According to FX168 Financial News (North America), after the S&P 500 Index has risen over 20% for two consecutive years, Wall Street strategists expect the pace of growth for the benchmark index to slow down in 2025, a situation that has not been seen since the late 1990s.

With strong earnings expected from a wide range of companies in 2025 and the anticipation that the USA economic growth will remain resilient, the fundamental story for further market growth in 2025 remains intact. However, strategists warn that with uncertainty surrounding the Federal Reserve's interest rate cuts and the imminent new government of Donald Trump, Stocks will face a more turbulent year.

BMO Capital Markets Chief Investment Strategist Brian Belski wrote in an outlook for 2025: "Bull markets may and should occasionally slow their pace, as it is a digestion period, which in turn will only highlight the health of the underlying long-term bull market." Therefore, we believe 2025 may be defined as a more normalized return environment, with performance more balanced across sectors, sizes, and styles.

Belski launched a year-end target of $6,700 for the S&P 500 Index. Given his index forecast of 6,100 by the end of 2024, Belski predicts a return of 9.8% in 2025, exactly aligning with the historical average growth rate of the index.

Belski launched a year-end target of $6,700 for the S&P 500 Index. Given his index forecast of 6,100 by the end of 2024, Belski predicts a return of 9.8% in 2025, exactly aligning with the historical average growth rate of the index.

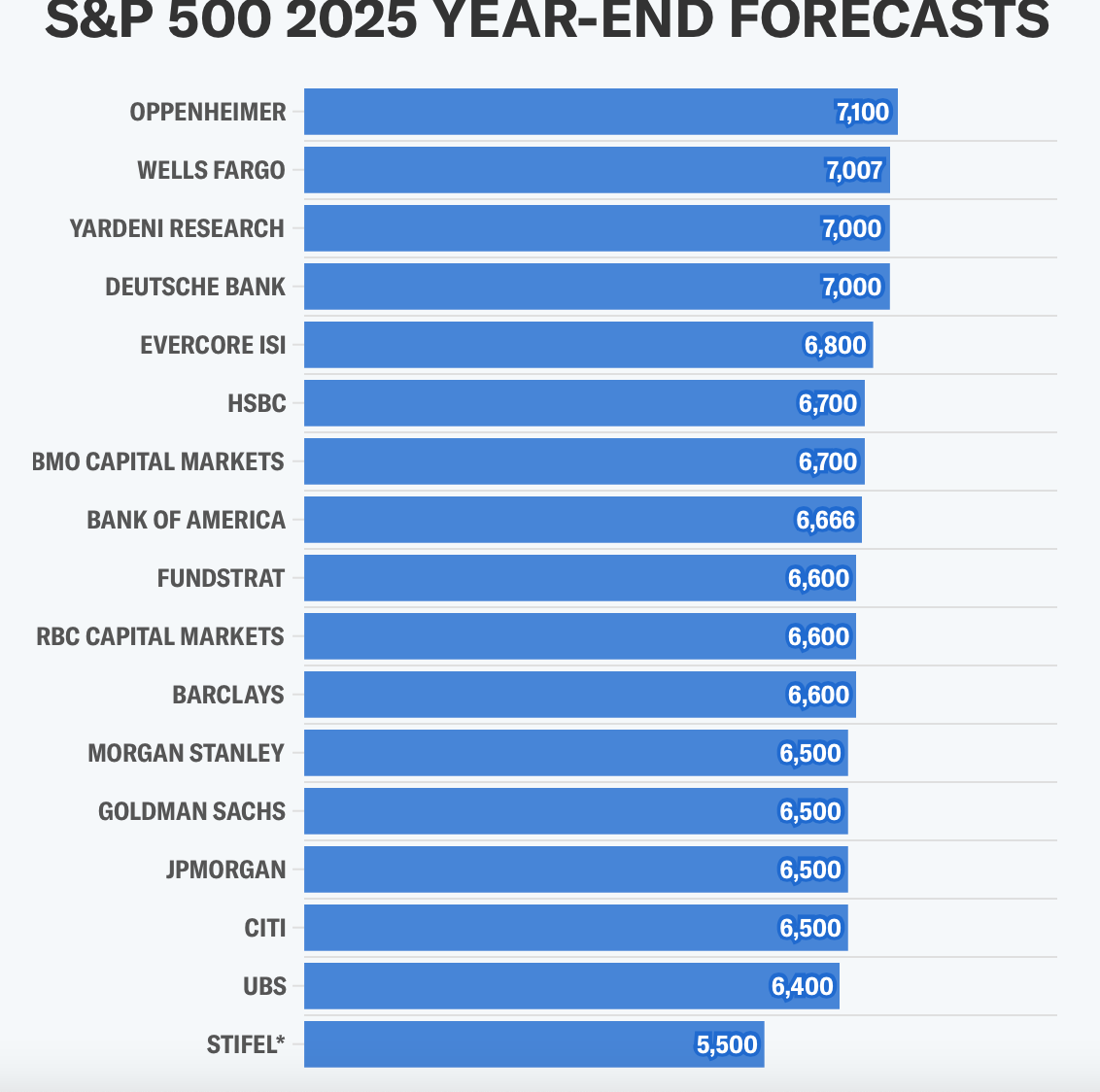

Among the strategists tracked by Yahoo Finance, the median year-end target for the S&P 500 Index is 6,600. This would represent about a 12% increase from the current level of the index. The target goes as high as 7,100 from Oppenheimer, down to the "mid-5,000s" prediction from Citigroup - the only call among the 17 strategists tracked by Yahoo Finance that expects the benchmark index to decline next year.

(Image source: finance.yahoo)

Less "stellar" performance.

Goldman Sachs' chief US stocks strategist David Kostin and others stated that even if the Stocks represented by the Magnificent 7 do not continue to perform excellently in 2025, the market could still surge, indicating a recovery in the Stocks.

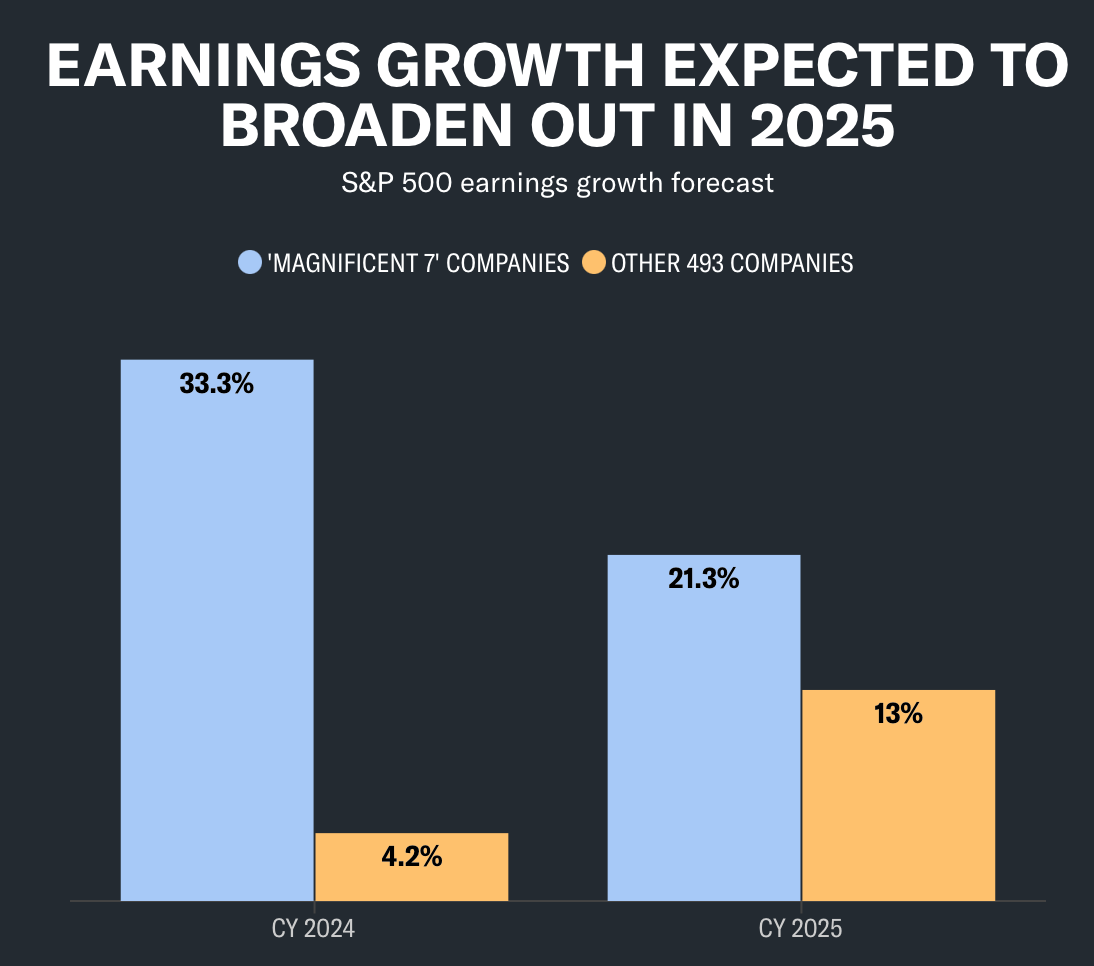

According to FactSet data, Apple (AAPL), Alphabet (GOOGL, GOOG), Microsoft (MSFT), Amazon (AMZN), Meta (META), Tesla (TSLA), and Nvidia (NVDA) saw a combined year-on-year earnings growth of 33% in 2024, while the other 493 S&P 500 companies only grew by 4.2%.

However, according to consensus estimates, this profit margin is expected to drop to only 8 percentage points by 2025. Kostin believes this will lead to the cohort only outperforming the other 493 Stocks by 7 percentage points in 2025, which is the narrowest margin level among the Stocks of the Magnificent Seven since 2018.

Kostin wrote that the narrowing gap in earnings growth rates should correspond to the shrinking relative Stock returns. "Although the 'micro' earnings growth story supports the continued excellent performance of the Magnificent 7, more 'macro' factors like economic growth and trade policy tend to favor the S&P 493."

(Image source: finance.yahoo)

Resilient US economy.

Lori Calvasina from Royal Bank of Canada Capital Markets listed growth stocks as a 'crowded' trade, leading to more Inflow potential in the market value aspect.

Importantly, Calvasina's appeal relies on another widely held belief entering the Wall Street bull market in 2025: the USA economy will continue to unexpectedly rise.

Calvasina stated, "To see value outperform the market in recent years, we need to see GDP running a bit hotter." He predicts GDP in 2025 to be between 2.1% and 3%, above Bloomberg's current consensus of 2.1%. "We provide an edge for expanding market leadership or shifting towards value, but consider this to be a close call."

The Bank of America economic team predicts that the USA economy will grow at an annualized rate of 2.4% in 2025, also higher than Bloomberg's consensus forecast of 2.1%.

This makes BofA lean towards "GDP-sensitive companies," recommending overweight ratings for the financial (XLF), consumer discretionary (XLY), materials (XLB), real estate (XLRE), and utilities (XLU) sectors.

Calvasina pointed out why achieving or exceeding optimistic economic growth is crucial for a stock market rebound. As early as 1947, annual GDP growth between 1.1% to 2% saw stocks rise fivefold. In those years, stocks only increased by 40% and had an average decline of 3.4%. Meanwhile, in years when GDP ranged between 2.1% and 3%, stocks rose by 70%, with average ROI close to 11%.

Of course, growth may not materialize. Evan Brown from UBS Group Asset Management stated that with so many strategists already anticipating a resilient economy, anything below that capacity could impact stocks. Considering that USA stock valuations are already quite rich, Brown stated, "It doesn’t take much" to change the widely held belief that the USA economy and stocks will outperform the rest of the world in 2025.

(Image source: finance.yahoo)

Known unknowns.

In fact, despite the optimistic market outlook, there are key risks in the strategists' calls that could lead to greater volatility in 2025.

One is the potential resurgence of inflation. Earlier this month, the Federal Reserve predicted that the core inflation rate would reach 2.5% next year, up from a previous forecast of 2.2%, and then decline to 2.2% in 2026 and 2% in 2027.

Barry Bannister, Chief Investment Strategist at Stifel, believes that sticky inflation due to sluggish economic growth will prompt the Federal Reserve to maintain high interest rates. These factors could be the key catalysts for a rebound in the stock market, potentially leading the S&P 500 Index to end 2025 in the 'mid-5000s.'

However, Bannister's fundamental case highlights many known unknowns discussed by Wall Street strategists regarding the stock outlook for 2025. The uncertainty surrounding what a new Trump administration will bring is likely to remain a market theme in the new year. Some policies proposed by President Donald Trump, such as imposing high tariffs on imported goods, corporate tax cuts, and limiting immigration, are considered potential inflationary.

Kevin Gordon, Senior Investment Strategist at Charles Schwab, stated, 'Stocks can withstand this situation, and they can... perform well in the long run, but not without some significant disruptions, especially since many of these policies are unprecedented.'