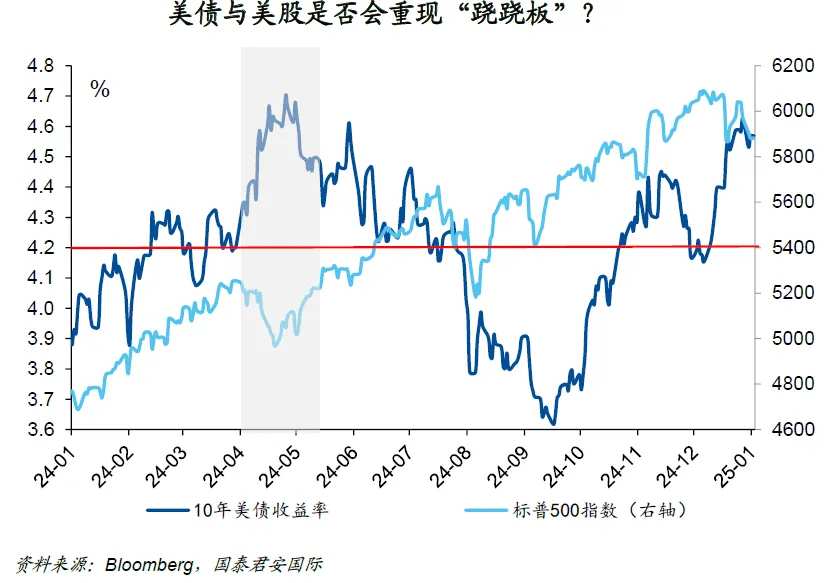

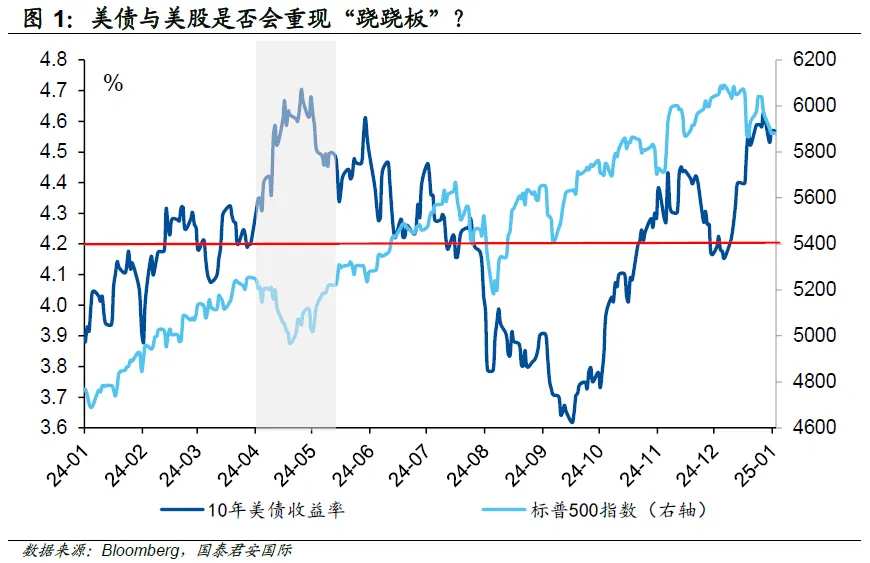

当然,支撑美股继续保持强势的理由,仍然是“美国例外”,即美国经济的良好表现会成为支撑美股的关键因素,因此美股将无惧来自利率端的压力。但这一看法能否站得住脚仍然需要推敲。从去年4月的情形来看,当时美国经济的表现也相当不错,GDPNow的预测值也一路上扬,直至5月才逐步见顶回落。但事实上,美股在整个4月的表现则相对低迷,直至10年美债利率出现回落后才逐步重拾动能。

当然,支撑美股继续保持强势的理由,仍然是“美国例外”,即美国经济的良好表现会成为支撑美股的关键因素,因此美股将无惧来自利率端的压力。但这一看法能否站得住脚仍然需要推敲。从去年4月的情形来看,当时美国经济的表现也相当不错,GDPNow的预测值也一路上扬,直至5月才逐步见顶回落。但事实上,美股在整个4月的表现则相对低迷,直至10年美债利率出现回落后才逐步重拾动能。Source: Guojun Overseas Macro Research

Authors: Zhou Hao, Sun Yingchao

The strong finish of the US stock market in 2024 has set the best consecutive performance in 25 years. As we enter 2025, the trading themes in the Global market still revolve around the 'Trump Trade' and 'US Exceptionalism'. Such trades have driven the rise of the dollar and US debt rates, but the recent market focus has shifted to US stocks, questioning whether US stocks will experience an adjustment similar to that of last April against the backdrop of strong dollar rates.

From past experience, the market's expectations for the Federal Reserve's interest rate cuts have always been dynamically adjusted. Based on the current expectation of about 1-2 cuts, a 2-Year T-Note yield of around 4.2% is relatively reasonable, which is also the safest area in the current US debt market. The fluctuations in long-term bonds reflect, on one hand, the market's entanglement and, on the other hand, may become a source of market volatility. Taking the 10-Year T-Note as an example, it rose by about 100 basis points after the Fed's rate cut in September, which not only surprised the market but also became the biggest macro risk factor for the adjustment of US stocks.

Of course, the reasons supporting the continued strength of US stocks remain 'US Exceptionalism', meaning that the good performance of the US economy will be a key factor supporting US stocks, hence US stocks will not fear pressure from interest rates. However, whether this view holds true still needs to be scrutinized. Looking back at April of last year, the performance of the US economy was also quite good, and the forecast value of GDPNow kept rising until it peaked and fell gradually in May. However, the performance of US stocks throughout April was relatively sluggish until the 10-Year T-Note yield began to fall, allowing it to gradually regain momentum.

Of course, the reasons supporting the continued strength of US stocks remain 'US Exceptionalism', meaning that the good performance of the US economy will be a key factor supporting US stocks, hence US stocks will not fear pressure from interest rates. However, whether this view holds true still needs to be scrutinized. Looking back at April of last year, the performance of the US economy was also quite good, and the forecast value of GDPNow kept rising until it peaked and fell gradually in May. However, the performance of US stocks throughout April was relatively sluggish until the 10-Year T-Note yield began to fall, allowing it to gradually regain momentum.

Another point worth comparing with the market over six months ago is the expectations of interest rate cuts. In late March, we held a roadshow in Shanghai, and the feedback from investors at that time was that they believed the Federal Reserve might not cut rates in 2024, citing the reasons of a strong US economy and high inflation. From this perspective, the consensus formed by the market at a certain point—though it may be proven wrong later—has been the dominant force driving market changes, and this is still the case now.

Our intuitive feeling is that, compared to last April, the market is obviously more optimistic about the US economy and US stocks, which somewhat indicates a more pessimistic view of the bond market. Whether Stocks and long-term Bonds will reappear in a seesaw pattern will be the first answer that investors need to wait for in 2025.

The strong finish of the US stock market in 2024 has set the best consecutive performance in 25 years. As we enter 2025, the trading themes in the Global market still revolve around the 'Trump Trade' and 'US Exceptionalism'. Such trades have driven the rise of the dollar and US debt rates, but the recent market focus has shifted to US stocks, questioning whether US stocks will experience an adjustment similar to that of last April against the backdrop of strong dollar rates.

In April 2024, the 10-Year T-Note rates saw a rapid increase, rising from around 4.2% to near 4.7%. Along with the rise in US bond rates, US stocks experienced a decline. For example, the S&P 500 adjusted by more than 5% in the first three weeks of April, even briefly falling below the 5,000-point mark. Compared to April last year, the US stock performance has been quite mixed since the Federal Reserve's rate cut in December. On the day of the interest rate decision, the Nasdaq index experienced an adjustment of over 3%, and it has been consolidating below 20,000 points recently. Ed Yardeni, known as the "Prophet of Wall Street," has recently indicated that US stocks might undergo a 10% or even 15% adjustment. The most important logic behind this is the market's adjustment to the expectations for the Federal Reserve's rate cuts. According to Yardeni, the US economy is performing well, therefore the current interest rate level is appropriate; in other words, he believes the chance of the Federal Reserve not cutting rates in 2025 is increasing. From the market's actual feedback, the expectations for rate cuts in 2025 have decreased from about four times a month ago to about 1.7 times.

From past experience, the market's expectations for the Federal Reserve's interest rate cuts have always been dynamically adjusted. Based on the current expectation of about 1-2 cuts, a 2-Year T-Note yield of around 4.2% is relatively reasonable, which is also the safest area in the current US debt market. The fluctuations in long-term bonds reflect, on one hand, the market's entanglement and, on the other hand, may become a source of market volatility. Taking the 10-Year T-Note as an example, it rose by about 100 basis points after the Fed's rate cut in September, which not only surprised the market but also became the biggest macro risk factor for the adjustment of US stocks.

Of course, the reason supporting US stocks to remain strong is still US Exceptionalism, meaning the strong performance of the US economy will be a key factor supporting US stocks, thus these stocks will not fear the pressure from interest rates. However, whether this view can hold up still needs to be examined. Looking back to April last year, the performance of the US economy was also quite good, and the GDPNow forecast rose steadily, peaking in May before gradually declining. However, in reality, the performance of US stocks was relatively lackluster throughout April, regaining momentum only after the 10-Year T-Note rates declined.

Another point worth comparing to the market more than six months ago is the expectations for rate cuts at that time. We had a roadshow in Shanghai at the end of March, and the feedback from investors was that they believed the Federal Reserve might not cut rates in 2024, also due to the strong US economy and high inflation. From this perspective, the consensus formed by the market at a certain point in time—despite being potentially falsifiable afterward—has been the dominant force driving market changes, and it remains so now.

Our intuitive feeling is that, compared to April, the market is clearly more optimistic about the US economy and US stocks, which to some extent also implies a more pessimistic view towards the bond market. Whether stocks and long-term bonds will see a seesaw effect again will be one of the first answers investors need to wait for in 2025.

Editor/rice