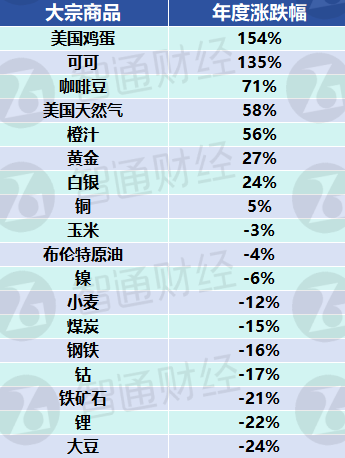

贵金属方面,2024年是包括黄金、白银在内的贵金属投资的重要一年。日益不确定的全球紧张局势和经济变化促使投资者寻求更安全的资产,推动了对投资贵金属的需求。其中,黄金频频创下历史新高。

贵金属方面,2024年是包括黄金、白银在内的贵金属投资的重要一年。日益不确定的全球紧张局势和经济变化促使投资者寻求更安全的资产,推动了对投资贵金属的需求。其中,黄金频频创下历史新高。Precious Metals shone, Copper experienced a dramatic short squeeze, soft commodities surged... The commodity market faced a turbulent year in 2024.

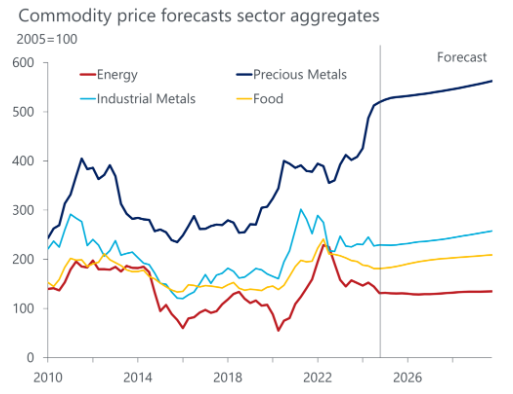

In 2024, the commodity market experienced a turbulent year with varied performances across different sectors.

As of the release date, in the energy sector, Brent Crude Oil and WTI Crude Oil prices fell slightly over the year, while Henry Hub Natural Gas prices increased by 58%. Changes in demand, geopolitical turmoil, and rising production are key factors affecting energy prices. Although Natural Gas prices rebounded at the end of the year, they remained under pressure for much of 2024.

In terms of Precious Metals, 2024 was an important year for investments in Precious Metals including Gold and Silver. Increasingly uncertain global tensions and economic changes prompted investors to seek safer assets, driving demand for Precious Metal investments. Among these, Gold frequently reached historical highs.

In terms of Precious Metals, 2024 was an important year for investments in Precious Metals including Gold and Silver. Increasingly uncertain global tensions and economic changes prompted investors to seek safer assets, driving demand for Precious Metal investments. Among these, Gold frequently reached historical highs.

Among base metals, Copper became the market focus, not only reaching historical price highs but also triggering a shocking COMEX short squeeze event in the first half of the year. In contrast, the three major battery metals continued their downward trend from last year, with trading prices of Lithium, Nickel, and Cobalt collapsing across the board.

The soft commodities sector was the brightest performer this year. Drought and high temperatures, combined with global reliance on supplies from a few regions or countries, were the main driving factors for the strong performance of soft commodities this year. The surge in Cocoa prices earlier this year garnered widespread attention, and prices for Orange Juice and, more recently, Coffee also experienced strong growth. In 2024, the best-performing commodities in the futures market continued to be the three soft commodities that ranked at the top last year: Cocoa, Orange Juice, and Coffee beans. However, similar to last year, Grain contracts again incurred losses over the past 12 months.

Looking ahead to 2025, based on supply and demand dynamics, Wall Street investment banks expect Brent Crude Oil prices to fall to about $70, while Natural Gas prices are expected to rebound further. Additionally, Precious Metal prices are anticipated to continue their upward trend, while prices for Cocoa, Coffee beans, Orange Juice, and Eggs are expected to rise further due to supply shortages. However, base metals and grain crops are likely to face price pressure due to oversupply.

Energy: Oil prices are under pressure, while natural gas rebounds.

Oil.

Crude Oil prices fluctuate downward, facing challenges from demand volatility triggered by economic uncertainties and other factors. At the same time, OPEC's production cut plan becomes an important variable affecting oil prices—this includes the timing of lifting the production cut plan and the overproduction issues of member countries. Geopolitical tensions further increase the uncertainty of oil supply. Additionally, the output growth from non-OPEC+ oil-producing countries also undermines the actual effectiveness of OPEC+'s production cut actions.

At the beginning of this year, the price of Brent Crude Oil was $75.90 per barrel, rising to $91.13 on April 5, reaching a new high for the year. On September 10, oil prices fell to a year-low of $69.09. As of the end of December, oil prices remained around $72.

In 2025, the dilemma facing OPEC is whether to continue to halt production and lose market share or increase output and endure a decline in prices and profit margins. Overall, as long as prices do not deteriorate further, OPEC+ will begin to increase production next year. As U.S. supply growth slows next year, the organization will provide a key area for supply growth.

Global oil demand has been disappointing, and global economic growth in 2025 is likely to remain robust but unremarkable. U.S. gasoline inventories, a key indicator of oil demand, are above long-term seasonal levels. With consumers shifting to electric vehicles, demand for automotive fuel in developed countries will decline over the long term, which is unfavorable for both demand and prices. Therefore, as market sentiment continues to remain weak, Brent Crude Oil prices may further decline. Major Wall Street investment banks, including Bank of America, Morgan Stanley, Jefferies, Goldman Sachs, and Citigroup, still expect Brent oil prices to further decrease to around $70 per barrel by the end of next year.

Henry Hub Natural Gas

In 2024, the rebound in international natural gas prices is mainly due to a slight slowdown in supply growth. The natural gas futures index is expected to show volatile movements throughout 2024, reaching a yearly high of $3.76 per million British thermal units on December 24, with an annual increase of over 30%. However, in 2024, the global economic recovery is weak, and in the context of slowing demand growth (mainly driven by a mild winter in Europe), the decline in global natural gas production growth partially offsets the downward pressure on prices.

Looking ahead, the five-year pipeline agreement between Russia and Ukraine will expire at the end of 2024, which will increase supply risks across the European continent, ultimately leading to higher demand for liquefied natural gas (LNG). The surge in industrial demand due to renewable energy and pipeline exports to Mexico will further support prices in the USA. Analysts expect that, facing tightening supply and demand risks, the Henry Hub natural gas spot price on NYMEX is likely to rise to around $3 per million British thermal units by 2025.

Metals: Precious Metals shine, Copper experiences dramatic fluctuations.

Gold

Overall, there are three main demand drivers for rising gold prices in 2024: the gold rush by global central banks (de-dollarization), interest rate cuts by the Federal Reserve, and demand for safe-haven assets. Against this backdrop, the international gold price rises from $2063.04 to a high of $2790, with a maximum annual increase of over 35% and an annual increase of nearly 27%. According to the World Gold Council, this year's gold price has set over 30 new highs.

Looking to 2025, as the three major demand factors are expected to remain in resonance, major Wall Street investment banks such as JPMorgan and Citigroup predict that demand for gold from central banks, along with concerns over inflation and excessive fiscal spending, will continue to drive gold prices higher next year. Goldman Sachs and Bank of America both expect gold to rise nearly 13% next year, reaching $3000 per ounce, although this is less than half of this year's increase. The average expectation of the top ten investment banks is that gold prices will rise 8% next year, reaching $2860.

Silver

The rise in silver prices this year largely reflects the upward trajectory of gold, driven by several common macroeconomic factors. As the 'poor relative' of gold, the three key factors boosting gold prices also indirectly support silver prices. On the other hand, although investment drivers play a role, the price movement of silver is also closely linked to its industrial use, which accounts for about 55% of total silver demand. The increase in industrial demand in 2024 has helped create physical tightness in the silver market. Sectors such as electronics and renewable energy, particularly photovoltaic (solar) technology, have contributed significantly to this surge.

The persistent structural deficit can be attributed to the difficulty miners face in discovering new silver deposits, and expectations of continued industrial demand may mean that silver supply shortages could last until 2025. The Silver Institute indicates that the silver market will experience a significant structural supply deficit for the fourth consecutive year. As silver is usually a byproduct of lead, zinc, copper, and gold mining, a price increase is unlikely to stimulate a significant rise in production, ensuring that the supply constraints will continue to support the market.

Meanwhile, current investment positions in silver remain relatively low. Data shows that both long-term holdings in ETFs and short-term futures positions are relatively low before 2025, suggesting potential upward space if the fundamentals support a rise in silver prices. Despite strong performance in 2024, silver only reached its highest point in 12 years, whereas gold set multiple historical highs. The dual impact of balanced investment and industrial demand may enable silver to outperform gold in the coming year.

In Saxo Bank's forecast, the current gold-silver ratio, which hovers around 87, may decline next year, potentially approaching 75 seen earlier in 2024. If this occurs, with gold prices reaching the predicted $3,000 per ounce, silver could reach $40 per ounce (an increase of over 25%).

Copper

Copper trading experienced a wild year in 2024. It initially began at the end of 2023, when several mines experienced production cuts, causing copper prices to rise. By mid-March 2024, expectations of interest rate cuts combined with the announcement of coordinated production cuts by Chinese smelters sparked a major rally in copper prices. In mid-May, due to historically low COMEX inventories and cross-market arbitrage opportunities that caused COMEX short positions to far exceed their inventories, a COMEX squeeze occurred, driving copper prices above $0.011 million per ton, hitting a historic high of $0.0115 million. From June to August, the COMEX squeeze subsided, and combined with negative demand feedback and rising inventories, copper prices started to correct. In September, China's shift in policy combined with the Federal Reserve's interest rate cuts saw copper prices break through $0.01 million again. In mid-November, after the U.S. presidential election results were confirmed, market concerns over trade frictions after Trump took office and a strong dollar led to a short-term rapid correction in copper prices.

The tight supply of Copper mines is one of the main drivers behind the strong rise in copper prices in 2024. However, the tight supply situation is expected to ease next year. The Bank of Montreal states that the copper market will remain well supplied in 2025, with a growth rate of about 2.8%, which is higher compared to recent historical levels. Additionally, Trump's tariff policy may undermine Global economic growth, causing trade flows to readjust, increasing inflation, and tightening monetary policy. For commodities like copper and iron ore that are most affected by the Global economy, this means demand may be impacted.

In 2025, copper prices are expected to maintain high volatility in a range. Against this backdrop, Goldman Sachs, which has been very bullish on copper prices in recent years, has significantly lowered its average copper price forecast for next year from $5,000 to $10,160 per ton. Citigroup has also recently downgraded its forecast from an average of $10,250 per ton next year to $8,750. However, in the context of potentially tight supply, the revised Target Price is still above the current level.

Nonetheless, the Royal Bank of Canada has lowered its estimate for 2025 to $8,800 (previously close to $10,000), while the Bank of Montreal's prediction for next year is that copper prices will hover around $4 per pound (or $8,800 per ton). Capital Economics is the most pessimistic, predicting an average of only $8,000 by the end of 2026 and a continued decline before 2030.

Battery Metal

This year, the battery metal industry globally is eerily similar to the bleak year of 2023, with ongoing price crashes for lithium, nickel, and cobalt in 2024. The 'electrification dream' of the 'three major battery metals' focused on electric vehicles has evidently turned into a nightmare that is difficult to escape.

This is also a story about large-scale oversupply, with too many new capacities being put into use at the wrong time. First, in terms of supply, there is a surge in the supply of metals used in electric vehicle batteries. Statistical agencies indicate that Chinese nickel producers have already achieved a technological leap. Secondly, Chinese lithium producers are also resisting production cuts.

In the demand sector, the electric vehicle market is still struggling to build momentum, with Auto Manufacturers significantly reducing their electric vehicle operations due to transformation difficulties. Additionally, Consumers are more inclined to choose hybrid vehicles—where the battery size is about one-third of pure battery models, meaning the size of all Metal cathode inputs will also significantly decrease.

For the outlook before 2025, given the similar negative supply-demand dynamics mentioned above, it is understandable why Wall Street Analysts generally believe that the producer prices of the three major battery metals will continue to plummet in the coming months.

According to consulting firm Benchmark Mineral Intelligence, lithium supply is expected to greatly exceed demand for three consecutive years by 2025. Predictions from consolidated Wall Street analysts indicate that if the scale of overproduction shrinks from nearly 10% last year to less than 1% of demand, this may limit further declines in battery metal prices.

In contrast, the oversupply in the nickel and cobalt markets may become a structural problem until the production of these two battery metals more closely aligns with demand.

Agricultural Products: Cocoa, coffee beans, and orange juice become the 'most popular commodities'.

Cocoa

In 2024, cocoa's surge has surpassed all major Commodities, even exceeding the gains of the USA stock market and Bitcoin. Due to declining yields in West Africa (the world's largest food cultivation area), a massive supply shortage has caused prices to nearly double, skyrocketing to a historical high of nearly $0.012 million per ton.

The rapid rise in cocoa prices is driven by several factors. First, adverse weather conditions in major producing countries like Ivory Coast and Ghana (which account for nearly 70% of global production) along with crop diseases have restricted overall production. Additionally, low global inventories, soaring shipping costs, and years of underinvestment in cocoa cultivation have further exacerbated supply tensions. In the 2023-2024 cocoa season, the supply gap reached 0.478 million tons, the largest in over 60 years. This marks the third consecutive year of deficits in the global cocoa market, intensifying the pressure on the supply chain.

The surge in cocoa prices has also impacted the chocolate industry. Leading confectionery brands like Hershey (HSY.US) and Mondelez International (MDLZ.US) are struggling to cope with rising input costs and increasingly passing the burden onto consumers. Price increases for chocolate, cakes, and cocoa drinks are becoming more common. Additionally, brands are diversifying their product portfolios and launching alternative flavors to offset the challenges of cocoa costs.

Looking ahead to 2025, there are few signs that the supply tightness and fragile trading environment that led to its nearly vertical trajectory will be quickly remedied. The record warm ocean temperatures globally have exacerbated the already vulnerable situation for West African cocoa crops, which have been damaged by two years of extreme weather. The recent Harmattan winds in West Africa threaten cocoa's 'mid-season crop,' which is typically harvested in the spring.

Moreover, both Ivory Coast and Ghana are still struggling to fulfill contracts that were postponed last season. The total short positions on the NYSE have fallen to their lowest seasonal level since 2011; this further drains liquidity, making the market more susceptible to significant price fluctuations.

Coffee Beans

In September this year, Robusta coffee reached an all-time high on the London ICE-LIFFE Futures Exchange, with prices up 86% compared to the same period last year. Arabica coffee futures prices once soared to a 47-year high, rising nearly 70% year-to-date. Major producer Brazil experienced its worst drought in 70 years in August and September, followed by heavy rains in October, raising concerns about potential crop failures. Meanwhile, growing consumption in China has further boosted demand for it.However, production has struggled to keep up with this rising demand.

Supply risks have triggered panic buying among commercial buyers concerned about shortages, and shipping ahead to the USA before potential tariffs may also have played a part. Finally, the EU's controversial deforestation regulations (EUDR) are set to be introduced, adding a layer of complexity to the market.

By 2025, coffee prices may be higher. The cocoa output in West Africa accounts for 70% of the global total, but the crop yield in the region has not rebounded significantly as previously expected. Coffee traders believe that if the crops in Brazil do not recover, prices may need to rise from the current 350 cents per pound to between 400 and 500 cents. Coffee roasters will raise retail prices, especially for espresso made from Arabica coffee beans.

Orange Juice

In the USA, Hurricane Milton has damaged orange production in Florida, while growers are still troubled by previous storms and persistent pest issues, all of which have driven orange juice Futures to set historical highs. Meanwhile, like coffee beans, Brazil has suffered from severe drought and heavy rain, causing orange juice prices to soar by more than 100% during the year.

Orange juice prices may further climb in 2025. A report released on December 10 by the USDA-NASS indicates that the sweet orange production in Florida for the 2024/2025 season is only 0.4899 million tons, down 20.00% from the October forecast and down 33.18% from the actual figure last year. Meanwhile, global orange juice inventories remain relatively low, and the settlement price of global frozen concentrated orange juice futures contracts continues to rise slightly.

Eggs

Due to the recent outbreak of Bird Flu alongside high demand, egg prices in the USA have surged. Following a massive outbreak of highly pathogenic avian influenza, egg prices in the USA reached a peak of $4.82 per dozen in January 2023. As flocks were replenished and supply increased, the average price in the USA fell to $2.04 in August 2023, before rising again. In summer 2024, egg prices slightly rose again, reaching a peak of $3.82 in September, and remained high. The average price for eggs in the USA in November was $3.65 per dozen.

The US egg market is still under tight supply. The supply has been reduced due to the outbreak of Bird Flu, and the process of clearing the Bird Flu epidemic and returning production to previous levels could take a whole year, coupled with demand peaking. To make matters worse, many states including Michigan, Massachusetts, and California have already or are about to pass laws banning the sale of cage-free eggs, which will drive up market demand. Additionally, companies like McDonald's only sell free-range eggs, increasing demand in the wholesale market.

Since 2022, Bird Flu has frequently broken out, hindering the establishment of flocks, resulting in insufficient supply in the egg market, and producers have still not been able to rebuild the total laying hen population. Kevin Bergquist, manager of the Agricultural Food Research Institute at Wells Fargo & Co, predicts that this rising cost will continue until 2025, especially if highly pathogenic avian influenza (HPAI) infections persist.

Cereal Crops

Soybean almost ranked at the bottom of the commodity price performance in 2024, with a decline of slightly over 20%. Favorable weather conditions in major producing areas led to a bumper harvest of soybeans in 2024, resulting in a market oversupply. At the same time, decreased demand from major importing countries and increased competition from alternative oilseeds contributed to a significant market oversupply.

The performance of wheat Futures has also been weak, and corn Futures performed only slightly better, with a decline of 15%. The seasonal price peak was set in May this year, and the preceding strength only provided a brief window for selling before harvest. The prices of corn, soybeans, and wheat Futures still remain above the lows reached since August.

The reason for the weak price trend in the agricultural product market this year is abundant supply. Due to Brazil's bumper harvest and weak demand, the supply level for the 2024/25 crop year will reach the highest level in 17 years. Similarly, the corn supply ratio will remain high for the 2024/25 crop year. In contrast, wheat prices continue to decline, indicating a tightening market but still remain at comfortable levels. Despite good harvests, India's export restrictions have kept rice prices high, but recent lifting of restrictions caused a price crash. Thus, soybean prices are expected to remain sluggish in 2025, reflecting a more relaxed market dynamic. Corn and wheat prices are expected to rise to current levels but will still be below the levels of 2021-2023.