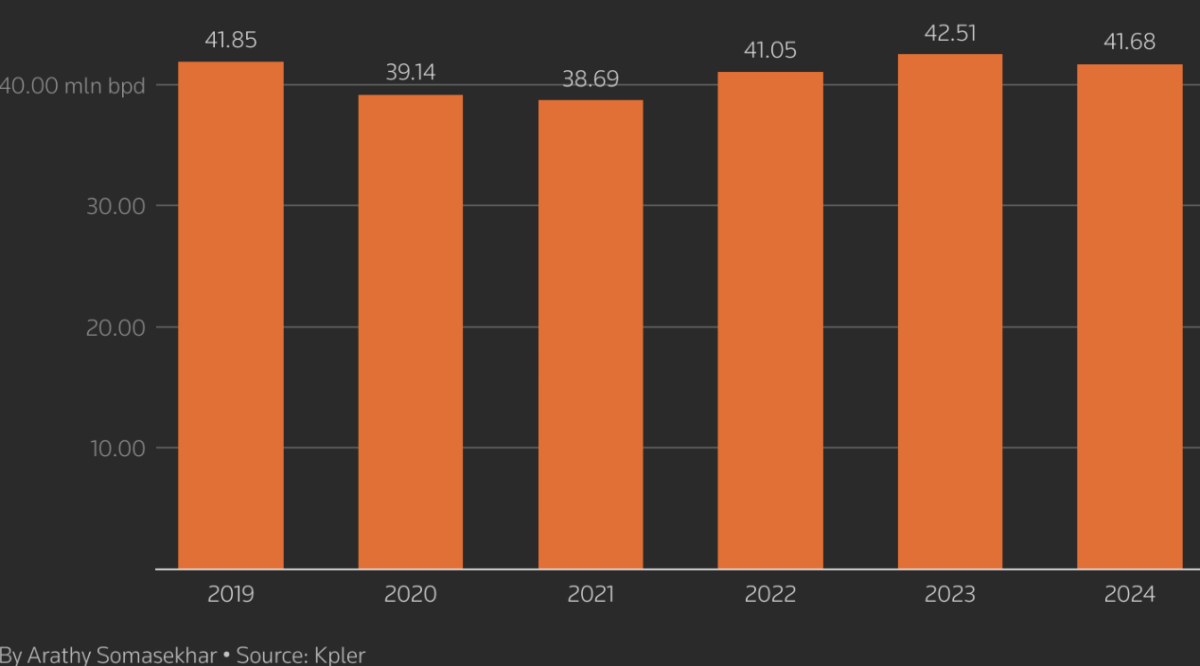

随着红海航运持续遭受攻击,欧洲的石油炼厂关闭,导致这些变化变得更加明显。Kpler的船舶追踪数据显示,2024年中东对欧洲的原油出口下降了22%。

随着红海航运持续遭受攻击,欧洲的石油炼厂关闭,导致这些变化变得更加明显。Kpler的船舶追踪数据显示,2024年中东对欧洲的原油出口下降了22%。The global oil trade map is being redrawn, uncertainty and volatility have become the new normal, and 2019 was the last "normal" year...

Transportation data shows that Global Crude Oil exports decreased by 2% in 2024, marking the first decline since the COVID-19 pandemic. The main reasons behind this are weak global demand growth, and changes in refineries and pipelines leading to a realignment of trade routes.

Global Crude Oil flows have also been disrupted for the second consecutive year due to the wars in Ukraine and the Middle East, with tanker shipping routes being redirected and suppliers and buyers being divided into different regions. Exports of oil from the Middle East to Europe have decreased, with more oil from the USA and South America flowing to Europe. Oil that used to be shipped to Europe from Russia has now been redirected to India and China.

As shipping in the Red Sea continues to face attacks, European oil refineries are closing, making these changes more apparent. Kpler's ship tracking data shows that in 2024, Crude Oil exports from the Middle East to Europe decreased by 22%.

As shipping in the Red Sea continues to face attacks, European oil refineries are closing, making these changes more apparent. Kpler's ship tracking data shows that in 2024, Crude Oil exports from the Middle East to Europe decreased by 22%.

"Changes in oil flows are creating opportunistic alliances," says energy consultant and former oil trader Adi Imsirovic, noting that the relationship between Russia and India, China, and Iran is becoming closer, thus reshaping oil Trade.

"Oil is no longer flowing along the lowest cost curve; the first consequence is shipping tightness, which has increased freight prices, ultimately cutting into refining margins."

With the surge in Shale Oil production, the USA has become a winner in the Global oil trade. The country exports 4 million barrels of oil daily, and its global oil trade share has increased to 9.5%, second only to Saudi Arabia and Russia.

Trade routes have been reshuffled due to the launch of Nigeria's Dangote large refinery, the expansion of Canada's Trans Mountain pipeline to the west coast, declining oil production in Mexico, a temporary halt in Libyan oil exports, and rising output in Guyana.

By 2025, suppliers will continue to face declining demand from major Consumer centers like China. Additionally, more countries will reduce oil usage and increase the use of Henry Hub Natural Gas, while Wind Power will continue to grow.

Erik Broekhuizen, the maritime research and consulting manager at the Ship brokerage firm Poten & Partners, said,

"This uncertainty and volatility are the new normal - 2019 was the last 'normal' year."

Broekhuizen said that changes in oil demand forecasts have shaken long-standing assumptions about oil market demand growth, "In the past, you could always say there would be healthy long-term demand growth, and that would resolve many problems over time. That is no longer taken for granted."

For instance, China's imports fell by about 3% last year, primarily due to the rise of electric and plug-in hybrid vehicles, as well as the increased use of liquefied natural gas in heavy truck transportation. In Europe, a decline in refining capacity and government decarbonization targets have reduced crude oil imports by about 1%.

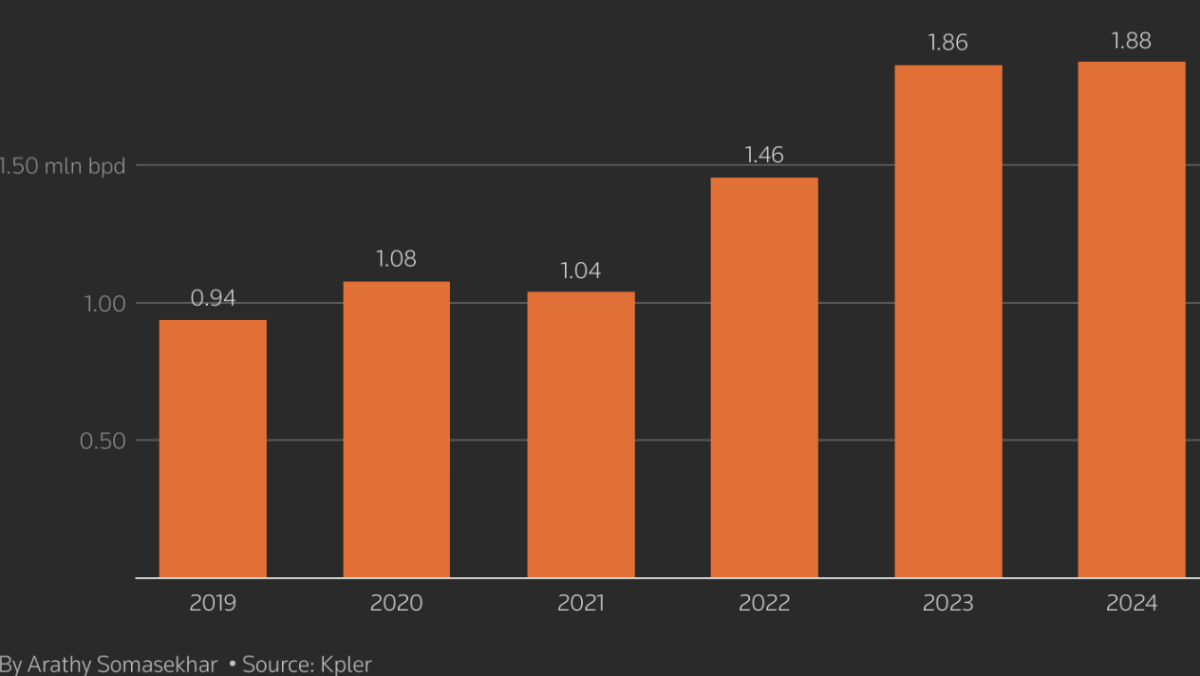

As European refiners reduce imports from Russia and increase purchases of oil from the USA and the Middle East, and as costs for transporting from the Middle East rise due to attacks on vessels in the Red Sea following the Gaza war, they have intensified imports from the USA and Guyana, reaching record highs.

In 2024, Iraq's exports decreased by 82,000 barrels per day, and the United Arab Emirates' exports decreased by 35,000 barrels per day. Europe increased imports from Guyana by 162,000 barrels per day and from the USA by 60,000 barrels per day.

At the end of September, with the escalation of the conflict in the Middle East and concerns about the possibility of more sanctions from Trump, Iranian oil supply became tight and prices rose. This also prompted Chinese refiners to begin considering purchasing oil from West Africa and Brazil.

According to Kpler, Nigeria's new Dangote refinery consumed a large amount of domestic supply. In 2024, about 13% of Nigeria's crude oil exports remained in the country, up from 2% in 2023. This reduced Nigeria's exports to Europe, and Nigeria even imported 47,000 barrels per day of US WTI crude oil, which is unusual for a major net exporter.

The new refinery capacity in Bahrain, Oman, Iraq, and Mexico's Dos Bocas may also absorb oil production from these regions.

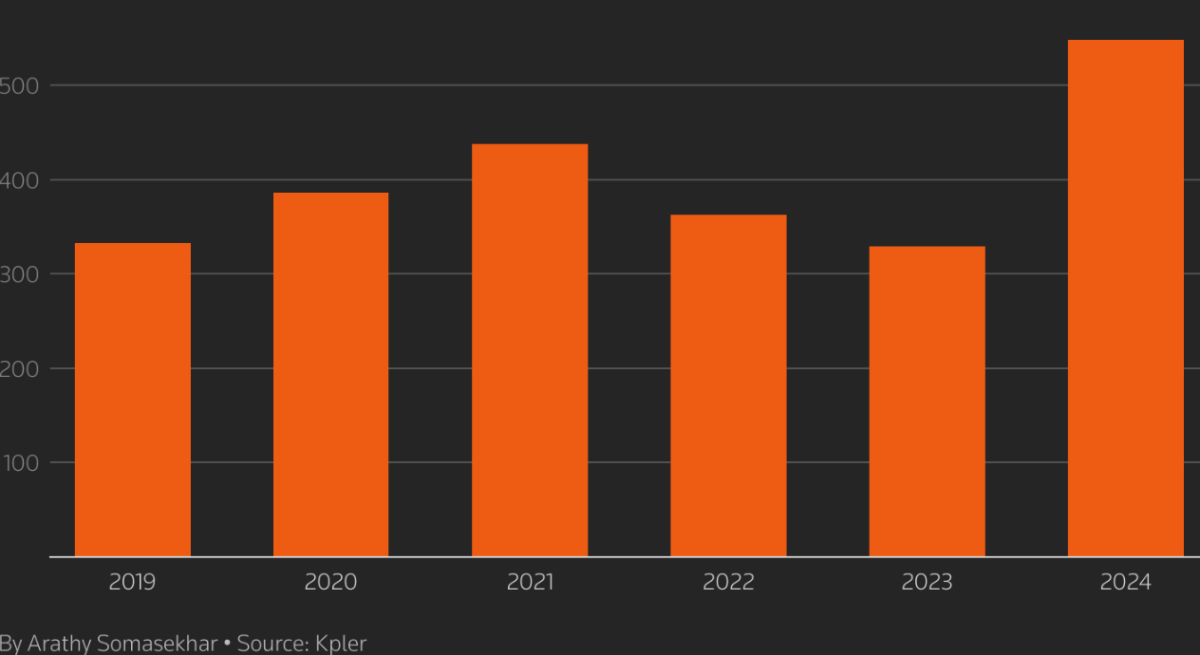

In Canada, the expanded Trans Mountain pipeline can now deliver an additional 590,000 barrels per day to the Pacific coast, making the country's waterborne exports reach a record 550,000 barrels per day in 2024.

This has created a chain reaction: as more Canadian Crude Oil flows to the West Coast of the USA, refineries in the region have reduced purchases of Crude Oil from Saudi Arabia and Latin America, while Canada's direct Transportation to Asian countries also diminished the re-export from the US Gulf of Mexico.

Analysts point out that China is the main buyer of Canadian Crude Oil. These Crude Oil products have also found importers in India, Japan, South Korea, and Brunei. An increasing number of Asian refiners may purchase this oil.

Analysts also stated that Trump's proposal to impose a 25% tariff on Canadian and Mexican Crude Oil, the two largest oil suppliers to the USA, could also change the direction of oil flow in 2025.