12月30日,信达证券固收首席分析师李一爽发布研报称,

12月30日,信达证券固收首席分析师李一爽发布研报称,Xinda Securities believes that the recent pricing of the 10-year government bond yields reflects the potential for a decline in the OMO rate next year. Based on the economic outlook and monetary policy environment for 2025, it is anticipated that a reduction of 50 basis points in the OMO rate may be necessary to achieve a marginal easing similar to that of 2024, which suggests that the 1.7% yield on the 10-year government bonds does not appear to be overly priced.

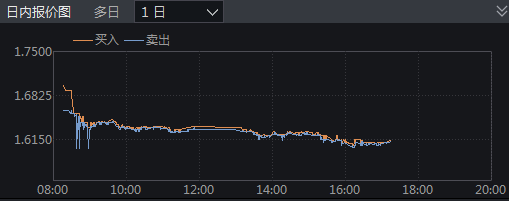

Recently, the bond market has continued to be strong, with today's government bonds futures and spot prices rising across the board. As of the close, the 10-year government bond active bond (240011) decreased by 5.15 basis points to 1.6125%.

As long-term interest rates enter an 'uncharted territory', particularly after the central bank once again highlights the interest rate risk, some investors still harbor concerns regarding potential adjustment risks: what exactly is currently priced into the 10-year government bond interest rate? Is there a risk of a correction in the bond market after the start of the year?

On December 30, Li Yishuang, Chief Analyst of Fixed Income at Cinda Securities, released a research report stating that the 1.7% 10-year government bond interest rate seems 'not to be overvalued'. If monetary policy is to achieve a degree of marginal easing similar to that of 2024, the OMO (7-day reverse repo operation) interest rate may need to be reduced by 50 basis points.

On December 30, Li Yishuang, Chief Analyst of Fixed Income at Cinda Securities, released a research report stating that the 1.7% 10-year government bond interest rate seems 'not to be overvalued'. If monetary policy is to achieve a degree of marginal easing similar to that of 2024, the OMO (7-day reverse repo operation) interest rate may need to be reduced by 50 basis points.

A report published by Shanghai Securities News last month, titled 'Bond Fund Investment Seeking New Anchors', quoted Zhu Run Investment's analysis, stating that based on the bond market pricing habits since July, the 10-year government bond interest rate has generally been judged with OMO plus 40 to 50 basis points as the phase interest rate lower limit. In the future, a rough benchmark of 'OMO rate + 45 basis points' can be considered a new pricing anchor for the bond market.

This implies that, based on the current OMO rate of 1.5%, if the future reduction reaches 50 basis points to 1%, then the pricing of the 10-year government bond at 1.7% may still fall within a reasonable range.

In September, the policy logic shifted, opening up the imagination for monetary easing.

In a Research Report, Cinda Securities stated that looking back at 2024, the core contradiction in the Bonds market is between the market's expectation of significant policy easing and the reality of gradual policy adjustments.

The report indicated that since March, the central bank has continuously signaled that market interest rates are declining too rapidly, even directly selling long-term Bonds to intervene in market expectations, but the downtrend of long-end rates has not been reversed. The significant reduction in policy rates in Q3 marks that the core contradiction in the bond market ultimately converges as policy aligns with market expectations.

This means that the downtrend in long-end rates and the lag in policy adjustments reflect a change in the economic model - the previous model, which relied on real estate to drive economic growth, is increasingly unsustainable.

After September 2024, a noticeable adjustment in policy logic occurred, confirmed at the end-of-year Central Economic Work Conference, and the report believes this change opens up new possibilities for monetary policy.

The Central Economic Conference has prioritized comprehensive expansion of domestic demand for next year’s work, but the emphasis on investment efficiency suggests that the process of expanding domestic demand is unlikely to follow the old path of relying on large-scale investments; the focus may shift towards increasing residents' consumption capacity to support Consumer spending. Its statements regarding fiscal policy generally align with expectations, but the tone of monetary policy has been adjusted for the first time since 2010, showing that the central authority also recognizes the need for greater easing of monetary policy.

From Cinda Securities' perspective, it is indeed necessary and feasible to further relax the current monetary policy in our country.

The report believes that in recent years, the potential to unblock the interest rate transmission mechanism has been fully utilized following the reduction of self-discipline upper limits on deposit rates, the prohibition of manual interest supplementation for high-interest deposit attraction, the alignment of interbank deposit rates with OMO rates, and the reduction of existing mortgage rates. If the marginal loosening of monetary policy in 2025 is to remain roughly similar to that of 2024, a greater reduction in policy rates will be necessary.

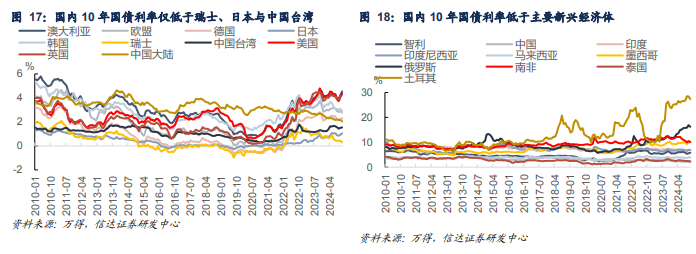

The report indicates that although current domestic long-term bond rates are only higher than those in the Swiss Franc, Japan, and Taiwan, domestic inflation is currently lower than in these developed economies, and the RMB exchange rate is also more stable compared to most emerging economies. This suggests that domestic monetary policy has the capacity to expand its loosening efforts— the previously cautious policy stance was more a matter of path dependence, and if the policy logic has reversed, there is hope for continued reduction in policy rates before significant improvement in domestic inflation.

Long-term bond yields are declining: the market anticipates further reductions following OMO.

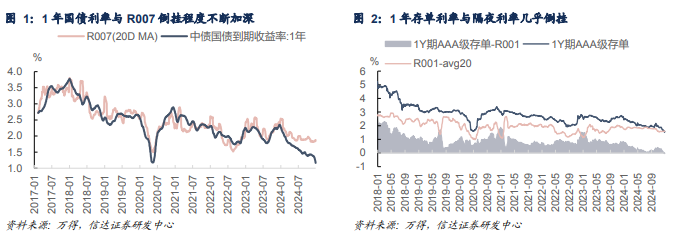

Based on the above, the market already has basic expectations for the loosening of monetary policy. In 2024, declines in various types of bonds are nearly all over 80 basis points, with only the reductions in OMO rates and R007 being relatively minimal. This reflects the market's expectation for further OMO reductions, and on the other hand, it also shows that funding costs have now become the largest constraint on the general decline in interest rates.

Therefore, the report believes that the yield on 10-year government bonds may exceed 1.7% by the end of 2024, which to some extent has already priced in the space for OMO rate reductions in 2025.

In other words, Cinda Securities believes that further loosening of monetary policy in 2025 is an inevitable trend, and the implementation of easing policies is merely a matter of time. Even if funding prices do not loosen as expected by the market after the cross-year period, a directional reversal in market expectations would also be difficult to achieve.

Looking ahead to 2025, the report predicts that the drag on the economy from declining real estate sales may converge marginally, but the support for the economy from manufacturing and infrastructure investment, after sustained expansion, can hardly continue to grow. Additionally, external demand for the economy will also weaken. Although consumer spending can offset the decline in demand to a certain extent, it may also struggle to drive the economy into a self-sustaining upward cycle in the short term.

In this context, Xinda Securities believes that if the monetary policy is to achieve a marginal easing similar to that of 2024, the reduction in OMO rates may need to reach 50 basis points. From this perspective, the decline in the 10-year government bond yield to 1.7% in December, although occurring too quickly, does not seem to be excessively priced in terms of magnitude.