布鲁可在昨日的暗盘表现同样不俗。该公司暗盘交易涨73.49%,报104.7港元。

布鲁可在昨日的暗盘表现同样不俗。该公司暗盘交易涨73.49%,报104.7港元。① How did Bluereco perform in the dark market? ② Why has the company attracted so much market attention?

Referred to as the "Chinese version of Lego", $BLOKS (00325.HK)$ On its first day, it performed brilliantly, surging more than 80% at one point after opening, drawing market attention. As of the time of reporting, Blokus has risen by 53.36%, trading at 92.55 Hong Kong dollars.

According to publicly available information, Bluereco specializes in building block toys and holds several Licensed Intellectual Property (IP) rights such as "Ultraman," being referred to as the "Chinese version of Lego." In 2023, the company's GMV (Gross Merchandise Volume) reached 1.8 billion RMB, capturing a 30.3% market share of the building block character toy market in China.

Bluereco also performed well in the dark market yesterday. The company's dark market trading rose by 73.49%, priced at HK$104.7.

Bluereco also performed well in the dark market yesterday. The company's dark market trading rose by 73.49%, priced at HK$104.7.

The performance on the first trading day and in the dark market is closely related to the market's subscription enthusiasm. According to related data, Bluereco received a subscription of 5,999.96 times during the public offering phase and 38.6 times for the international offering.

Additionally, Bluereco introduced three cornerstone investors for its IPO, including Jinglin Asset Management Hong Kong Limited, UBSAM Singapore, and Franklin Templeton Investments (Hong Kong) Limited.

The popularity of Bluereco is related to its associated IP.

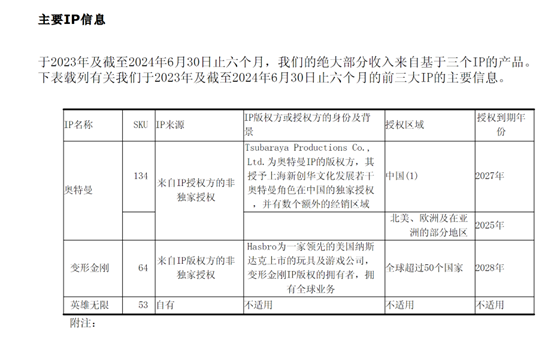

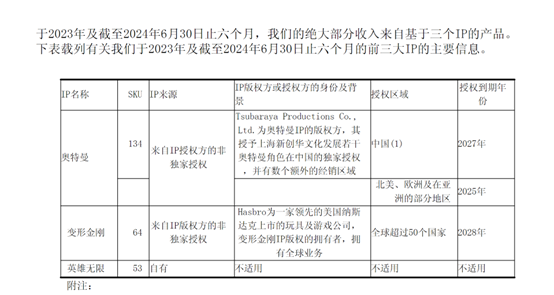

In 2023 and the first half of 2024, most of Blucco's revenue comes from products based on three Licensed Intellectual Properties (IP): Ultraman, Transformers, and Heroes Unlimited, which contributed over 90% of the revenue each year from 2021 to 2023.

Among them, the revenue from the Ultraman series reached 0.557 billion yuan and 601 million yuan, accounting for 63.5% and 57.4% of total revenue, respectively.

Moreover, in the current context of the booming "millet economy," the IP economy has received high attention and favor from the Capital Markets. Blucco holds the licenses for many well-known IPs, including Ultraman, Transformers, Super Sentai, Mobile Ultraman, DC Superman, DC Batman, Harry Potter, and Star Wars, which gives the company a strong market appeal and relevance, attracting significant attention from investors.

Institutions expect Blucco's future revenue to continue to grow.

SWHY forecasts that Blucco's annual revenue during the period of 2024-2026 will reach 2.201 billion yuan, 3.405 billion yuan, and 4.384 billion yuan, with corresponding growth rates of 151%, 55%, and 29%. The adjusted net income attributable to the parent company is expected to be 0.6 billion yuan, 1.061 billion yuan, and 1.407 billion yuan, with growth rates of 724%, 77%, and 33%, respectively.

CSC has also provided predictions, estimating Blucco's operating revenue for 2024-2026 to be 2.19 billion yuan, 3.45 billion yuan, and 4.34 billion yuan, with year-on-year growth of 149.8%, 57.7%, and 25.8%. The adjusted net income attributable to the parent company is approximately 0.58 billion yuan, 1.09 billion yuan, and 1.36 billion yuan, with corresponding growth rates of 699.0%, 87.7%, and 24.0%. Based on its high growth potential, China Securities Co., Ltd. has initiated coverage with a "Buy" rating.

However, China Securities Co., Ltd. also pointed out that Blucco faces many risks:

The first is the risk of IP license renewal. Currently, the motivation for consumers to purchase its products partly stems from their love for the cooperating IPs (such as Ultraman and Transformers, which accounted for 57% and 19% of 24H1 revenue respectively). If the IP license expires and it is difficult to renew or the renewal terms are unfavorable, the Operation will be hindered. Based on the 24H1 scenario, if the proportion of IP licensing fees in revenue increases by 1, 3, or 5 percentage points, adjusted net income could potentially decline by 2.7%, 8.0%, or 13.3%, respectively.

Secondly, there is the risk of channel management. Since 2022, the company has actively expanded its offline dealer channels, with this channel accounting for as much as 91.6% of revenue in the first half of 2024, and collaborating with 511 dealers. If channel management is poor, it may lead to inventory backlog and disorder in the pricing system, which will affect both brand image and product sales.

Thirdly, there is the risk of changes in toy trend fluctuations. Given the rapid changes in toy trends, if the company cannot collaborate with popular Licensed Intellectual Property (IP) and launch new products that meet consumer demands, its operating performance and growth potential may be impacted.

Fourthly, there is the risk of intensified market competition. If the number of competitors in the building block industry increases and their competition strategy becomes aggressive, Broccoli's revenue and performance growth may be hindered.

Futu draws new shares, truly 0 interest, 0 commission, dark pool trading one step ahead.Come and experience it>>

Editor/new