders, Tencent (00700.HK) also holds 8.62% through Imagery Flag; SUNSHINE INS holds 6.39%; and Yuanhui Capital holds 5.75%, which are important external shareholders of Huishuangzhang.

The founder comes from clinical medicine.

What background does the founder of Huishuangzhang have to attract so many leading institutions?

The prospectus shows that the founder of Huishuangzhang is Zhang Shugang. Compared to other entrepreneurs, Zhang Shugang has a different background.

Zhang Shugang graduated from Qinghai University Medical College, majoring in clinical medicine. However, instead of deeply engaging in the medical field, he chose to enter the financial and tax services industry. Before founding Huishuangzhang, Zhang Shugang served as general manager in multiple business divisions at Fangxin Technology Co., Ltd., and participated in the "Golden Tax Phase III" project of the State Administration of Taxation of China, responsible for drafting relevant standards.

This experience allowed Zhang Shugang to accumulate industry experience and also made him aware of the pain points and needs of small and micro enterprises in financial and tax management. In 2015, Zhang Shugang founded Huishuangzhang, focusing on providing SaaS-based financial and tax solutions for small and micro enterprises.

The prospectus shows that Huishuangzhang provides lower-cost services for small and micro enterprises in financial and tax services. From 2022 to 2024, the delivery human cost per small and micro enterprise client is 888 yuan, 805 yuan, and 738 yuan respectively, while according to Frost & Sullivan's data, the delivery human cost for traditional solution providers is about 2,550 yuan per year.

In terms of market performance, in 2024, the SATP system of Wisdom Accounting served 0.6517 million small and micro enterprises, with a customer retention rate reaching 80.0%.

Reflecting on revenue, from 2022 to 2024, Wisdom Accounting's revenue reached 0.516 billion yuan, 0.539 billion yuan, and 5.51 billion yuan respectively, with a compound annual growth rate of 3.4%. However, in terms of net income, there were losses of 0.506 billion yuan, 0.302 billion yuan, and 1.41 billion yuan during the reporting period.

The reason for this is that Wisdom Accounting disclosed in its prospectus that from 2022 to 2024, the number of customers for its direct sales model based on Saas solutions continuously decreased, reaching 0.2119 million, 0.2112 million, and 201,800 respectively; the corresponding revenue from its Saas solutions also fell, dropping from 0.464 billion yuan in 2023 to 0.459 billion yuan.

Industry professionals interviewed by the Star Daily stated that the sector in which Wisdom Accounting operates shows typical characteristics of a "large industry with small companies." This dispersed pattern arises from the low market entry barriers, with over 0.1 million registered accounting agencies nationwide, resulting in severely homogenized services and fierce price competition.

To address this, Wisdom Accounting has maintained high sales and marketing expenditures from 2022 to 2024. Data shows that during the reporting period, the expenditures were 0.381 billion yuan, 0.303 billion yuan, and 2.74 billion yuan, accounting for 73.8%, 56.2%, and 49.8% of revenue respectively.

As for the proportion of sales personnel, by the end of 2024, Wisdom Accounting had a total of 1,042 employees, with sales personnel accounting for 47.9%; while in 2023, Wisdom Accounting had 1,277 employees, with sales personnel making up 46.5%, which is approximately 594 sales personnel.

Has issued multiple rounds of "redeemable convertible preferred shares."

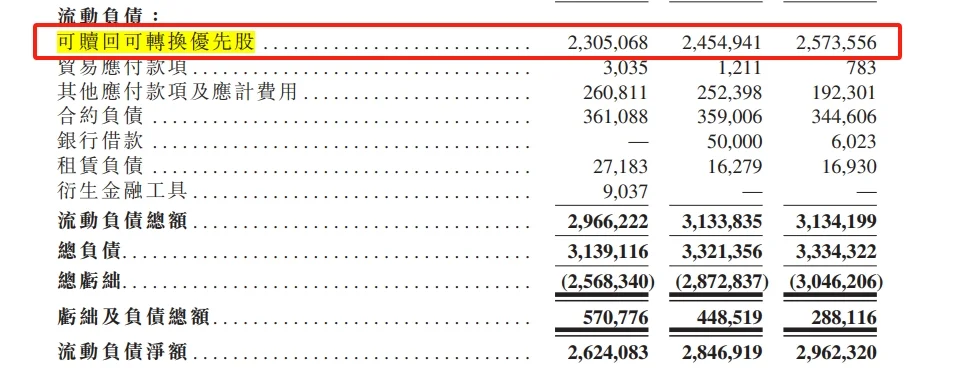

In the past nine rounds of financing, Wisdom Accounting has also issued redeemable convertible preferred shares. The reporter from Star Daily noted that these preferred shares are accounted for as current liabilities.

According to the prospectus, from 2022 to 2024, the amounts of redeemable convertible preferred stocks are 2.305 billion yuan, 2.455 billion yuan, and 2.574 billion yuan respectively, totaling over 7.3 billion yuan. Huishuan Account stated that the increase in the amount of these preferred stocks is mainly due to the valuation increase resulting from the company's revenue growth.

At the same time, according to relevant terms, if Huishuan Account fails to complete a qualified listing within five years after the D round financing in April 2021, investors have the right to request the company to repurchase the stocks. From a timing perspective, Huishuan Account has just over a year left, and the company has already updated its prospectus twice.

It is worth mentioning that Huishuan Account's cash flow from operating activities is also under pressure. From 2022 to 2024, the amounts are -0.216 billion yuan, -0.218 billion yuan, and -0.54 billion yuan respectively. By the end of 2024, the company's operating cash flow is -0.031 billion yuan, with cash at the end of the period around 0.092 billion yuan and short-term contract liabilities of 0.345 billion yuan.

According to the latest prospectus, Huishuan Account stated that the net proceeds from the IPO will primarily be used to expand business, improve market penetration; optimize tax and financial solutions; increase R&D investment to enhance technological capabilities; conduct strategic investments and acquisitions; as well as supplement working capital.

An investor told the Star Daily that Huishuan Account's financing has stagnated since 2021, reflecting the 'cold winter' of capital in the enterprise service sector.

The investor stated that after 2021, the valuation logic for SaaS companies in the primary market shifted from 'scale priority' to 'profit priority', while Huishuan Account has not yet achieved positive cash flow. Although its core SaaS subscription revenue accounts for over 80%, the growth rate of new customers has slowed, further undermining capital confidence.

In addition, changes in the competitive landscape of the industry have intensified financing difficulties. Traditional accounting firms are accelerating digital transformation, giants like Kingdee are seizing the market through B2B2C models, and new entrants are competing for customers with low-price strategies. Although Huishuan Account holds the top market share in the industry, it is only 0.5%, making it difficult to realize economies of scale. In this context, capital is more inclined to wait and see, awaiting industry consolidation or the emergence of profit turning points.

Today, after hitting the high near 24,000 in the early session and entering bearish positions, the index fell sharply by nearly over 600 points, immediately recouping yesterday's losses significantly.

Today, after hitting the high near 24,000 in the early session and entering bearish positions, the index fell sharply by nearly over 600 points, immediately recouping yesterday's losses significantly.

Moreover, today it broke the new high again, reaching a maximum of 24,076, but by the end of the market, it fell back by about 70 points, producing a bearish candle. The current trend has not yet been broken, but from the previous low until now, it has risen close to 6,000 points. It is believed that those with positions can continue to hold until there is a clear trend reversal for profit-taking. Those without positions can wait for a pullback to get in. Actually, it is hoped for a quick pullback, as it allows for entry and also provides a healthy breath.

Moreover, today it broke the new high again, reaching a maximum of 24,076, but by the end of the market, it fell back by about 70 points, producing a bearish candle. The current trend has not yet been broken, but from the previous low until now, it has risen close to 6,000 points. It is believed that those with positions can continue to hold until there is a clear trend reversal for profit-taking. Those without positions can wait for a pullback to get in. Actually, it is hoped for a quick pullback, as it allows for entry and also provides a healthy breath. Currently, the outlook remains the same as before. It is believed that even if there is a pullback, it shouldn't be too deep. However, if Futures fail to stabilize and close below 22,350, there may still be room for decline. The chance of Futures falling below 21,400 in the short term should be low, so it is considered that if a significant pullback occurs, it presents a good opportunity to incrementally go long. Recently, there has been a consistent approach to not hold positions overnight, only focusing on immediate trades, as there is no high chasing and no casual short selling.

Currently, the outlook remains the same as before. It is believed that even if there is a pullback, it shouldn't be too deep. However, if Futures fail to stabilize and close below 22,350, there may still be room for decline. The chance of Futures falling below 21,400 in the short term should be low, so it is considered that if a significant pullback occurs, it presents a good opportunity to incrementally go long. Recently, there has been a consistent approach to not hold positions overnight, only focusing on immediate trades, as there is no high chasing and no casual short selling.

Comment(0)

Reason For Report