据TrendForce集邦咨询数据,

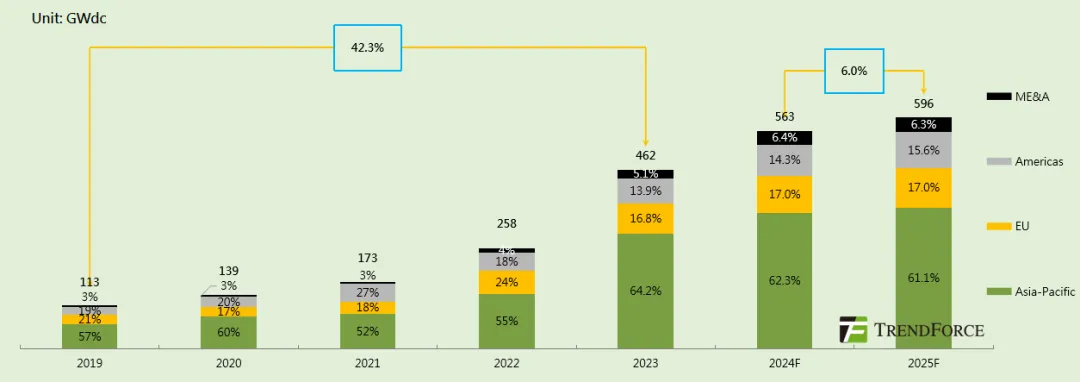

据TrendForce集邦咨询数据,According to TrendForce's data, Global photovoltaic installed capacity has rapidly increased from 113 GW in 2019 to 462 GW in 2023, with an average annual compound growth rate of 42.3%.

According to the Zhito Finance APP, against the backdrop of the Global Energy Transition, the photovoltaic industry is thriving, and the global installed capacity of photovoltaic systems continues to grow. TrendForce predicts that by 2025, the global photovoltaic newly installed capacity will reach 596 GW, an increase of 6.0% year-on-year, with growth significantly slowing down. The three major mainstream increment markets in China, Europe, and the USA are seeing a decline in market share, while Emerging Markets such as Southeast Asia, Latin America, and the Middle East are performing exceptionally well, injecting new Xiong'an New Power Technology into the growth of global photovoltaic installed capacity.

Part.01 The global newly installed capacity in 2025 will reach 596 GW.

According to data from TrendForce, global photovoltaic installed capacity rapidly increased from 113 GW in 2019 to 462 GW in 2023, with a compounded annual growth rate of 42.3%. After experiencing high growth in the first five years, it is expected that starting in 2025, the growth rate of global photovoltaic newly installed capacity will significantly decline, entering an adjustment phase. By 2025, the global photovoltaic newly installed capacity will reach 596 GW, an increase of 6.0% year-on-year. In terms of market share, the Asia-Pacific region slightly decreased to 61.1%, the Americas market increased to 15.6%, and there were not significant changes in the shares of Europe and the Middle East and Africa markets.

According to data from TrendForce, global photovoltaic installed capacity rapidly increased from 113 GW in 2019 to 462 GW in 2023, with a compounded annual growth rate of 42.3%. After experiencing high growth in the first five years, it is expected that starting in 2025, the growth rate of global photovoltaic newly installed capacity will significantly decline, entering an adjustment phase. By 2025, the global photovoltaic newly installed capacity will reach 596 GW, an increase of 6.0% year-on-year. In terms of market share, the Asia-Pacific region slightly decreased to 61.1%, the Americas market increased to 15.6%, and there were not significant changes in the shares of Europe and the Middle East and Africa markets.

Figure: 2025 global photovoltaic newly installed capacity forecast.

From the photovoltaic newly installed capacity data of the four major regional markets in 2025, the Americas show a slight lead in growth, while the increment is still led by the Asia-Pacific region. In 2025, the Americas, driven by the USA and Brazil markets, will maintain a leading growth rate; Emerging Markets in the Middle East and Africa still have development potential but will see significant slowdowns in growth; the Asia-Pacific region will lead the global photovoltaic market increment, but growth rates will slow down due to high base numbers; Europe will steadily grow its increment under the goals of coal phase-out and total renewable energy.

Figure: Forecast for new installed photovoltaic capacity in global regional markets for 2025.

Part.02 The share of new installations in China, Europe and the USA in 2025 is 71.6%.

With the acceleration of the global Energy transition, countries are placing increasing importance on the development of Wind Power. China, Europe, and the USA continue to be the main incremental markets for global photovoltaic growth, accounting for 71.6% of new installations in 2025. However, due to the high base effect, the growth rate is gradually slowing down, and the installation share is showing a downward trend. In the non-China, Europe, and USA regions, driven by rigid demand for Electrical Utilities, urgent Energy transition requirements, and strategic Energy goals, the demand for photovoltaic is growing rapidly, with an upward trend in installation share. The following will focus on analyzing the development trends of the two major markets, China and the USA.

Figure: Proportion of new installed photovoltaic capacity in mainstream incremental countries in 2025.

In the Chinese market, centralized photovoltaic remains the main demand, while the incremental market is shifting towards commercial and industrial photovoltaic. TrendForce predicts that new installed photovoltaic capacity in China will reach 265GW in 2025, a year-on-year increase of about 1%, with overall growth significantly slowing down. From the perspective of detailed categories, household photovoltaic is constrained by insufficient grid capacity and declining economic viability, and is expected to remain weak in 2025; commercial and industrial photovoltaic is expected to continue growing against the backdrop of dual control on energy consumption and carbon emissions, as well as rising electricity prices in industry; the demand for centralized photovoltaic installations in the next two years will focus on wind and solar major base projects, and long-term support will still depend on the completion of Ultra High Pressure transmission line construction to effectively resolve consumption bottleneck issues.

Figure: Forecast for new installed photovoltaic capacity in China for 2025.

In the USA market, the Trump 2.0 policy has led to fluctuations in the installation of photovoltaic systems, but the long-term high growth trend remains unchanged. TrendForce predicts that by 2025, the USA is expected to add 60 GW of new photovoltaic installations, a year-on-year increase of 20%, with a slight slowdown in overall growth rate. Due to mismatches between electricity consumption and supply needs for grid facilities, the USA may face a significant electricity gap in the future. In the photovoltaic market, although trade barriers and supply chain issues continue to limit the release of installation demand, under a quota of 12.5 GW for Batteries, there is still an opportunity for the USA to import Batteries produced in four Southeast Asian countries to meet local end-user demand. Combined with support from the USA IRA subsidies, domestic production capacity will accelerate its release.

Figure: Prediction of new photovoltaic installations in the USA for 2025.

Part.03 The growth rate of new installations in four major regional markets slows down.

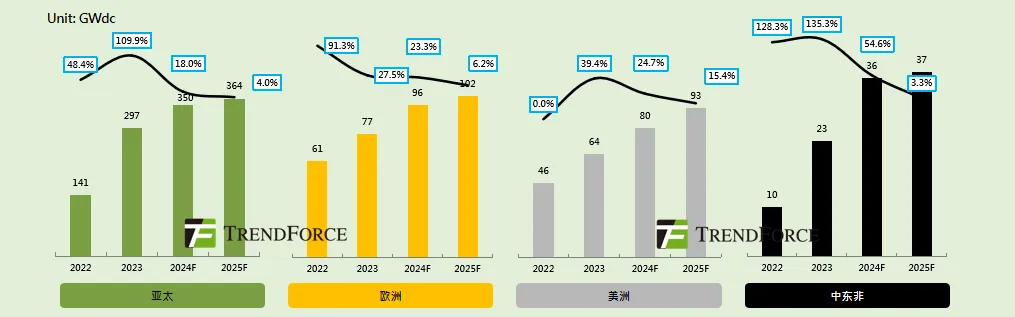

In the Asia-Pacific market, TrendForce predicts that by 2025, new photovoltaic installations in the Asia-Pacific region are expected to reach 364.3 GW, a year-on-year increase of 4.0%. China and India dominate the market, while the Southeast Asian region is experiencing high growth in photovoltaic installation demand due to energy transformation and increasing industrial electricity needs. In the Asia-Pacific market, distributed photovoltaic subsidies are gradually declining, and installation demand is shifting from subsidy-driven to market-driven. Centralized photovoltaic systems are being promoted by photovoltaic bidding projects, with the current growth bottleneck being issues related to grid acceptance.

Figure: Prediction of new photovoltaic installations in the Asia-Pacific market for 2025.

In the Americas market, TrendForce forecasts that the newly installed PV capacity in the Americas will reach 92.8 GW by 2025, representing a year-on-year increase of 15.4%. The growth will mainly come from the USA, while Brazil's growth rate is slowing and its share is declining. Distributed PV in mainstream countries in the Americas still relies on subsidies to drive installation demand, coupled with high electricity prices in some countries, which is likely to stimulate demand for self-consumed PV installations. Centralized PV mainly relies on PPA projects for promotion. Currently, grid absorption and financial pressures in Latin America will be major obstacles to the future development of the Americas.

Figure: Forecast for the newly installed PV capacity in the Americas market in 2025.

In the European market, TrendForce forecasts that the newly installed PV capacity in Europe will reach 101.5 GW by 2025, representing a year-on-year increase of 6.2%, with Germany, Spain, and the Netherlands ranking the top three. Distributed PV in the European market primarily relies on subsidy policies to drive growth, but these policies are facing a trend of gradual reduction. Centralized PV depends on government tenders and PPA projects for promotion. Although Europe is facing issues such as weak electricity demand and frequent negative electricity prices, the demand for PV installations continues to show strong growth under its long-term renewable energy and coal phase-out goals.

Figure: Forecast for the newly installed PV capacity in the European market in 2025.

In the Middle East and Africa market, TrendForce forecasts that the newly installed PV capacity in the Middle East and Africa will reach 37.5 GW by 2025, representing a year-on-year increase of approximately 3.3%. Installation demand mainly comes from Saudi Arabia, the UAE, and South Africa, while emerging markets such as Egypt and Oman remain to be developed. Currently, the demand for PV installations in the Middle East and Africa mainly relies on government or government-authorized institutions for bidding. In recent years, as the price of PV components has continued to decline, private PPA projects have gradually become active in the market due to higher market-based electricity prices.

Figure: Forecast for the newly installed PV capacity in the Middle East and Africa market in 2025.

Overall, by 2025, the growth rate of new photovoltaic installations is expected to significantly slow down globally. The traditional markets of China, Europe, and the USA are gradually slowing because of their large scale, while non-China, Europe, and USA markets are anticipated to achieve rapid growth from a low base. Emerging Markets are rising rapidly, leading to a high demand for photovoltaic installations. The main reasons for the slowdown in global photovoltaic installation growth are insufficient grid capacity and increasingly prominent issues with accommodating wind and solar power. In some regions, economic downturns and limited fiscal expenditures have resulted in insufficient implementation of subsidy policies. Additionally, some mainstream countries are facing growth bottlenecks in residential photovoltaics. In the future, commercial, industrial, and centralized photovoltaics are expected to become the dominant forces in the market.