Pfeffer 认为,

Pfeffer 认为,Author: Donovan Choy, Blockworks; Translated by: Tao Zhu, Jinse Finance.

In 2017, investor John Pfeffer published "(Institutional) Investors' Views on Crypto Assets", a groundbreaking paper on long-term investment in crypto tokens.

In hindsight, Pfeffer's original paper was far ahead of its time. It laid the groundwork for investors to think about the magical internet currency and made many predictions that still hold true today.

Pfeffer believed that the long-term equilibrium outcome would be the dominance of a crypto asset as a store of value, and Bitcoin could be one of them. He predicted that BTC's Market Cap would be between 4.7 and 14.6 trillion USD (each BTC 0.26 million to 0.8 million USD).

Pfeffer believed that the long-term equilibrium outcome would be the dominance of a crypto asset as a store of value, and Bitcoin could be one of them. He predicted that BTC's Market Cap would be between 4.7 and 14.6 trillion USD (each BTC 0.26 million to 0.8 million USD).

There are many reasons Pfeffer believes Bitcoin will solidify its dominant SOV position, but the key point of the paper is that the technical risks borne by BTC are minimal. To defeat BTC in the SOV game, ETH would need massive intellectual coordination over many years of roadmap, and many technological upgrades may face delays and/or failure risks.

As Hasu mentioned in the old Uncommon Core podcast, "The fact that nothing has happened on Bitcoin is actually the best thing that could happen to Bitcoin."

Speaking of Ethereum, nowadays ETH bulls tend to argue in multiple ways that ETH is superior to BTC: its use as a means of payment within the EVM ecosystem reinforces its value as SOV (besides the deflationary effect post EIP-1559).

But it remains unclear why this alone can make ETH a valuable SOV.

Pfeffer believes that cryptocurrency participants only need to convert their preferred "store of value" into the exact amount required through payment channels at the time of payment, and to do so as quickly as possible. He likens this to retailers converting bank deposits into physical cash only when needed for payment.

Pfeffer also foresaw that Ethereum's scaling solutions (such as L2 and transitioning to proof of stake) would "benefit adoption/users, but be detrimental to token value/investors". Given the constant complaints on Crypto Twitter about the lack of appreciation in last year's ETH prices, this viewpoint has proven to be extremely correct.

So, how much is ETH worth?

Today, Pfeffer's landmark paper is being revisited through a newly published paper on the Triton liquidity fund he co-authored.

The conclusion of the paper is: Ethereum is a technological marvel, but the risk-adjusted upside potential of ETH is difficult to predict.

One can attempt to value ETH as a cash flow asset. However, the continuous innovations of Ethereum in its protocol and tokenomics make DCF analysis "difficult to conduct accurately".

Even so, the paper attempts this based on generous assumptions that issuance is net neutral, plus an average growth rate of 5%. However, regardless of the discount rate used, "ETH today seems severely overvalued as a $400 billion cash flow asset."

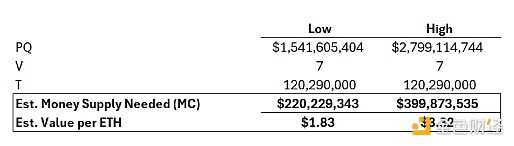

Then, one can turn to the "monetary premium" argument for ETH. But contrary to ETH bulls, ETH is not money—it is not even the de facto unit of account in the EVM ecosystem (that is the dollar). For example, the largest L2 on Ethereum, Base, started offering the option to pay gas fees using USDC instead of ETH last month.

Even if ETH is seen as the main trading medium on-chain, attempting to justify ETH's valuation of about 400 billion USD based on "monetary premium" is simply wishful thinking. This paper estimates Ethereum's on-chain "GDP" at approximately 2.8 billion USD (based on annualized data from the past six months), which is about 1000 times higher than the current valuation.

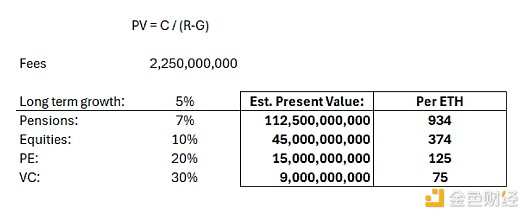

The strongest argument for ETH as an investable asset is that it is the dominant internet-native commodity and productive on-chain asset. Holding ETH is not like holding gold bars or oil—people can stake it in DeFi to earn returns.

However, the paper questions whether Lido's 3% yield exceeds the inherent volatility of ETH, making it suitable as an "internet bond."

Conclusion: "Currently, with ETH's market cap at 400 billion USD, considering its current trend, it is challenging to prove that ETH is a long-term reasonable investment adjusted for risk, regardless of the perspective used to evaluate it... BTC still maintains its status as a robust bet adjusted for risk, and it can evolve into a role as a non-sovereign store of value."