One of the biggest questions facing market participants is how many times the Federal Reserve will cut interest rates in 2025. Some even suggest the possibility of an interest rate hike within the year.

The Federal Reserve and its decisions on monetary policy are significant. The actions of the Federal Reserve affect the cost and availability of money, which can impact the economy.

However, some analysts in the market believe that the Federal Reserve's relevance is currently much lower than during the economic crisis, which required sudden and significant changes in policy to address issues such as soaring inflation, plunging economic activity, and a shortage of market liquidity.

The economy continues to grow while cooling down. Although inflation is slightly above the Federal Reserve's target, it does not constitute a crisis.

The economy continues to grow while cooling down. Although inflation is slightly above the Federal Reserve's target, it does not constitute a crisis.

After the hawkish monetary policy widely believed by the market was announced last December, there were concerns that the Federal Reserve's rate cuts would be lower than expected, which is bearish for stocks.

But for stock market investors, this narrow focus on rate cuts is misguided. The number of times the Federal Reserve cuts rates is not the right question.

Instead, what matters is the economic developments that lead the Federal Reserve to adjust its monetary policy outlook.

(Image source: finance.yahoo)

In the latest economic forecast summary released in December last year, the Federal Reserve raised its estimates for GDP growth in 2024 and 2025, while lowering its estimates for the unemployment rate. These forecasts also increased the inflation predictions and decreased expectations for interest rate cuts.

Perhaps better-than-expected economic performance is the reason for inflation being slightly above target and the continued rollback of interest rate cut expectations. Is that a terrible combination of factors?

Fewer interest rate cuts? No problem.

Despite some fluctuations in recent months, the stock market has remained strong, with the S&P 500 Index mostly trending upward.

It can be said that the outlook for MMF policy is becoming increasingly hawkish.

Goldman Sachs' Jan Hatzius stated in a note to clients on December 23 last year that financial markets have significantly reduced expectations for the easing of US MMF policy. "Federal funds futures now imply that the total amount of interest rate cuts in 2025 will be below 40 basis points, down from 125 basis points after a 50 basis point cut in September."

Currently, there is a common perception in the market that interest rate cuts will be bullish for risk assets like Stocks. Therefore, any development that lowers the probability of short-term interest rate cuts will be bearish. This view makes sense under all other conditions being equal.

But the world is complex, and other things are never equal.

The Fed's decisions on MMF policy - and the market's expectations of those decisions - do not occur in a vacuum. They happen against the backdrop of everything happening in the economy.

The economy has consistently exceeded expectations. Better-than-expected economic results help explain better-than-expected earnings growth, and earnings are the most important driver of stock prices. These Indicators are not bearish.

Early 2024 seems familiar.

A year ago, there was a very similar discussion on TKer: 'Whether the Fed will cut rates is not the right question.'

By the end of 2023, the market believed that the Fed would first cut rates in March 2024. However, as economic data surged far beyond expectations, those odds plummeted.

From an investor's and economic perspective, the economy has not collapsed, and this is not the worst thing in the world. Because when it comes to the Fed's pivot, many of these assumptions are also related to the idea that the economy is cooling - growth is slowing down, and many have become more vigilant about a recession. Therefore, perhaps the Fed will not pivot because the economy is recovering.

As known now, the initial rate cut has been delayed until September 2024.

Importantly, during this period, the stock market continues to rise.

Outlook Forecast

Just as everyone wants to avoid an economic crisis, history shows that this is inevitable. Therefore, the Federal Reserve's policy decisions may have a more significant impact on market outlook.

But currently, monetary policy is just one of many things that can drive the market.

Bank of America’s Savita Subramanian stated in September, "For USA Stocks ROI, policy measures are more important than the scarcity or abundance of company profits."

This illustrates the truth about the stock market, "News regarding the economy or policy will drive the market to the extent of expected impact on earnings. Earnings (also known as profits) are the reason you invest in a company."

Currently, the outlook for earnings growth remains good.

Macroeconomic Review

As of now, there are several noteworthy data points and macroeconomic developments:

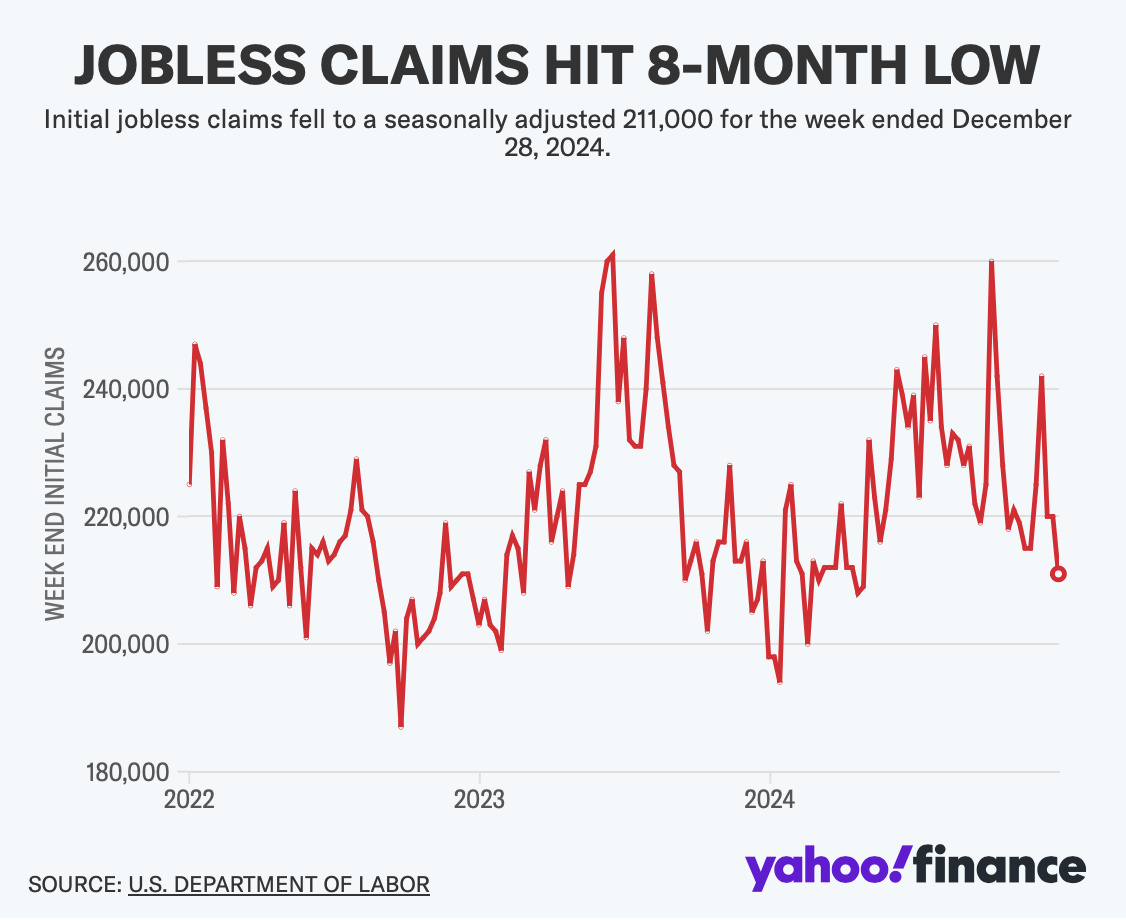

Unemployment claims have decreased. In the week ending December 28, initial claims for unemployment benefits fell to 0.211 million, down from 0.222 million the previous week. This indicator continues to remain at a historically relevant level in relation to economic growth.

(Image source: finance.yahoo)

Consumer sentiment has worsened. The Consumer Confidence Index from the USA Conference Board declined in December. Dana Peterson from the organization stated: "Although the decline was driven by weaker assessments of the current situation and expectations, the largest drop was in the expectations factor. Consumers' views on the current labor market conditions continue to improve, consistent with recent employment and unemployment data, but their evaluations of business conditions have weakened. Compared to last month, consumer optimism regarding future business conditions and income has significantly decreased in December. Additionally, following a cautiously optimistic view in October and November, pessimism regarding future employment prospects has returned."

Consumers feel better about the labor market. The December consumer confidence survey shows: "Consumers' assessments of the labor market improved in December. 37.0% of consumers reported that jobs are 'plentiful', up from 33.6% in November. 14.8% of consumers stated that it is 'hard to find' work, down from 15.2%."

Many economists are monitoring the spread between these two percentages (also known as labor market disparity), which reflects a cooling in the labor market.

Credit card data is facing a block. Data from JPMorgan shows: "As of December 21, 2024, our Chase credit card spending data (unadjusted) is up 2.1% compared to the same day last year. Based on the Chase credit card data as of December 21, 2024, our estimate for December retail sales from the US Census is 0.82%."

Mortgage rates are rising. According to data from Freddie Mac, the average 30-year fixed mortgage rate increased from 6.85% last week to 6.91%. From Freddie Mac: "Mortgage rates are inching toward 7%, reaching the highest point in nearly six months. Compared to the same time last year, rates have increased, and the headwinds for market affordability continue to exist. However, with the rise in pending home sales, buyers seem more inclined to withdraw."

There are 0.147 billion housing units in the USA, of which 86.6 million are owner-occupied, with 34 million units (or 40%) being mortgage-free. Among those carrying mortgage debt, nearly all have fixed-rate mortgages, most of which were locked in before rates soared from their 2021 lows. All of this illustrates that most homeowners are not particularly sensitive to changes in home prices or mortgage rates.

(Image source: finance.yahoo)

Home prices are rising. According to the S&P CoreLogic Case-Shiller Index, home prices increased by 0.3% in October compared to the same month. From Brian Luke of S&P Dow Jones Indexes: "Our national index has set a new record for the 17th consecutive time, with only two markets—Tampa and Cleveland—experiencing declines over the past month. The annual ROI continues to show positive inflation-adjusted returns, but is far from the annualized gains seen over the past decade. Markets in Florida and Arizona are rising but not keeping pace with inflation, with annual increases exceeding 10% since 2020. This has allowed other markets to catch up."

New home sales are rising. In November, new home sales grew by 5.9%, with an annualized rate of 0.664 million units.

Construction spending rose. In November, construction spending saw slight growth, reaching an annualized $2.15 trillion.

Manufacturing is doing better. From the S&P Global's December US Manufacturing PMI: "US factories reported a difficult conclusion to 2024 and amplified optimism about growth in the coming year. Due to disappointing inflow of new orders, the output in December rose at a reduced pace. Although in November, with the uncertainty of the elections passing, orders were almost stable, and customer demand rebounded, this respite proved temporary. Factories reported a lackluster sales and inquiry environment, particularly regarding exports. Many companies generally expect a rebound in business for the new year, with respondents hoping the new government will loosen regulations, alleviate tax burdens, and increase demand for US-made goods through tariffs."

The ISM Manufacturing PMI improved in December but continues to indicate a contraction in the Industry.

During perceived periods of stress, soft survey data often exaggerates more than actual Hardware data.

Most states in the USA are still growing. According to the Philadelphia Fed's November report: "In the past three months, the Index rose in 39 states, fell in 10 states, and remained stable in one state, with a three-month Diffusion Index of 58. Additionally, in the past month, the Index rose in 31 states, fell in 15 states, and remained stable in four states, with a one-month Diffusion Index of 32."

The short-term GDP growth forecast remains positive. The Atlantic Federal's GDPNow model shows an actual GDP growth rate of 2.4% in the fourth quarter.

Portfolio data outlook

The long-term outlook for Stocks remains positive, thanks to expectations for earnings growth. Earnings are the most important driver of stock prices.

Demand for Commodities and services is positive, and the economy continues to grow. Meanwhile, economic growth has normalized from the hotter levels of the early cycle. With significant tailwinds such as excessive job vacancies having subsided, the economy is less "curled up."

With strong Consumer and Business balance sheets supporting it, the economy remains very healthy. Job creation is still positive. The Federal Reserve—after addressing the inflation crisis—will focus on supporting the labor market.

(Image source: finance.yahoo)

Given the decoupling of hard economic data from soft sentiment-driven data, we are in a strange period. Consumer and business sentiment are relatively poor, even as tangible consumer and business activities continue to grow and reach record levels. From the perspective of investors, it is important that hard economic data continues to exist.

Analysts expect that the performance of Stocks in the USA may outperform the USA economy, largely thanks to positive operational leverage. Since the pandemic outbreak, companies have actively adjusted their cost structures. This involves strategic layoffs and investments in new equipment, including AI-driven Hardware. These initiatives are generating positive operational leverage, which means that moderate sales growth in a cooling economy is translating into strong earnings growth.

Of course, this does not mean we should be complacent. There will always be risks to worry about - such as political uncertainty in the USA, geopolitical turmoil, fluctuations in Energy prices, cyberattacks, etc. There are also terrifying unknowns. Any one of these risks could erupt and trigger short-term fluctuations in the market.

Another grim reality is that economic recessions and bear markets are developments that all long-term investors should expect to experience while accumulating wealth in the market. Always fasten the seatbelt in the Stock market.

At present, there is no reason to believe that the economy and market will face insurmountable challenges over time. The long game remains undefeated, and long-term investors can expect this to continue.