The underlying logic of the Reagan cycle is to suppress inflation with tight MMF, stimulate growth with loose regulation, and ultimately create a cycle of "economic growth - strong dollar - strong U.S. stocks" in growth, liquidity, and Assets.

According to Zhito Finance APP, China Securities Co.,Ltd. released a Research Report stating that the underlying logic of the Reagan big cycle is to use tight currency to suppress inflation, loosen regulation to stimulate growth, ultimately creating a cycle of "economic growth - strong dollar - strong US stocks" in terms of growth, liquidity, and assets. Whether Trump can replicate Reagan depends on the sustainability of the AI Technology revolution, as the future trend of US stocks will depend on the continuity of the technology revolution driven by AI. If technology proves to be sustainable, then US stocks will be strong, and US Treasury rates may remain high due to a "seesaw effect."

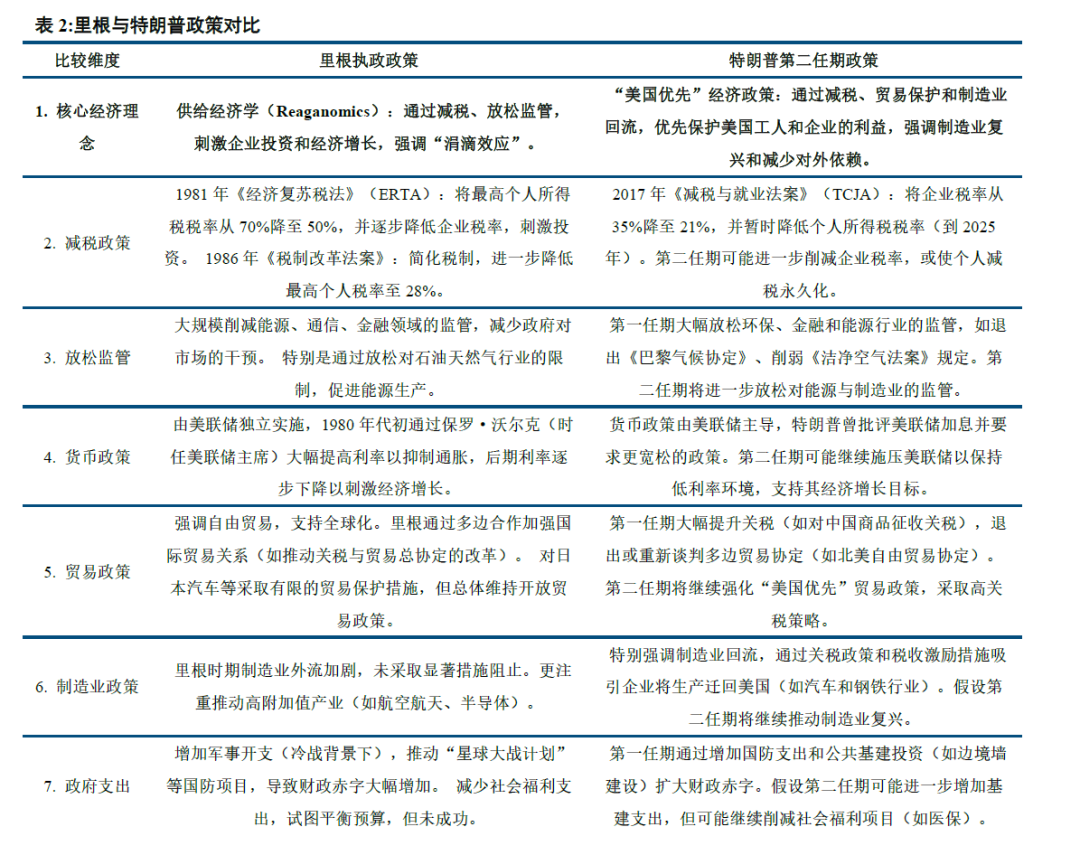

Comparing Reagan and Trump, the biggest similarity between the two is that their core policy ideas are consistent, namely, "tax cuts" and "deregulation."

Comparing Reagan and Trump, there are four key differences between the two:

Comparing Reagan and Trump, there are four key differences between the two:

Firstly, there are differences in policy emphasis. Trump places more emphasis on immigration and tariff issues, aiming for "American manufacturing to return." The main issue Reagan needed to address was "stagflation," and he did not overly restrict the outflow of manufacturing. In fact, the Reagan era can be seen as the beginning of the outflow of American manufacturing.

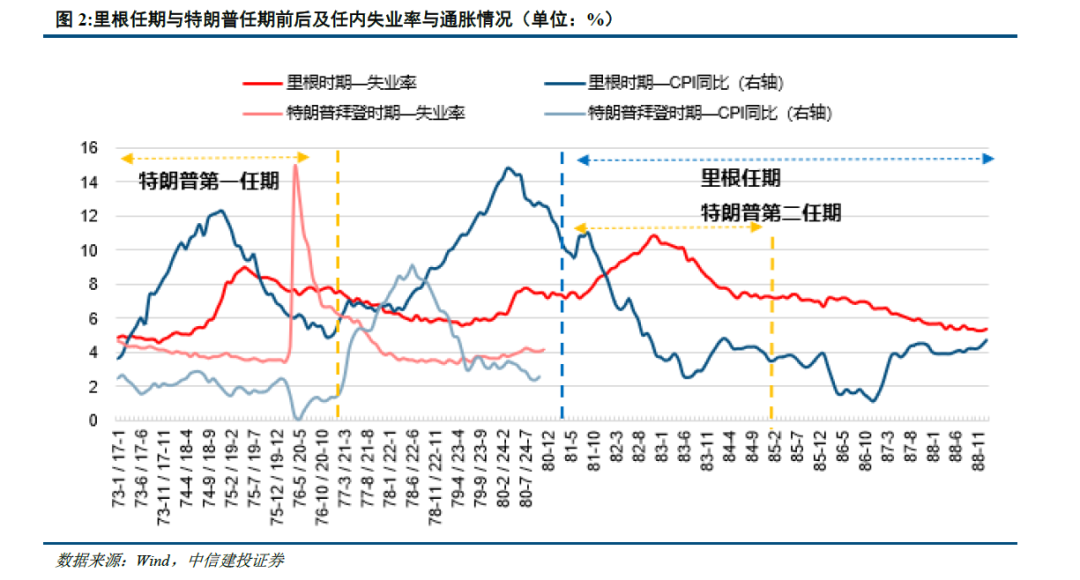

Secondly, the economic situation is different. When Reagan took over, the USA was experiencing a terrible stagflation. Unlike the Reagan era, the American economy under Trump was healthier.

Thirdly, the focus of Technology is different. From the Reagan era to the eve of Trump 2.0, the USA has been a leader in a new generation of technological waves, with Trump's period leaning more towards Software. The driving forces of technology were hardware dominated during Reagan's time, while the core during Trump's time was algorithms and data. Economic impact model: the PC revolution directly created new industries, whereas the AI revolution primarily functions through optimizing traditional industries and promoting digital transformation. Stock market performance: during Reagan's time, tech stocks were just emerging, while during Trump’s time, tech giants had already become dominant forces.

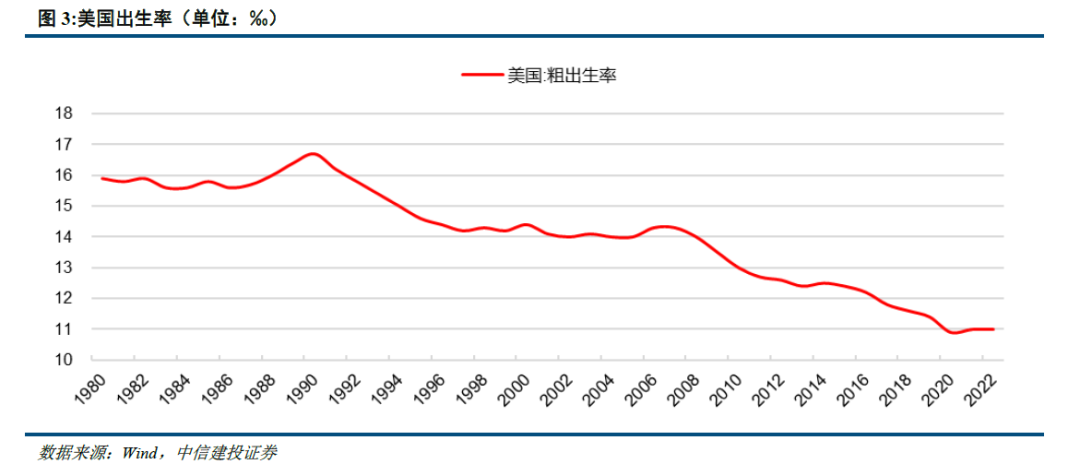

Fourthly, population growth and driving forces differ. Population growth during Reagan's time relied mainly on the post-war baby boom. In Trump's time, although the birth rate declined, immigration became a vital source of population growth.

The real key to the Trump cycle lies in Technology.

1. The cycle of 'economic growth - strong dollar - strong US stocks' has already started.

In early 2020, with the outbreak of the pandemic, the USA fell into a brief recession, and the unemployment rate surged. It is precisely because of the brief shock of the pandemic that the economy itself is easier to recover. Coupled with the broad easing of American fiscal and monetary policy, this recession was easily resolved.

"The 'big cycle' reemerges, and the combination of 'expansive fiscal policy and tight monetary policy' successfully stimulates the vitality of USA's industry and consumption, forming a virtuous cycle between industry and consumption.

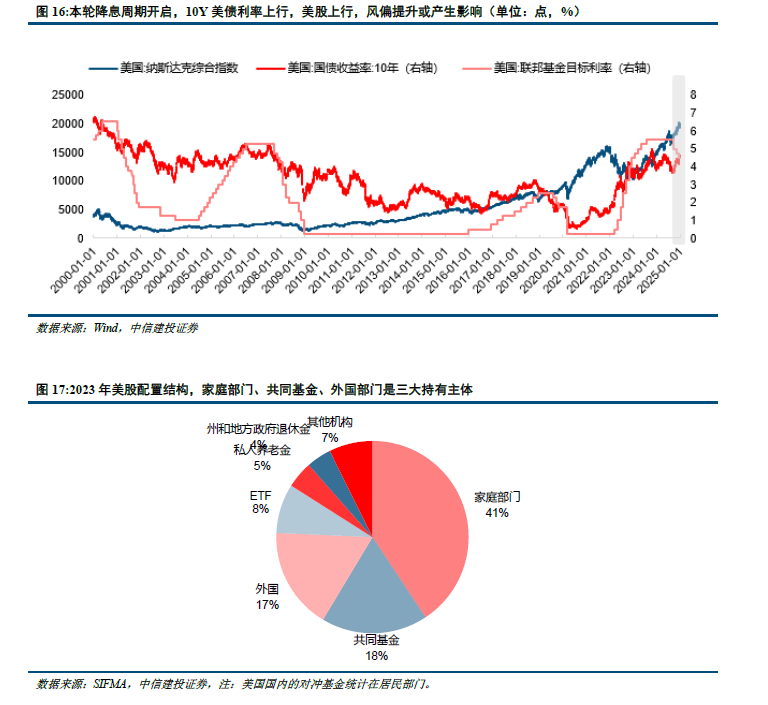

Subsequently, the USA tightens its monetary policy, yet this does not impact the US stock market. Generally, tight monetary policy would affect liquid assets (such as Stocks), but under the support of Technology, tight monetary policy actually comes alongside a return of the dollar, which is why liquidity in the stock market is not necessarily hurt during tight monetary conditions.

The USA has become a global high-interest zone, with low-cost overseas funds continuously flowing into the USA. On one hand, this enhances American Financial Assets and increases the wealth effect for residents; on the other hand, it promotes real investment in the USA, helping to achieve the investment boom in the AI industry.

2. Whether the Trump cycle can run smoothly depends crucially on the sustainability of Technology, which is also key to the current direction of the USA's economy and Assets.

The current wave of the AI revolution originates from Biden's industrial stimulus policy, which is crucial for the US stock market today and for the return of the dollar. The USA's Technology sector is experiencing large-scale investments, with investments primarily reflected in construction expenditures, while equipment investment is still at the early growth stage. Clearly, this wave of AI is also key to the direction of the USA's economy.

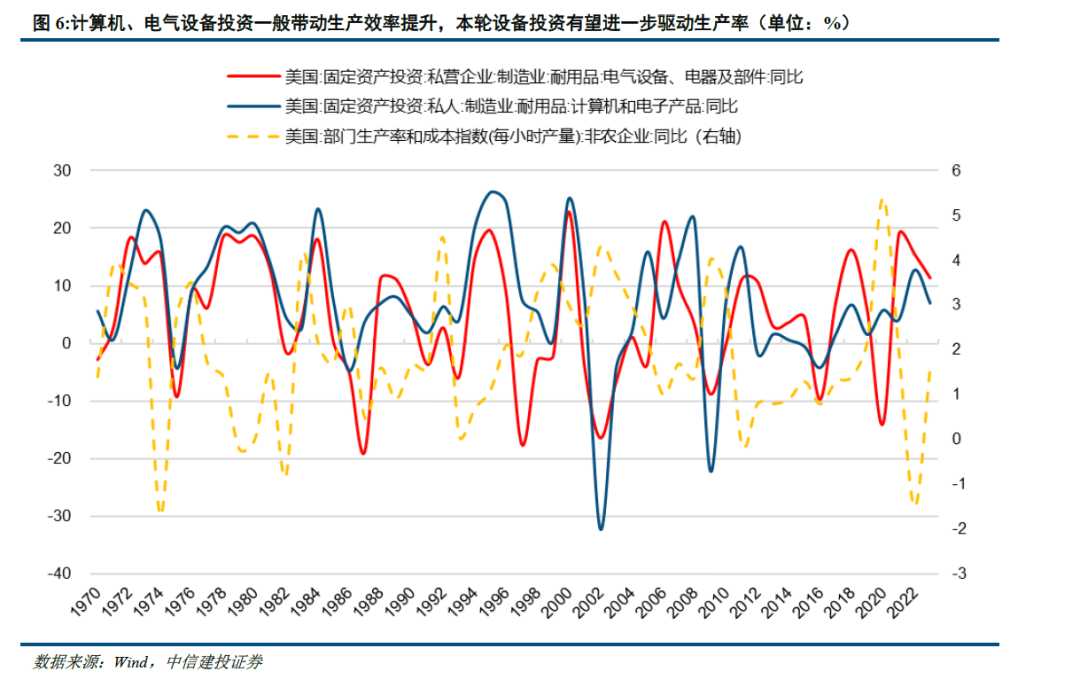

The explosive growth of the AI industry first promotes investment growth. Investments in computers and Electrical Equipment stimulate productivity improvements. Understanding this, we can understand why the USA has shown resilience in growth in recent years, faced challenges in the last mile of inflation, a strong US stock market, and a weaker US bond market.

The potential impact on Global Asset Prices.

1. US Stocks: Under the drive of the Technology Industry, US Stocks are unlikely to weaken, and the key to their renewed strength depends on the sustainability of the technology revolution.

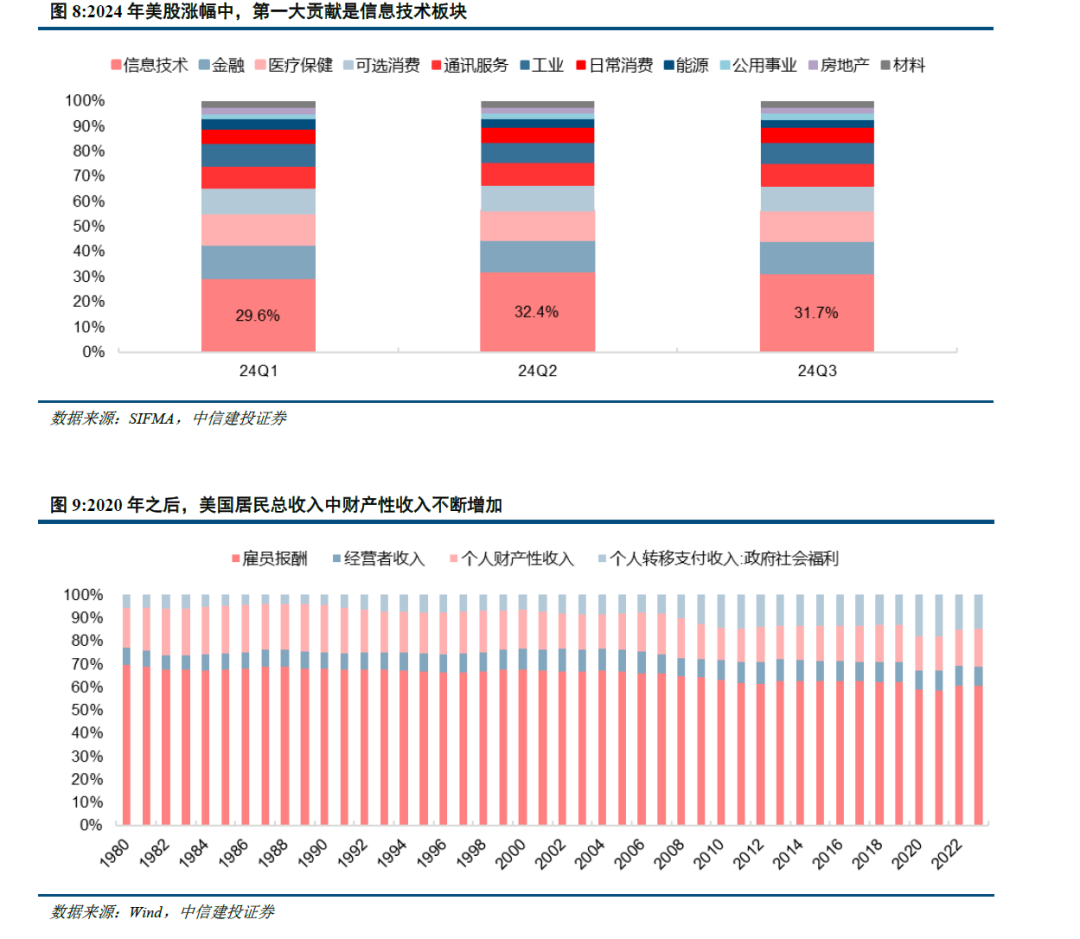

In 2024, the performance of American Technology Stocks remains impressive and continues to be an important driver of growth in US Stocks. In the second half of the year, financial conditions are eased, providing another boost to US Stocks. In 2024, the growth rate of construction expenditure in the USA's high-end manufacturing industry is still significantly higher than that of equipment investment.

Whether there can be sustained equipment investment expenditure in the future depends crucially on the development trend of the Technology Industry.

2. US Bonds: The probability of experiencing another round of 'reflation' is low; the question is how much downwards space there is for US Bond interest rates, or whether they will maintain high volatility at elevated levels. Currently, this is where market divergences lie. We believe that if US Stocks remain strong and the risk appetite of funds is not weak, then US Bond interest rates may still be elevated due to the 'seesaw' effect.

In 2024, the USA's battle against inflation has made significant progress, though the final 'one kilometer' has been a repeated and slow journey. The most important factors are that investment in Technology and high-end manufacturing leads to growth in R&D investments, and at the same time, the USA's labor market remains relatively strong, thus keeping service industry inflation represented by rents at high levels. This is a potential consequence of the 'MAGA movement'. The probability of rapid declines in service industry inflation in 2025 is low.

3. US Dollar: The future trend depends on the direction of the interest rate spread between the USA and non-USA driven by AI.

In this round of dollar tides, dollars continue to flow to the USA. The seemingly direct reason is that the USA's growth is relatively strong, and the US stock market currently has appeal, reflected in the higher interest rate spread between the USA and non-US countries. In fact, the interest rate cycles of the USA and non-US countries are not synchronized, and the key is that the USA is the leader in this round of AI industry development, with Technology and high-end manufacturing rapidly developing and possessing potential high yields.

4. CSI Commodity Equity Index (Industrial Products): By 2025, the pricing of industrial products will be more based on expectations.

High interest rates suppress, trade frictions may escalate, Industry Chain restructuring may happen, and Global demand for industrial products may remain weak. China's economy is still in a weak recovery process, and weak global manufacturing makes it difficult for Global demand for industrial products to improve significantly, leading to weak industrial product prices.

5. Gold: Gold prices are not weak, and the conditions for the strength of gold (i.e., significant liquidity expansion and geopolitical factors) are uncertain.

Gold is primarily priced based on its financial and MMF properties. In the medium term, gold prices are not weak, and further strength depends on US Treasury bond yields and geopolitical conflicts. The reason gold prices are not weak is due to central banks continuously buying gold supported by the logic of changes in the international monetary system.