尽管仍有投资者担忧市场涨势过于集中的风险,但瑞银认为,

尽管仍有投资者担忧市场涨势过于集中的风险,但瑞银认为,UBS Group believes that while large Technology stocks continue to see earnings expansion, their valuation growth is slowing down, making them "cheaper" compared to the overall market, and this trend is expected to continue, hence there is still room for appreciation.

Looking back at the U.S. stock market in 2024, large Technology Stocks once again dominate. Does this mean that the concentration of the upward trend will still be a significant threat to the U.S. stock market?

The UBS Group strategy team stated in a Research Report released on January 2 that in 2024, leading Technology stocks will continue to drive market growth. The top 6 weighted stocks are expected to achieve an ROI of 48% in 2024, contributing to$S&P 500 Index (.SPX.US)$a 9% increase over the past year, while excluding these 6 stocks, the remaining S&P 500 Index constituent stocks have shown only a 16% increase year-to-date.

Despite remaining investor concerns about the risks of a too concentrated market rally, UBS believes that considering the significant upward revision of the earnings growth expectations for leading Technology Stocks next year, and the notable slowdown in their valuation growth compared to the market, there is still potential for upward movement.

Despite remaining investor concerns about the risks of a too concentrated market rally, UBS believes that considering the significant upward revision of the earnings growth expectations for leading Technology Stocks next year, and the notable slowdown in their valuation growth compared to the market, there is still potential for upward movement.

With strong earnings momentum and relatively low valuations, leading Technology Stocks are expected to continue rising.

The report shows that over the past decade, the growth in the S&P has become increasingly concentrated, with the six largest stocks by market capitalization now accounting for 31.2% of the total market value, a significant increase from 11.2% in 2013.

The market is clearly concerned about the trend of the rally focusing on the leading Technology stocks. According to the report, the average Shareholding reduction ratio of Large Cap stock portfolios against six major indices exceeds 6%, with only the reduction ratio for Google's parent company Alphabet being below this level.

However, the report also adds that in the past year, the contribution of large Technology stocks to the rise of the US stock market (38.9%) far exceeds that of other individual stocks (5%), while the valuation increase (5.8%) is actually lower than that of other individual stocks (8.6%). This means that large Technology stocks are becoming 'cheaper' compared to the overall market as their earnings continue to expand while valuation growth slows.

Even excluding Technology stocks, the US stock market still appears very expensive. The report shows that vertically, the current PE of the S&P 500 Index is 21.5 times, about 1.5 standard deviations above the historical average; horizontally, the valuation premium of the S&P compared to the Non-US Developed Markets Index (EAFE) continues to widen.

At the same time, regarding the expected factors that most impact ROI, the report states that the market generally expects the EPS growth rate of the six major Technology stocks (19.1%) to continue outperforming the Large Cap average (10.8%) next year, and still far exceed the average level of the past 30 years (5%).

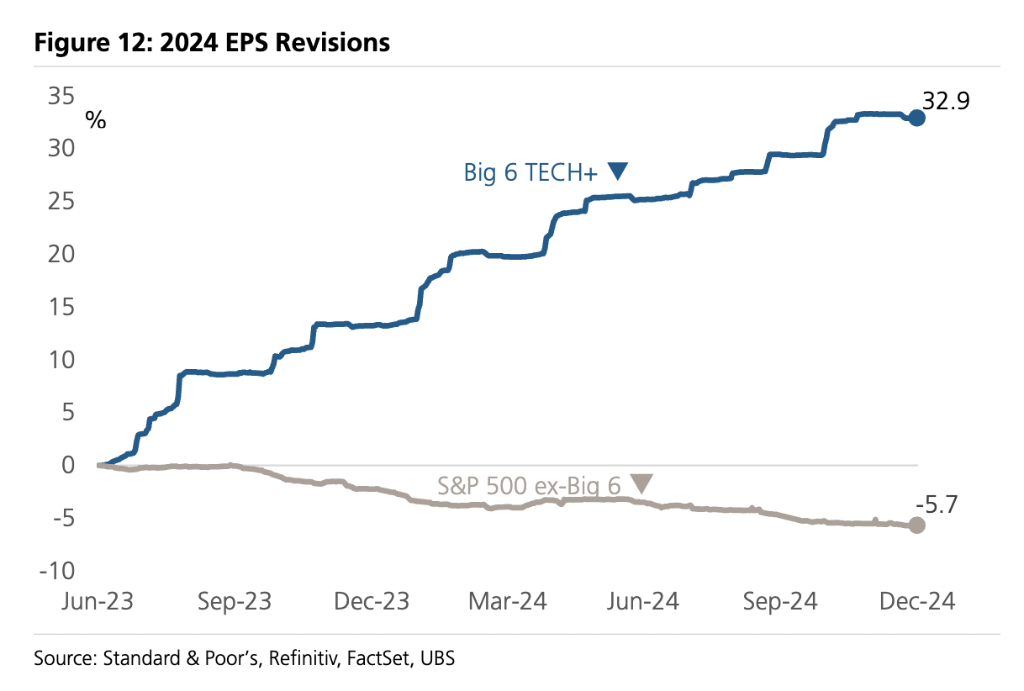

Since 2024, earnings expectations for the six major Technology stocks have been continuously revised upward, while those for other sectors have been steadily declining, and UBS Group expects this trend to continue through 2025.

Overall, the report believes that strong economic growth, better-than-expected earnings, a narrowing credit spread, and an increase in valuations all support the market's rise in 2024.

Although some investors worry about the market being overheated, the report believes that this concern may be exaggerated. Even compared to the dot-com bubble period, based on current economic and market data, US Stocks still have room for growth, and 2025 is expected to be "another strong year."

Editor/Rocky