麦德龙(Metro),正是那个办会员卡才能进,和山姆(Sam's Club)和开市客(Costco)齐名的仓储式超市。物美,则是区域性超市龙头。据披露,截至2021年,物美超市在国内北方区域的市占率为35%,其中在北京区域的市占率为56%。

麦德龙(Metro),正是那个办会员卡才能进,和山姆(Sam's Club)和开市客(Costco)齐名的仓储式超市。物美,则是区域性超市龙头。据披露,截至2021年,物美超市在国内北方区域的市占率为35%,其中在北京区域的市占率为56%。Relying on Wumart may escalate financial anxiety.

Half a year later, Metro Supply Chain has once again submitted an application to the Hong Kong Stock Exchange, with UBS Group and China Merchants serving as joint sponsors. This listing application marks Metro Supply Chain's determination to further expand into Capital Markets.

The updated prospectus shows that Metro Supply Chain positions itself as a provider of fast-moving consumer goods supply chain solutions for CHINA FOODS, mainly targeting three areas: providing retailers with retail distribution solutions (including product sales and supply chain services to retailers); offering food service and distribution solutions to corporate and Institutional clients, as well as welfare gift solutions. As of July 31, 2024, the company provides retail distribution solutions to 99 Metro stores and 342 Wumart supermarket stores and 287 Wumart convenience stores.

Metro (Metro) is the warehouse-style supermarket that requires a membership card to enter, alongside Sam's Club and Costco. Wumart is a regional supermarket leader. According to reports, as of 2021, Wumart supermarkets had a market share of 35% in northern China, with a market share of 56% in Peking.

Metro (Metro) is the warehouse-style supermarket that requires a membership card to enter, alongside Sam's Club and Costco. Wumart is a regional supermarket leader. According to reports, as of 2021, Wumart supermarkets had a market share of 35% in northern China, with a market share of 56% in Peking.

With two major well-known clients backing it, the company has an extraordinary position in the supply chain industry. According to Frost & Sullivan, based on revenue in 2023, Metro is the second largest provider of fast-moving consumer goods supply chain solutions in China, with a market share of 0.2%.

However, from a financial standpoint, the company cannot conceal its volatility. Additionally, its dependence on Wumart exacerbates financial concerns, which has become a major factor for investors' worries.

Revenue has declined for three consecutive years, with profits on a 'roller coaster.'

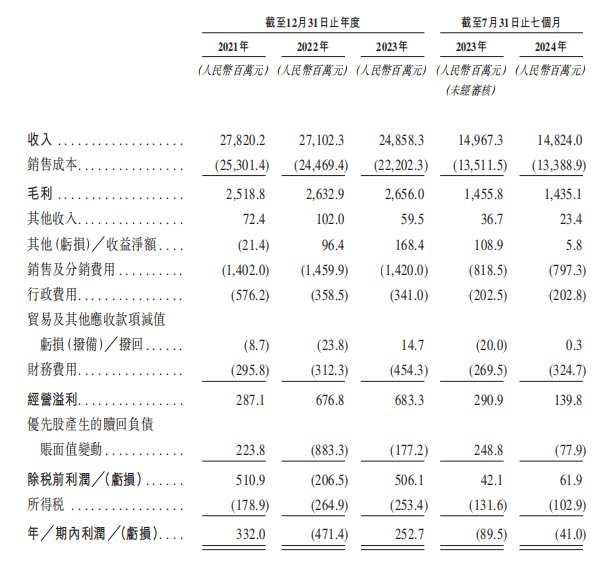

Despite being a leader in the fast-moving consumer goods supply chain solutions for food, the revenue of Metro Supply Chain does not look good. From 2021 to 2023 (hereinafter referred to as the reporting period), the company's revenues were 27.82 billion yuan (currency: RMB, the same below), 27.102 billion yuan, and 24.858 billion yuan, respectively, showing a continuous decline, with a three-year compound annual growth rate of -5.47%.

Meanwhile, the company's profits also fluctuated greatly, with net incomes of approximately 0.332 billion yuan, -0.471 billion yuan, and 0.253 billion yuan, respectively, resulting in a three-year compound annual growth rate of -12.76%, with significant losses in 2022. In terms of interest rates, the company's gross margin during the period was approximately 9.1%, 9.7%, and 10.7%, which was relatively stable; the net margin was approximately 1.2%, -1.7%, and 1.0%, which was more volatile. The net margin was thin.

In the first seven months of 2024, the company's revenue was 14.824 billion yuan; during the same period, the profit was -0.041 billion yuan, again resulting in losses.

While the performance is unstable, the other Financial Indicators of Metro Supply Chain are also concerning.

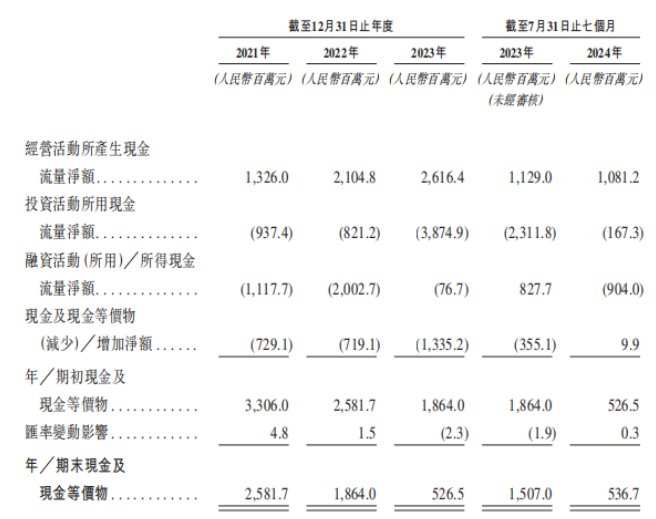

From 2021 to July 31, 2024 (hereinafter referred to as the reporting period), the company's cash and cash equivalents were 2.58 billion yuan, 1.86 billion yuan, 0.53 billion yuan, and 0.54 billion yuan, respectively, with cash flow continuously shrinking. Especially as of the end of July 2024, the cash and cash equivalents on hand were only about 0.5 billion yuan.

While cash on hand is decreasing, the company's external debts continue to grow significantly. From 2021 to July 31, 2024, the company recorded net current liabilities of 10.24 billion yuan, 12.34 billion yuan, 15 billion yuan, and 16.23 billion yuan, respectively. As of July 31, 2024, the company's total liabilities reached 27.01 billion yuan, raising significant debt repayment concerns.

Cash is far from covering current liabilities, which will pose a huge challenge to the liquidity of the Metro supply chain. The company also indicated in its risk warning that if it fails to maintain sufficient cash and financing, the Metro supply chain may not have enough cash flow to fund its business, Operation, and capital expenditures.

The company has divided its Business into several segments, with the top three being: retailer distribution solutions, food service and distribution solutions, and welfare gift solutions, which accounted for 60%, 14%, and 14% of revenue in 2023, respectively.

Although the top three businesses collectively account for over 80% of the company’s revenue, they are not crucial to the company’s profitability. The hidden insight lies in the Other businesses which have the lowest revenue share.

From 2021 to 2023, the revenue share of Other businesses was 3%-4%. According to the notes in the Earnings Reports, more than half of the revenue from Other businesses came from rental income, which remained stable at around 0.5 billion yuan from 2021 to 2023. The net income during the reporting period was lower than the rental income for the same period. In other words, the company’s supply chain business has always been operating at a loss, and the company completely relies on 'collecting rent' to sustain itself.

Relying on Wumart's 'beauty' and 'ugliness'.

According to disclosures, Wumart Group has always been the company's largest client. During the historical record period, revenue from Wumart Group accounted for 61.5%, 62.3%, 62.0%, and 61.4% of the company's total revenue.

However, revenue from Wumart Group decreased from 17.097 billion yuan in 2021 to 16.889 billion yuan in 2022 and further decreased to 15.405 billion yuan in 2023, as well as declining from 9.443 billion yuan in the seven months ending July 31, 2023 to 9.105 billion yuan in the same period of 2024.

The reduction is mainly due to Wumart Group optimizing its network to close underperforming stores and adopting a membership system in its retail store strategy. The decrease in Wumart Group's procurement is the main reason for the decline in Metro's supply chain revenue.

Compared to Wumart, Metro's supply chain has a weaker voice, which is reflected in the Earnings Reports through the continuous high growth of the company's receivables. During the reporting period, the company's receivables from related parties were 1.87 billion yuan, 2.74 billion yuan, 4.53 billion yuan, and 4.47 billion yuan respectively, with year-on-year growth rates of 46.5% and 65.3%. The accelerated growth of receivables from related parties undoubtedly exacerbates the cash flow situation of Metro's supply chain.

On the other hand, through Wumart's empowerment, Metro's supply chain can enjoy the growth dividends of the domestic fast-moving consumer goods supply chain Industry.

According to Frost & Sullivan's data, by revenue, the market size of China's fast-moving consumer goods supply chain Industry has increased from RMB 7036.6 billion in 2018 to RMB 9900.7 billion in 2023, with a compound annual growth rate of 7.1%. It is expected to continue to grow at a compound annual growth rate of 7.4% from 2023 to 2028, with the market size expected to reach RMB 14149.7 billion by 2028.

In terms of competition, the fast-moving consumer goods supply chain Industry in China is highly fragmented. As of 2023, the market share of the top five fast-moving consumer goods supply chain solution providers is 0.8%. In the same year, Metro's supply chain market share was 0.2%, making it the second largest fast-moving consumer goods supply chain solution provider in China. From the revenue scale perspective, the gap between the company and the leaders is not significant.

In short, Metro, backed by Wumart, possesses both 'beauty' and 'ugliness.'

Currently, in the vast trillion-yuan market, there is no absolute leader. As industry concentration continues to rise, the growth potential for Metro's supply chain is considerable. If it can successfully pass the Hong Kong Stock Exchange hearing, the company is expected to enhance its Industry Chain influence and consolidate its market position by expanding its comprehensive supply chain to incorporate more categories of industry participants.

However, whether it is for further market expansion domestically or for enhancing operational independence, Metro's supply chain must improve its profitability and smooth out operational fluctuations. Now, Metro's supply chain has entered a critical crossroads in its development, with cash flow continually shrinking and liabilities consistently rising, urgently needing to go public to meet short-term funding needs and ensure long-term competitiveness.