Source: Minsheng Securities

Author: Shao Xiang

How much longer can the USD rise? Is Trump really "not worried"?

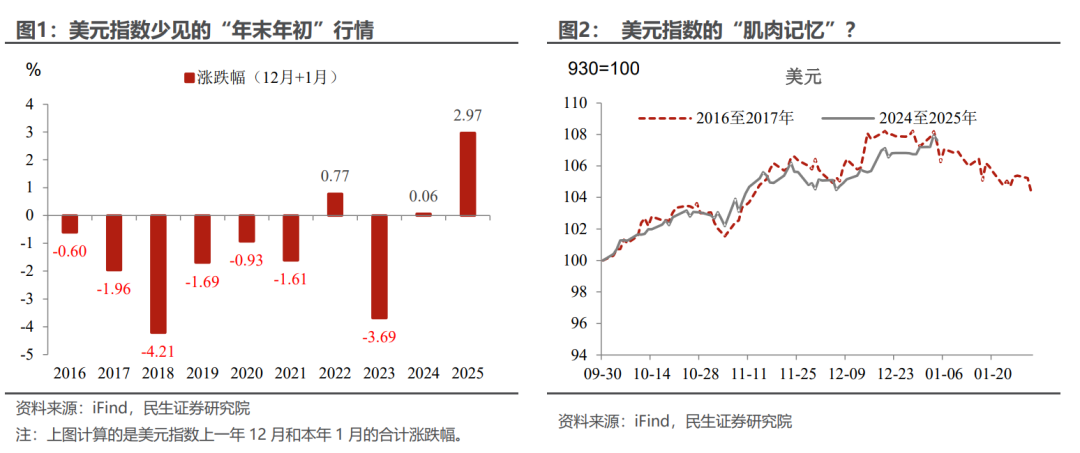

If we are to find the biggest contradiction in Trump's policies this year, it might be the "USD is the only option". Although Trump expressed his preference for a "weak USD" multiple times during his campaign, the market reaction shows that the USD has contradicted its typical weakness at the end of last year and the beginning of this year, with its increase since last December being remarkably significant (see Figure 1). How much longer can the USD rise? Is Trump really "not worried"?

Based on the "muscle memory" from 2016 to 2017, the USD may have already peaked. The USD may be one of the Assets that aligns most closely with the market during Trump's previous term (from October 2016 to January 2017). Interestingly, the USD actually peaked in early January 2017. Will the USD "repeat" the pattern of a spike followed by a decline?

Based on the "muscle memory" from 2016 to 2017, the USD may have already peaked. The USD may be one of the Assets that aligns most closely with the market during Trump's previous term (from October 2016 to January 2017). Interestingly, the USD actually peaked in early January 2017. Will the USD "repeat" the pattern of a spike followed by a decline?

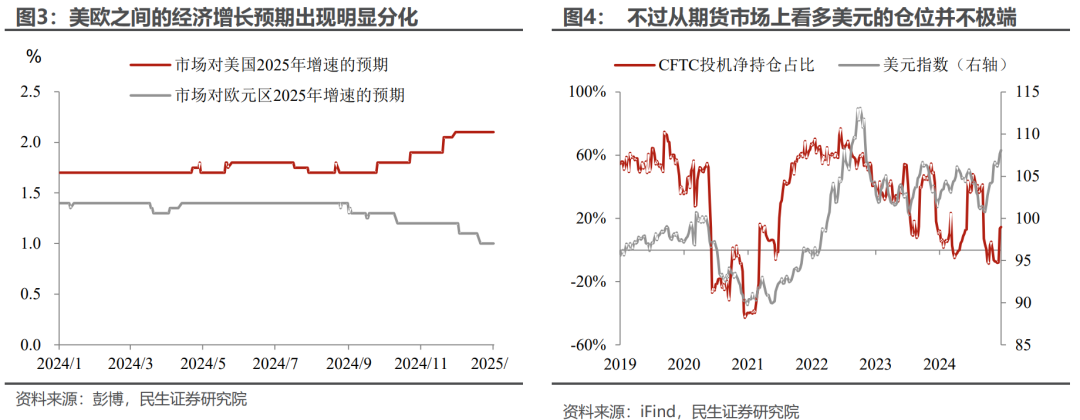

It is quite possible, but it will require some time and opportunity. There is no doubt that the current appreciation of the USD has the "timing and geographical advantage"; on the one hand, Trump's inauguration is just around the corner, and as long as policies have not yet been implemented, there is ample room for imagination—whether in terms of growth or inflation; on the other hand, as the biggest "competitor" to the USD, Europe is indeed not in a good situation, plagued by economic growth issues and uncertainties arising from the political instability in core countries like Germany and France.

Moreover, from the perspective of Futures positions, the current market sentiment towards going long on the USD is not extreme. The USD's turning point will still require some time. However, we believe that this point in time will not be too far off, and looking ahead, we consider the following main lines will become key macro clues for pricing:

First is the positioning under the macro narrative. The macro allocation narrative is not good at timing, but it can provide a certain reference and positioning for the current asset's price. Looking back over the past decade, a few points are relatively clear:

The upward shift of the USD central system reflects the changes in the Global landscape, which is difficult to reverse in the short term. After 2020, among major economies, both China and Europe are facing significant structural transformations, while the USA has better economic resilience after major stimulus, and currently does not have the conditions to reverse this pattern.$USD (USDindex.FX)$The conditions for breaking below 100.

The USD Index (narrowly defined) may also not have the conditions to break the 2022 high in 2025. The USD Index briefly reached a high of 114.8 in September 2022. At that time, there were at least three conditions that are not currently present: the Russia-Ukraine conflict and its impact on the Global Industry Chain and liquidity; the unprecedented acceleration of interest rate hikes by the Federal Reserve and the policy and personnel changes in China.

For the USD Index to refresh a five-year high in 2025, unless... Trump aggressively imposes universal tariffs globally, combined with the Federal Reserve reconsidering interest rate hikes. At least at present, the possibility of these two points "coming true" is not very high.

Secondly, behind the breakdown of Trump's new policy, there might also be a reluctance for the USD to be too strong. We certainly do not doubt the "label" of Trump's active fiscal policy, but under various "both-and" scenarios, at least in the early stages of governance, fiscal policy may show a counterintuitive relative tendency toward "tightening".

The core contradiction of Trump's policy lies in the emergence of different positive feedback mechanisms, ultimately leading to policy failure and market turmoil. For example, a strong USD may help solve the sustainability issue of US debt (with foreign investment buying US bonds), but seeking trade balance under a strong USD will bring more tariffs, leading to greater inflation expectations and higher long-term rates, which will further destabilize US bonds and impact stock markets and other markets.

How to break the deadlock? Solve the core issues. For Trump, apart from immigration, controlling inflation and stabilizing the US bond market may be the most important initial issues: on one hand, considering a shift to a relatively tight fiscal policy and a relatively loose monetary policy. The Federal Reserve cannot continue to shift hawkishly and must control the overall level of US bond rates; fiscal policy should make full use of the time window of the debt ceiling, with help from Musk's DOGE (Department of Government Efficiency) and support from not renewing some expiring short-term debts, to temporarily shift towards a relatively tight stance. A combination of tight fiscal policy and loose monetary policy is Bearish for the USD.

On the other hand, tariffs in exchange for "U.S. Treasury bond purchases" and avoiding depreciation of non-USD currencies. During the new term, tariffs could gradually become an important bargaining chip for the USA in negotiations, not only to secure imports from other countries but also to require non-USD economies to purchase more U.S. Treasury bonds to help stabilize the U.S. bond market, prompting non-USD currencies to avoid depreciation against the USD or even appreciate, achieving a comprehensive effect of trade rebalancing and reviving manufacturing, which is a decent option for the Trump administration.

Thirdly, observing the USD cannot be limited to just the USD. Non-USD, especially Europe and China, are likely to see marginal changes that are Bearish for the USD from the end of the first quarter to the second quarter: on one hand, positive or stabilizing signals may emerge from Europe's turmoil, including developments in the Russia-Ukraine situation, the German elections (February 23), etc.; on the other hand, China is likely to focus on preventing a persistent economic decline from the end of the first quarter to the second quarter.

In summary, our perspective on being bullish on the USD is cautious; a pullback after a rise in the USD is the "trend of the situation," and we expect this turning point to occur in the first quarter. The peak may be above 110, but it will not reach the highs of 2022. Of course, the USD's performance in the second half of the year may be more complex, which will require further tracking.

For the RMB, the rhythm in the first half of this year may also be somewhat different. This week, the RMB broke through the constraint of 7.30 against the USD, while the traditional Spring Festival foreign exchange settlement rush has not yet appeared. Generally speaking, in the past, the RMB exchange rate often showed characteristics of appreciation in the first quarter and increased pressure in the second quarter. This year, the situation may be the opposite; after overcoming the pressure period at the beginning of the year, the subsequent "landscape" will be quite different.

Risk Warning: Unexpected U.S. presidential term policies could lead to a significant cooling of the global economy, causing the USD to appreciate beyond expectations; geopolitical issues could create unexpected fluctuations, and liquidity problems may cause the USD to rise unexpectedly.

Editor/Rocky