科技巨头能否在 2025 年重复这一壮举?

科技巨头能否在 2025 年重复这一壮举?Source: US Stock Research Society

Author: Mark Hibben

"Will the highlights of Technology in 2024 continue?"

Due to AI and investor attention on the Magnificent 7, Technology once again stole the market spotlight in 2024.

Can technology giants replicate this feat in 2025?

Can technology giants replicate this feat in 2025?

Mark Hibben, head of investments at a well-known investment site, stated that major companies in the Technology industry will continue their success from 2024 this year.

$NVIDIA (NVDA.US)$Stocks rose by 180% when 2024 ended. Hibben mentioned that this chip company may continue to dominate its Datacenter and Consumer markets, predicting that stock prices will further increase in 2025. It is unclear how Intel will compete in the chip market and whether it will truly implement its Global Strategy.

Investors will also closely watch Google and its antitrust case. Hibben believes that a friendly resolution for this search giant may ultimately be reached. The market will focus on how Apple resolves tricky issues. Hibben expects Apple Intelligence to become clearer, stating that this could evolve into a bigger opportunity for this tech giant.

NVIDIA is still at the buy point.

Hibben's outlook for 2025 is as follows:

Regarding NVIDIA, it is clear that the company remains the tech darling of investors, and it seems this momentum will continue until 2025.

Mark Hibben stated that NVIDIA investors have many expectations for 2025. As NVIDIA's flagship product, the Blackwell AI accelerator goes into full production, the datacenter segment may continue its impressive growth. Additionally, NVIDIA may achieve sustained growth in the consumer market by releasing its new RTX 50 series standalone GPUs and a new series of ARM processors for Windows Copilot+ PCs, although the growth will be modest.

Regarding Data Center growth:

NVIDIA investors will naturally worry whether the explosive revenue growth in the datacenter field can continue until 2025. Especially since NVIDIA's guidance for its fourth quarter indicates a decline in growth rate. Considering this guidance, the revenue growth for the datacenter segment in the fiscal year 2025 (ending January 2025) will be only 137%.

Growth next year may slow down. Hibben is currently modeling revenue growth for the datacenter in fiscal year 2026 to be slightly above 50%. Demand for generative AI platforms for cloud and enterprise datacenters remains very strong.

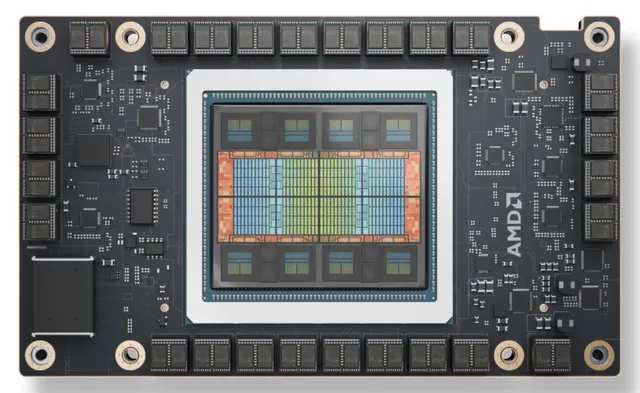

Next year, NVIDIA's competition will remain relatively weak at least in the first half; AMD will also offer AMD Instinct MI325X:

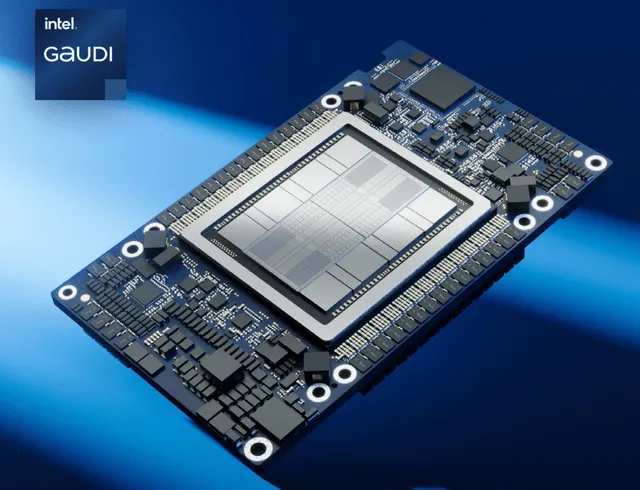

Intel will provide Gaudi 3:

The MI325X betrays its traditional role as a supercomputing accelerator, performing excellently in high-precision floating-point calculations. However, these numeric formats, 32-bit and 64-bit floating-point numbers, FP32 and FP64, are rarely used in AI. AI models have been gradually shifting towards increasingly lower precision numbers, such as FP16 and FP8, in this regard, Blackwell's performance surpasses its competitors:

These TOPS (Tera Operations Per Second) ratings provided by manufacturers represent theoretical maximum values. For operational AI performance, Hibben prefers to rely on ML Commons benchmark tests. However, few companies, except NVIDIA, publish their results on ML Commons. Google has published results for its custom tensor processing units (TPUs), and there are some inference results for AMD Instinct MI300X and Intel Xeon CPUs.

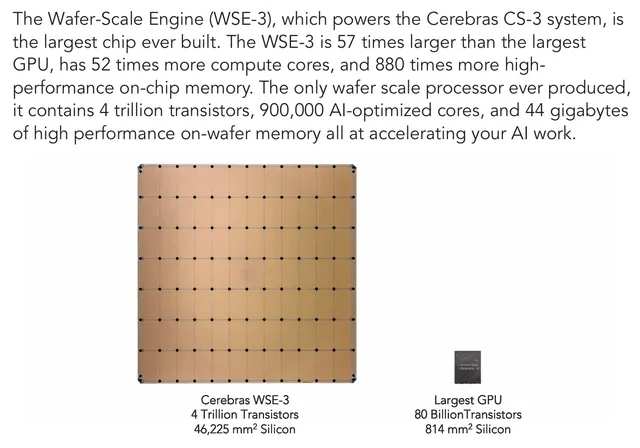

The lack of posts about AMD Instinct, Gaudi, or Intel Ponte Vecchio may better summarize the competitive landscape than the original TOPS ratings. NVIDIA's dark horse competitor is Cerebras (CBRS), which has also never published results on ML Commons.

Cerebras has created a "wafer-scale" GPU accelerator, claiming to have a huge size advantage over NVIDIA:

Cerebras chips are made by stitching together 84 different areas, which are typically separate devices during the photolithography process. This is a difficult process that has never been accomplished before.

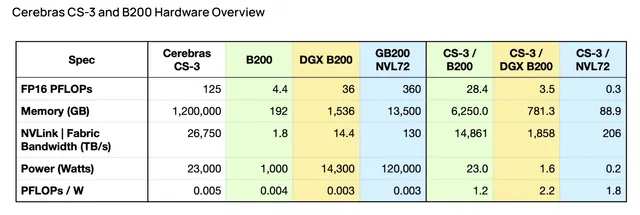

Cerebras also claimed in a blog post that it has a significant performance advantage over Blackwell:

The most comparable Nvidia system is a rack system composed of 36 Grace-Blackwell superchips (72 Blackwell B200), namely GB200-NVL72:

Compared to Nvidia's H100 "Hopper", the previous generation Cerebras processor CS-2 also boasts impressive performance. So, why hasn't Cerebras monopolized the market?

It may be due to the cost of the system. Constructing a traditional GPU on a wafer may be significantly cheaper than combining all these GPUs so that they can operate together as a single chip on the wafer.

Cerebras submitted an IPO on October 1. In the filing, they disclosed that their revenue for the first six months of 2024 was only 0.1364 billion USD, with a loss of 66.6 million USD. Therefore, Cerebras may need at least a few years to make its wafer-level chips profitable. Until then, it cannot afford to manufacture many.

At this year's Computex, AMD revealed that the MI350 series will debut in 2025, but no exact details about the new series' timing or performance were provided. This outlines the competitive landscape for 2025. It's no wonder that Nvidia stated in October that Blackwell is "sold out" for the next 12 months.

Regarding the growth of the consumer market:

Given the explosive growth in Datacenter revenue over the past few years, it’s easy to overlook the fact that Nvidia's other segments have been growing at a healthy pace. Nvidia reported that its revenue from consumer GPU add-in boards was well received by gamers, growing 15% in fiscal year 2024, and may be roughly the same in fiscal year 2025.

Nvidia is about to launch a new series of graphics cards called the RTX 50 series, with the RTX 5090 replacing the now outdated RTX 4090 as the flagship. Of course, critics often complain in advance about how expensive these cards might be.

But Nvidia is simply doing what any well-run business should do: charge what the market will bear. Nvidia dominates PC gaming to the extent that AMD's Senior Vice President and General Manager of Computing and Graphics Business Group, Jack Huynh, stated in an interview with Tom's Hardware's Paul Alcorn that AMD is moving away from competing with Nvidia in the high-end GPU space. Alcorn asked Huynh:

There’s a lot of anxiety in the PC enthusiast Community, as people are so focused on AMD's creation of Datacenters and your success, that the focus on gaming will diminish. There are even multiple different sources repeatedly spreading rumors that AMD may not be that committed to the high-end market for enthusiast GPUs, that it may lean more toward the mid-range market, and may not even have a flagship SKU to compete with Nvidia’s top models. Are you committed to competing at the top of the stack with Nvidia?

Huynh responded:

I'm focused on scale, and AMD is in a different position right now. We have a lot of these discussions at AMD, right? So the question I ask is, PlayStation 5, do you think that hurt us? It’s priced at $499.

So, I ask, is it fun to go to King of the Hill? Similarly, I am looking for scale. Because when we achieve scale, I will bring in developers.

Therefore, my current priority is to scale up, so we can faster reach the 40% to 50% market. Am I pursuing a 10% TAM (Total Addressable Market) or 80%? I am an 80% person because I do not want AMD to be a company where only those who can afford Porsche and Ferrari can buy from. We want to build gaming systems for millions of users.

Hibben believes Huynh's argument is somewhat specious. He stated that he owns an RTX 4090 and enjoys playing Cyberpunk 2077 at 8K in 2077, but does not own a Porsche or Ferrari.

Considerations of market share are not without reason. According to data from Jon Peddie Research via Tom's Hardware, as of the first quarter of 2024, NVIDIA's share of the add-in board market is 88%. According to the Steam Hardware Survey as of August, 76.5% of Steam users own an Nvidia GPU.

In fact, Hibben believes that AMD has shifted its resources to datacenter work and minimized investment in gaming GPUs. The RTX 50 series will once again see competition from AMD. Or for that matter, from Intel. The latest "Battlemage" GPU released by Intel on December 3 has been praised by critics for its value, but no one claims they will compete in the high-end market.

In consumer GPUs, Nvidia stands out again in the high-end market. The RTX refresh will undoubtedly stimulate sales and growth next year. It is believed that Nvidia is preparing to enter $Microsoft (MSFT.US)$ the Copilot+ PC market.

Nvidia has long had a range of SOCs (System on Chip) that utilize ARM architecture, CPU cores, and its own GPU architecture. These are primarily targeted at robotics and automotive driver assistance as well as self-driving. Given their powerful GPU and AI capabilities, these seem to be ideal choices for the next generation of AI PCs.

About a year ago, rumors regarding this matter first emerged, and a recent report on October 31 confirmed that Nvidia plans to release ARM-based consumer SOCs for Windows PCs by September 2025.

This could significantly expand its ARM SOC sales, but Nvidia will not own this market outright. It will face fierce competition from$Qualcomm (QCOM.US)$, AMD, and Intel. However, Nvidia will have a strong advantage in its onboard GPU and AI capabilities.

Overall, Hibben expects revenue and profits in the datacenter and consumer-driven markets (such as gaming, PCs, and Autos) to continue to grow. He stated to remain bullish on Nvidia and rates it as a Buy.

There is still a considerable uncertainty regarding Intel.

On the other side is $Intel (INTC.US)$ With the departure of CEO Pat Gelsinger, the company is in deep trouble.

Regarding the next steps, Mark Hibben stated: While some believe firing Gelsinger was a mistake, he might even return; no matter what happens to Intel in the future, I am certain Gelsinger will not return to the company.

Intel investors should assume that the Board of Directors did not act capriciously when dismissing Gelsinger, despite investors knowing nothing about the reasons. This lack of transparency is a persistent issue in Intel's corporate culture that the next CEO needs to correct.

Investors and Analysts need to sift through existing data to derive a viable hypothesis regarding Gelsinger's dismissal and Intel's future prospects.

Most of the data is indisputable: compared to Intel's relative stagnation, NVIDIA's disruption in the datacenter and its massive growth in datacenter revenue. NVIDIA's third-quarter datacenter revenue was $30.77 billion, overshadowing Intel's total revenue of $13.284 billion in the third quarter.

These facts clearly illustrate the failure of Intel's own datacenter GPU accelerator, Ponte Vecchio (now known as Datacenter GPU Max 1550). It was released in 2022, meant to be timely, and could have captured a significant market share in the datacenter AI market. However, Intel no longer even lists it in its processor data profile, which is odd considering that processors usually have a lifespan of several years.

The latest Gaudi 3 AI accelerator also falls short. As reviewed above, its specifications suggest that it is entirely inadequate to compete with Blackwell or even MI325X. This leaves Intel with nothing to offset NVIDIA's advantages and only limited competition against AMD until its next generation of GPUs (referred to as Falcon Shores) is released sometime in 2025.

In March 2023, Intel updated its Datacenter GPU roadmap, indicating that Falcon Shores will be postponed from 2024 to 2025. Intel has made significant commitments to Falcon Shores:

However, Intel made similar commitments to Ponte Vecchio but failed to deliver and was delayed. Hibben will not bet on Falcon Shores to stop the Datacenter bleeding.

In the development of advanced Semiconductors processes and Intel Foundry, the situation is less clear but equally frustrating. From all angles, Intel is sticking to Kissinger's route and suggesting that '5 nodes in 4 years' is 'on track.'

At least this is what Intel seemed to communicate during UBS Group's Global Technology and AI Conference in December, where interim co-CEO David Zinsner and Chief Global Operations Officer and General Manager of Foundry Manufacturing Naga Chandrasekaran were interviewed at the conference. Zinsner first said:

. . . The Board of Directors is very clear that the core Global Strategy remains unchanged. We still aspire to be a world-class foundry. We aim to be the leading Western supplier of chips for customers, which remains our goal. But we also understand that success for the largest customer of the foundry is crucial for the foundry's success. Therefore, the Board of Directors also wishes to focus on execution in the Business product area to ensure that the foundry business remains successful.

Hibben believes this should be qualified as 'the core strategy temporarily remains unchanged.' Or until Intel finds a new CEO. Interestingly, Zinsner seems to place the burden of generating more sales on the Products group. However, in the third quarter, nearly all operational losses from business departments came from the foundry business.

Intel's foundry strategy has a real problem, which is a lack of cost competitiveness compared to other mature foundries.$Taiwan Semiconductor (TSM.US)$Intel is still catching up with advanced processes, which is futile. At this point, eliminating Intel's 20A process leaves it with no choice but to use Taiwan Semiconductor's "3 Nanometer" N3 process for its latest Lunar Lake Copilot+ PC processor and Arrow Lake desktop processor.

In terms of process node development, Chandrasekaran is far less optimistic than Gelsinger. Tim Arcuri from UBS Group asked:

However, can you talk about the position of 18A and where you think it needs to intersect with the second half of 2025? B, what I am hearing from some customers, or some potential foundry clients is that 18A still leans more towards HPC. As a broadly foundry node, customers I spoke with think 18A is good, and if you have an HPC application, then 14A might be the node that is more broadly applicable to external foundry clients. Can you discuss that as well?

Chandrasekaran answered the first part:

So, when Pat announced that defect density D0 was less than 0.4, it was a point in time indicating we are progressing as expected. If I look at it today, we are making progress. We have achieved several milestones, and many milestones remain for technological development. If I put on my technology development hat for a minute, there are always challenges when introducing new technology, with ups and downs. But I want to say that there is nothing fundamentally challenging at this node.

What needs to be addressed now is to tackle remaining yield challenges, defect density challenges, continue to improve it, and increase the process profit margins. Will there be challenges? Yes, but I believe we are making progress. Next year, in my opinion, mainly in the first half, we will deliver engineering samples of the node to our customers for feedback and begin a ramp-up point in Oregon. In the second half of 2025, our milestone is to certify the node, upgrade capacity in Arizona, and make the products available for customers to purchase. These are the milestones we are working hard to achieve all of these next year. This is critical for us.

Notably, in the reply, Chandrasekaran never used the term 'expected' to describe the preparedness of 18A. Instead, he stated that they have production targets, which include sampling in the first half of 2025, followed by a production increase in the second half. At the same time, he acknowledged that there are still challenges with yield and defects.

So, does Intel have an 18A node that can generate sufficient output in production volume, making it a viable manufacturing process? At this point, Hibben believes the obvious answer is no.

Regarding the second part of the question, Arcuri seems to know that potential customers are already dissatisfied with 18A and have postponed any commitments until 14A is ready. Chandrasekaran continued to say:

It [18A] can benefit mobile devices based on how the design is completed, but since customer engagement happened later, it does not address the full TAM. And for 18A, our largest customers in the next two to three years will still be Intel products, which goes back to what Dave said. For Intel products, we know the demand, we know what needs to be done, our focus is on scaling it and continuing to get more customers to use 18A. But all these learnings have been integrated into 14A.

Therefore, with the advent of 14A, it will enter a broader market that includes computing, mobile, and other applications, as well as the way PDK is completed, making it applicable not only to Intel Focus but also to a broader ecosystem adopting 14A and applying it to their designs.

Chandrasekaran admitted that there are not many customers for Intel's 18A, but it is expected that there will be more interest in 14A. When will 14A be ready? He did not say.

In the development of process nodes, what matters is what manufacturers can provide in terms of large-scale production, rather than what they can showcase in marketing presentations. Chandrasekaran candidly admitted that Intel faces challenges in fully ramping up 18A for production. However, he is also constrained by management expectations, which prevent him from acknowledging an obvious fact: 18A may not be ready for large-scale production next year.

Hibben boldly makes some inferences and predictions. Inferring that the Board of Directors has asked Chandrasekaran to deliver large-scale production by the end of 2025 is not because they are satisfied with the progress of the process node but because Intel has already invested a significant amount in advanced processes and manufacturing.

Hibben predicts that if 18A does not go into large-scale production next year, the Board of Directors will cancel the Foundry strategy simply because it sees no way to become competitive. Some might say that this is premature and shortsighted, but without any signs of returns, Intel's bottom line may not sustain a foundry strategy for more than a year.

This does not necessarily mean that Intel will abandon advanced manufacturing. Hibben has pointed out that Intel's efforts to become a foundry have actually lowered its manufacturing efficiency in the short term. However, there will certainly be a very strong monetary temptation to move away from Foundry and towards a fabless model.

The results will prove everything over time. Hibben continues to give it a Sell rating based on Intel's poor financial performance and uncertain future.

Google's antitrust case has both pros and cons.

$Alphabet-C (GOOG.US)$ The antitrust case is a significant development for the company, especially with considerable implications for its evolution as a search giant in 2025 and beyond.

Mark Hibben: It is difficult to predict how the incoming Trump administration will handle the antitrust lawsuits initiated by the Biden administration. Generally, conservatives are hostile to business regulation.

After Google's defeat, the U.S. Department of Justice has requested quite harsh remedies, including the breakup of the Android operating system and Chrome browser, as well as the termination of "exclusive deals" with companies like Apple.

Hibben pointed out that Google's dissolution is unlikely to be approved:

Although a breakup of Google may be attractive to competitors, I do not believe it will happen. The issue here is that it is difficult to prove that a breakup along reasonable organizational lines would effectively weaken Google's dominance in search and search text advertising.

As free products, Chrome and Android are entirely reliant on Google's search revenue. I pointed out:

The fundamental issue here is that separating the search business from other Alphabet businesses would only relieve the search business from the financial burden of supporting other Alphabet businesses. The Search can freely use its massive revenue to maintain its dominance.

Any derivative scenario that could be fabricated would ultimately run into the same dilemma. While user tracking in search is enabled in Chrome, it does not require Chrome, as tracking can be done through any cookie-supporting browser. Moreover, Google Analytics may provide most of the user tracking that Google needs.

While it is not surprising that the Justice Department is seeking a breakup, Hibben believes it will not be approved when the remedy phase begins next August, anyway. Under the Trump administration, the Justice Department may concede on break-up remedies, but will still seek behavioral remedies that he believes could be implemented:

I believe that the court will mainly focus on behavioral remedies, such as abolishing the RSA (Revenue Sharing Agreement), rather than a breakup which could be said to harm consumers. Auction pricing may also be restricted because it is clearly an abusive behavior. Suggestions that Google does not favor its own services in search results may also be adopted.

Financially, the most effective remedy is to abolish RSA, so let's take a look at this. The cost report for the RSA (including Apple) is reported as Traffic Acquisition Cost - TAC. According to Alphabet's 2023 annual report, the TAC for the 2023 fiscal year is 50.866 billion dollars, accounting for 29% of search advertising revenue.

Abolishing RSA will effectively save Google about 50 billion dollars in costs each year. Users need to make a choice from the options menu during the initial setup on their device or browser, rather than from the default positions in the browser and the Android home screen.

In the process, Google may lose some search share, but would it lose about 30%? This is a difficult question to answer, but it is believed not, at least while competitors remain relatively weak.

Over time, competitors might gain market share. Apple, being deprived of the motivation to do nothing, may seek to develop its own search engine. Additionally, against the backdrop of operating systems supporting AI in the future, search and generative AI are inseparable. Apple may integrate search as part of its broader AI strategy.

Therefore, in the short term, it is doubtful whether Google will suffer financially from the lack of RSA. It has lost a certain percentage of search revenue but offset by recovering TAC fees. In the short term, it is believed Google will be ahead, although revenue will decline year-on-year.

Given that RSA is viewed by some as an illegal "exclusive deal" contract under Sherman, Hibben at least does not believe the judge will approve such a remedy. Of course, unless the new Department of Justice simply takes action to dismiss the case. He continues to rate Google as "Hold," but may upgrade it to "Buy" depending on the disposition of the soon-to-be-inaugurated government.

Apple's AI advantage.

Finally, how Apple will respond to tricky questions in 2025 and beyond and the view on Apple and its AI work.

$Apple (AAPL.US)$ Apple has been diversifying its manufacturing to places like Vietnam and India, and may accelerate this process regardless of tariffs. However, Apple's contract manufacturer, such as Fujifilm Holdings Corporation Unsponsored ADR, has made substantial infrastructure investments in mainland China. Moving all manufacturing out of China may take years.

It remains uncertain how Apple will respond to the direct impact of tariffs. Apple's profit margins are not large enough to absorb the full cost of a 60% tariff, so most of this cost must be passed on to consumers.

He believes the Trump administration is likely to exempt consumer electronics again, rather than face the political consequences of significant price increases that would fall on consumers. Trump vowed to curb inflation price hikes from the Biden era, and significant price increases in consumer electronics would be contrary to this goal.

Regarding Apple's AI efforts:

As an Apple developer, Hibben invested in the high-end versions of the latest M4 Max MacBook Pro, M4 iPad Pro, and iPhone 16 Pro Max, enabling exploration of Apple Intelligence (referred to as AI) on the best Apple devices.

Most AI features are implemented on-device and do not require an Internet connection. This aligns with Apple's emphasis on privacy and security, but it limits what AI can do. Apple has delivered all AI features it promised to launch by the end of this year at WWDC. The main outstanding work is the cloud-based version of Siri using generative AI.

These features also work, but are generally not impressive. Smart phones (even iPhones) can only accommodate so many smart capabilities. Users looking for features like Microsoft Copilot or Google Gemini may feel disappointed.

However, it is unreasonable to compare these huge cloud-based generative AI models with what Apple has done on-device, although consumers may do so regardless. This could be a potential issue for Apple. Consumers may not care about this distinction.

Apple is making a long-term bet that it can weave AI on devices and based in the Cloud into a seamless whole that "just works." Microsoft is also trying to combine device-based AI with Cloud-based AI in its Copilot+ PC.

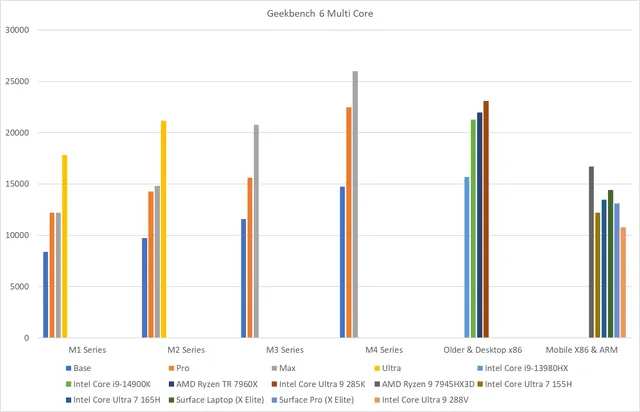

Apple's main advantage in this area is Apple Silicon, which continues to make significant progress compared to competitors, whether using ARM or x86 architecture. According to Geekbench results, Apple's M4 Max CPU outperforms the latest Intel Lunar Lake and Arrow Lake processors in multicore CPU benchmark tests:

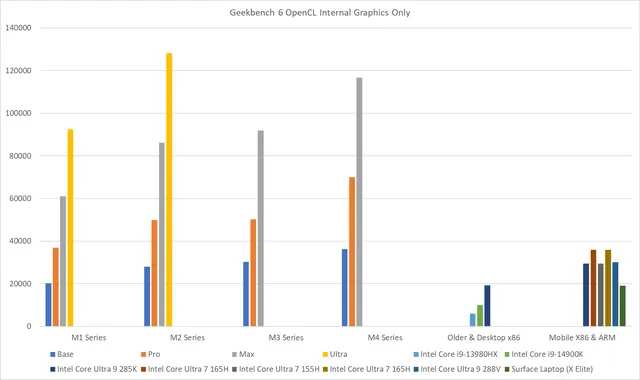

Apple's integrated graphics have also been tested to far outperform competitors in the Geekbench OpenCL benchmark test:

Hibben has personally confirmed these results on his 16-inch MacBook Pro, which is equipped with the M4 Max processor. The integrated graphics results are particularly relevant because the GPU portion can be used for AI computation.

The biggest problem currently with Apple Intelligence is that Apple requires it to be backward compatible with the M1 series, which means it cannot take advantage of the processing power offered by the M4 series Macs.

Fortunately, Mac users are not limited to Apple's device-side AI; they can also utilize open-source AI models that can be downloaded through the MIT-licensed AI platform, Ollama. Hibben has used Ollama and found that it can even run the very large 405 billion parameter Llama 3.1 model on a MacBook Pro.

Therefore, his conclusion is that the latest Apple Silicon Macs are excellent platforms for device-side AI, even if Apple Intelligence does not fully utilize them. As Apple Intelligence software matures and evolves into more powerful platforms in the future, users will find its capabilities increasingly powerful and useful.

The powerful capabilities of Apple Silicon also hint at the imminent release of a server-based intelligent version of Siri next year. This new Siri will run on Apple Silicon-based cloud servers, which could become Apple’s secret weapon in competing against Google and Microsoft's cloud-based AI.

Hibben still expects that the ultimate goal of Apple's Intelligence is a new AI-based user interface, where nearly all computer interactions are mediated by AI on the device.

These are the 'agent' functions that Microsoft and Google refer to, allowing AI to perform operations on the device on behalf of the user. However, both companies are very cautious with their agent approaches, as allowing cloud-based AI to control users' local devices clearly presents security risks.

If AI is hosted on the device, these security issues typically disappear. Siri already has more agent capabilities than Microsoft or Google might have imagined. Users can simply ask Siri to turn on WiFi or start an application. The voice response is very reliable, and everything happens on the device.

A smarter Siri will use Apple's secure server approach, enabling it to process user queries in the cloud when necessary. User data is always sent in an encrypted manner and is never stored after processing the queries.

Ultimately, Hibben hopes that Siri will become a fully functional user interface capable of handling almost any function that users traditionally perform on their devices. Apple has once again pioneered a new computing interface that cloud-based AI cannot achieve, without exposing users and local devices to the risks of privacy breaches or, worse, malware attacks.

Although the launch of Apple Intelligence may not have gone smoothly, it could have a bright future, allowing continued bullish sentiment on Apple and rating it as a Buy.

Editor/Rocky