作为衡量美国国内需求的指标,包括对冲基金、养老基金、

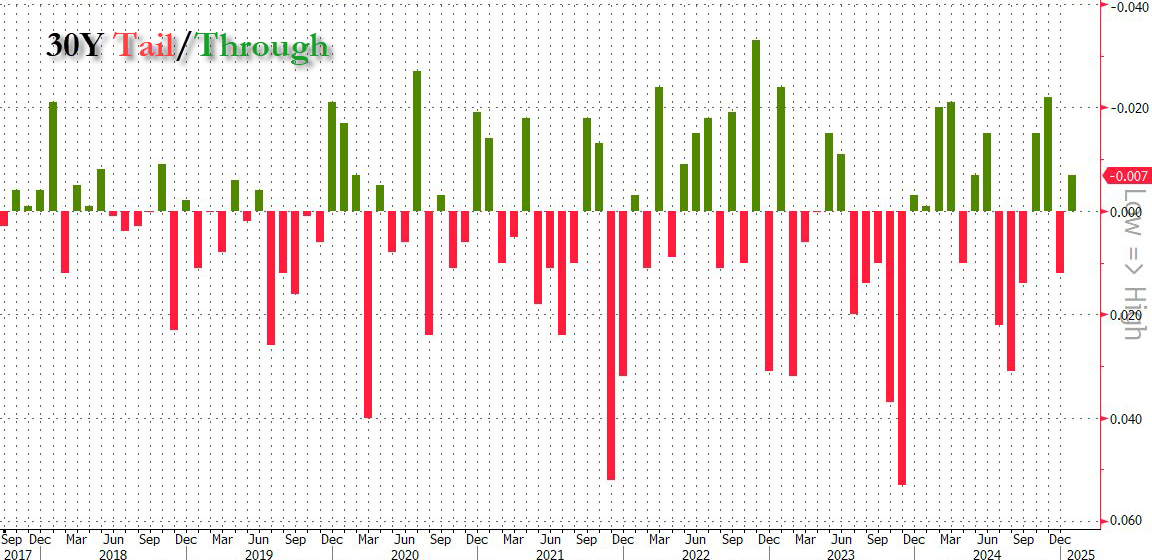

作为衡量美国国内需求的指标,包括对冲基金、养老基金、On Wednesday, the USA Treasury auctioned $22 billion in 30-year bonds, similar to the results of Tuesday's 10-year bond auction, with the yield rates reaching new highs not seen since 2007. However, from several indicators of this auction, it can be considered not a very bad sale, at least stronger than yesterday's 10-year bonds.

The winning yield rate for this 30-year bond auction was 4.913%, the highest since August 2007, compared to 4.535% on December 12. Although the yield rate is high, the highlight is that the pre-issue rate for this auction was 4.920%, which is higher by 0.7 basis points than the final winning yield, and there was no tail spread reflecting weak demand.

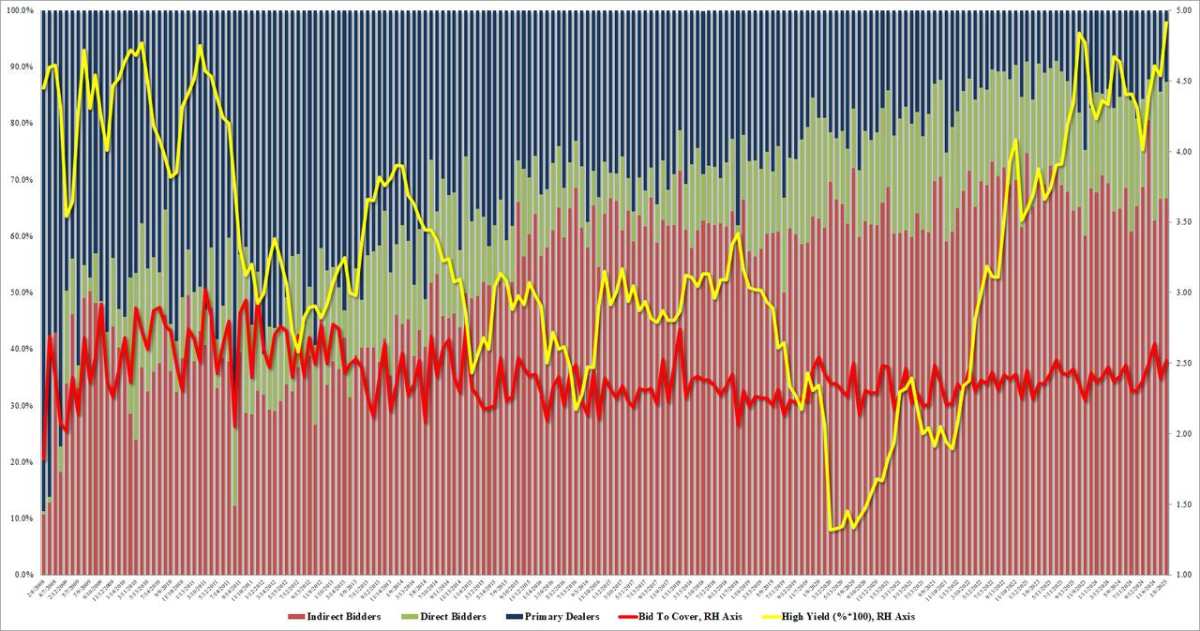

The bid-to-cover ratio for this 30-year bond auction was 2.52, compared to 2.39 in December, also above the average of 2.42 from the last six auctions.

As an indicator of domestic demand in the USA, the allocation ratio for direct bidders, including hedge funds, retirement funds,Mutual fundsinsurance companies, banks, government institutions, and individuals was 20.7%, up from 19.1% in December, and slightly higher than the average level of recent auctions.

As an indicator of domestic demand in the USA, the allocation ratio for direct bidders, including hedge funds, retirement funds,Mutual fundsinsurance companies, banks, government institutions, and individuals was 20.7%, up from 19.1% in December, and slightly higher than the average level of recent auctions.

As an indicator of overseas demand, the allocation ratio for indirect bidders, who typically participate in bidding through primary dealers or brokers such as foreign central banks, was 66.6%, slightly up from 66.5% in December, but below the average of 67.4% from recent auctions.

As the "white knight" taking on all unsold supplies, the allocation ratio for Primary dealers in this round is 12.7%, lower than 14.4% in December and the recent average of 14.6%.

The financial blog Zerohedge commented that overall, this was a mediocre auction. After the auction results were released, the yield on 10-year U.S. Treasury bonds surged by 4 basis points, once again approaching intraday highs.

Recently, the yield on US Treasury bonds has been steadily rising, becoming the focus of market attention. Wall Street expects the yield on 10-year US Treasury bonds to further rise to 5%. Deutsche Bank believes that the sell-off of US Treasury bonds is not completely over, and if the term premium returns to the average level of 2004-2013, the yield on 10-year US Treasury bonds should rise by about 40 basis points. However, Citibank believes that the rise in US Treasury bond yields to 5% will present a good buying opportunity.

Morgan Stanley's analysis indicates that as the yield on 10-year U.S. Treasuries rises above 4.5%, it has begun to pressure U.S. stock valuations, with the correlation between the S&P 500 Index and U.S. Treasury yields turning "significantly negative". Bank of America believes that if U.S. Treasury yields surpass 5%, investors may reassess the valuations of risk assets, leading to pressure on the stock market.