然而,

然而,HSBC believes that a "just right" economic environment may emerge in the first half of 2025. The market breadth of the S&P 500 Index has significantly decreased, and historical experience suggests that this may be a contrarian indicator, indicating that the market adjustment is nearing its end.

In December, the Federal Reserve's hawkish stance triggered market fluctuations, but HSBC stated not to panic, as this could be the biggest "bargain" opportunity in 2025.

On January 2, a research report titled "What You Might Have Missed" was released by HSBC, where Analyst Max Kettner and others indicated that since the Federal Reserve cut rates last month, US Treasury yields have surged, the US dollar has strengthened, and the market has entered what is called the "Danger Zone" mode.

However, a "just right" economic environment may emerge in the first half of 2025. The market has been too conservative in its expectations for Federal Reserve rate cuts, predicting only one cut in the first half, which may need to be reassessed.

However, a "just right" economic environment may emerge in the first half of 2025. The market has been too conservative in its expectations for Federal Reserve rate cuts, predicting only one cut in the first half, which may need to be reassessed.

HSBC believes that short-term market fluctuations will create attractive buying opportunities for USA Treasury Bonds and risk assets. Over-sold "Bond Proxy" Assets, Bank of America stocks, Technology stocks, and Emerging Markets hold potential opportunities.

What has happened in the market over the past few weeks?

HSBC pointed out that the Federal Reserve exhibited an unexpectedly hawkish stance at its December 2024 meeting, driving up US Treasury yields and strengthening the US dollar. This change triggered what is called the "Danger Zone" phenomenon, causing almost all asset classes to be affected to varying degrees.

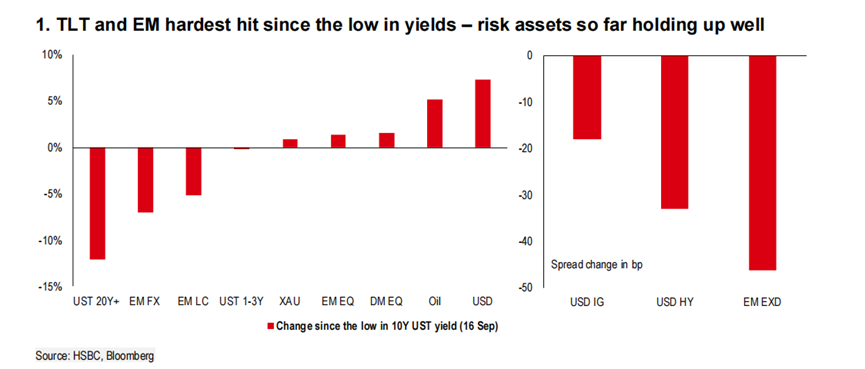

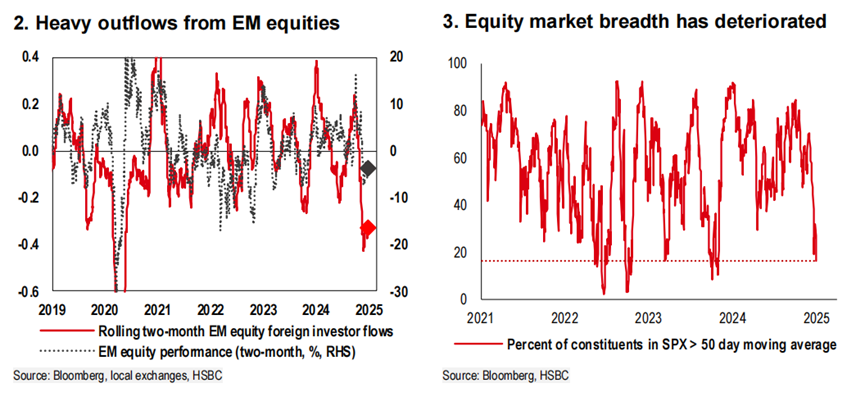

Specifically, since the yield low point in mid-September, the total return on long-term US Bonds has decreased by more than 12%, Exchange Rates in Emerging Markets and local Bonds have encountered a significant adjustment, and the stock market has experienced the largest Outflow of foreign capital since 2020.

At the same time, the USA's economic growth forecast for 2025 has been upgraded, and growth in the fourth quarter of 2024 may again exceed expectations. Inflation expectations have also risen significantly, with the market currently implying a one-year CPI of 2.52%. Meanwhile, short-term earnings expectations for the S&P 500 Index remain relatively low.

"The market breadth of the S&P 500 Index has significantly declined; historical experience shows that this may be a contrarian indicator, suggesting that the market adjustment is nearing its end."

Looking ahead to the coming weeks, HSBC believes that the market may continue to be volatile.

High expectations for Bond supply and ongoing inflation pressure may lead to poor performance of long-term yields, further suppressing the prices of risk Assets. At the same time, inflation expectations and market pricing have been excessively hawkish, which may gradually return to neutral.

Currently, market sentiment and position indicators have not issued a clear Buy signal.

Opportunities in the future.

However, HSBC stated that short-term market volatility will create attractive buying opportunities for USA Treasuries and risk assets. In particular, a "Goldilocks" economic environment could emerge in the first half of 2025, with both economic growth and inflation at moderate levels.

The current market has only priced in one rate cut by the Federal Reserve in the first half of the year, while the actual rate cut may be larger and requires repricing.

In terms of Stocks, HSBC believes that some excessively sold "bond proxy" assets (such as residential builders) may have rebound potential.

In addition, despite the overall market correction leading to a decline in Bank of America shares, HSBC believes that this drop has been excessive considering the potential for industry deregulation, high merger and acquisition activity, and high yields. Technology Stocks also show attractiveness in further adjustments.

For Emerging Markets Stocks, if the yields on US Bonds and the dollar stabilize, it may attract foreign capital inflows, and local debt in Emerging Markets may also become an unexpected "dark horse."

HSBC believes that in the coming months, the biggest risk is further increases in yields, rather than political factors.

"The key short-term catalysts are not the inauguration on January 20, but the US inflation data in December and the quarterly refinancing announcement (QRA) in early February."

Editor/new