全球旅游大热潮,是美国股市与全球股市的航空股从第三季度暴跌中反弹的原因之一,大批量美国游客前往世界各地,尤其是欧洲与东亚地区,在亚洲,中国游客赴日本、东南亚的旅游热潮已经持续一整年,并且中美刮起的全球旅游热潮未看到任何降温迹象。另一方面则是各大航空公司的运力增长非常有限,部分原因是航空公司正在削减一些无利可图的航线。巴克莱银行预计,到2025年,美国航空公司的座位增长将低于3%,低于新冠疫情前的长期趋势。

全球旅游大热潮,是美国股市与全球股市的航空股从第三季度暴跌中反弹的原因之一,大批量美国游客前往世界各地,尤其是欧洲与东亚地区,在亚洲,中国游客赴日本、东南亚的旅游热潮已经持续一整年,并且中美刮起的全球旅游热潮未看到任何降温迹象。另一方面则是各大航空公司的运力增长非常有限,部分原因是航空公司正在削减一些无利可图的航线。巴克莱银行预计,到2025年,美国航空公司的座位增长将低于3%,低于新冠疫情前的长期趋势。As the tourism industry thrives, American Airlines stock index has risen by 60%, marking the largest increase in a decade and significantly outperforming the S&P 500 Index.

According to Zhito Finance APP, the US travel industry is experiencing a record sales growth momentum in 2024, driving a surge in the annual stock price performance of US airline stocks. The benchmark index for US airline stocks increased significantly by 60%, far outperforming the S&P 500 Index, and the continued strong earnings expansion outlook indicates that the stock market outlook for 2025 remains optimistic. With the global tourism industry flourishing, both US market airline stocks and global overall airline stocks have reached the highest growth levels in a decade.

Statistics show that the benchmark index for US airline stocks, the S&P Supercomposite Airlines Index, rose by 60% in 2024, while the S&P 500 Index increased by only 27%. This is the best year for the industry's benchmark index since 2014, when it also significantly outpaced the US Large Cap market. The best-performing component stock of this airline benchmark index was United Airlines (UAL.US), which has seen its stock price rise by about 144% so far this year, making it the fourth-best-performing component of the S&P 500 Index in 2024.

The global tourism boom is one of the reasons for the rebound in airline stocks in the US and global stock markets from the sharp decline in the third quarter, as a large number of American tourists travel around the world, especially to Europe and East Asia. In Asia, the surge of Chinese tourists to Japan and Southeast Asia has continued for a whole year, and the global tourism boom triggered by the USA and China shows no signs of cooling down. On the other hand, the capacity growth of major airlines is very limited, partly due to airlines cutting back on unprofitable routes. Barclays estimates that by 2025, the growth of seats offered by US airlines will be below 3%, lower than the long-term trend before the COVID-19 pandemic.

The global tourism boom is one of the reasons for the rebound in airline stocks in the US and global stock markets from the sharp decline in the third quarter, as a large number of American tourists travel around the world, especially to Europe and East Asia. In Asia, the surge of Chinese tourists to Japan and Southeast Asia has continued for a whole year, and the global tourism boom triggered by the USA and China shows no signs of cooling down. On the other hand, the capacity growth of major airlines is very limited, partly due to airlines cutting back on unprofitable routes. Barclays estimates that by 2025, the growth of seats offered by US airlines will be below 3%, lower than the long-term trend before the COVID-19 pandemic.

Investment Institutions believe that these stock prices are still cheap, according to a team of analysts led by Brandon Oglinski at Barclays. He is bullish on traditional airline giants such as United Airlines and Delta Air Lines (DAL.US) because they provide high-quality travel services and large-scale international route operations. The firm also favors Alaska Air Group (ALK.US) and Frontier Group Holdings Inc. (ULCC.US) because they have significantly improved their frequent flyer programs.

Barclays stated that this significant rise indicates good prospects for the global airline industry in the coming year. "We believe that by 2025, the fundamentals of the aviation industry will continue to improve significantly, which will provide important support for the strong profit margins and earnings growth prospects of many airlines in the industry," wrote Barclays analysts led by Oglinski in a research report.

The aviation giants have collectively raised their performance expectations.

Not only do investment institutions have a bullish outlook on the performance growth of the aviation industry in 2025, but the airlines themselves also look very promising—extreme optimism for 2025 has already been fully reflected in the performance forecasts of the aviation giants. JetBlue Airways, Southwest Airlines, and American Airlines Group have significantly raised their profit forecasts for the fourth quarter and early 2025, reflecting strong demand for holiday travel, rising ticket prices, and declining fuel prices. Delta Air Lines will officially kick off the quarterly performance reporting cycle for airlines on January 10.

Investment institutions are also optimistic that the significant improvement in the regulatory environment under the re-elected U.S. President Donald Trump will support the prosperous development of the aviation industry. Executives in the aviation industry generally believe that Trump's promised deregulation and tax cuts could further boost tourism development and overall demand for the aviation industry, and that compared to the Biden administration, mergers and acquisitions in the aviation sector may be more favorable.

It is understood that the Biden administration had collectively pressured U.S. airlines on issues such as automatic refunds, ultimately preventing a large-scale merger between JetBlue Airways and Spirit Airlines Inc.

Grace Li, a fund manager from the Columbia Dividend Opportunity Fund, stated that it is unlikely for Trump to prioritize significant adjustments or drastic changes in air travel. As of November, the fund continues to hold shares in Southwest Airlines. Li mentioned that the operating conditions of Southwest Airlines have improved following the aggressive investment campaign by activist investment institution Elliott Management.

The portfolio manager stated, 'Overall, I am more confident; many management teams we have contacted in the aviation industry seem to have a more optimistic view of the improvement in global business and economic activity.'

The travel boom continues to sweep the globe, and capacity cannot keep up with demand.

After the COVID-19 pandemic, global airlines are struggling to balance air transportation capacity with increasingly strong demand, rushing to expand routes and the number of aircraft in any way possible to keep up with the so-called revenge travel boom. Overall, airlines' capacity is falling short of the increasingly strong demand from global travelers. Airlines need a long period to restore or expand capacity, such as reopening routes, recruiting and training crew members, purchasing or leasing new aircraft, etc. These adjustments typically lag significantly behind the rapid changes in demand, resulting in a continued shortage of capacity.

It is reported that the largest manufacturer of civil aircraft, Boeing, was controlled by American aviation regulatory authorities this year due to a series of scandals, limiting aircraft production capacity. On January 5, 2024, a Boeing 737 MAX 9 passenger aircraft operated by Alaska Air experienced a door detachment during flight, forcing an emergency landing. Following the incident, the FAA restricted the production rate of the Boeing 737 MAX.

This imbalance is most evident among low-cost airlines focused on the domestic market in the USA. Due to the long-term inability of capacity to meet demand and high maintenance and monitoring costs for older aircraft, these airlines are now shifting towards offering a higher-end flying experience to attract global travelers with bigger budgets.

In the USA, according to the latest statistics from the Department of Transportation, the number of Americans flying has reached an unprecedented level, with the busiest 10 travel days in the history of the TSA occurring in the Calendar for 2024. American tourists are primarily heading to Europe and regions in East Asia and Southeast Asia.

In Asia, customs statistics show that in the first 10 months of this year, over 30 million international tourists visited Japan, breaking Japan's annual record for tourists, with the main sources of visitors being the USA and China. According to MSCI Real Assets, as of the first half of 2024, the overall transaction volume in Japan's hotel industry reached 767 billion yen, a 46% increase year-on-year, marking at least the highest level in a decade.

A forecast report from Deutsche Bank indicates that the gap between the "wealthy countries" and "poor countries" in the aviation Industry will widen, and it is anticipated that aviation giants like Delta Air Lines, American Airlines, and United Airlines will account for about 90% of operating and pre-tax profits in 2025. It is evident that the Industry experienced a dramatic shift in the last few months of 2024, and there are still areas that require significant improvement.

Due to delays in large-scale deliveries of civil aircraft from Boeing and Airbus, as well as fluctuations in oil prices, the maintenance and monitoring costs incurred by the continued operation of some older aircraft models remain a major risk, which is also the core logic behind the wait-and-see attitude of some investment Institutions. Even though American Airlines' stock price has recently rebounded significantly, the industry benchmark stock Index is still over 10% lower than the peak level in early 2020.

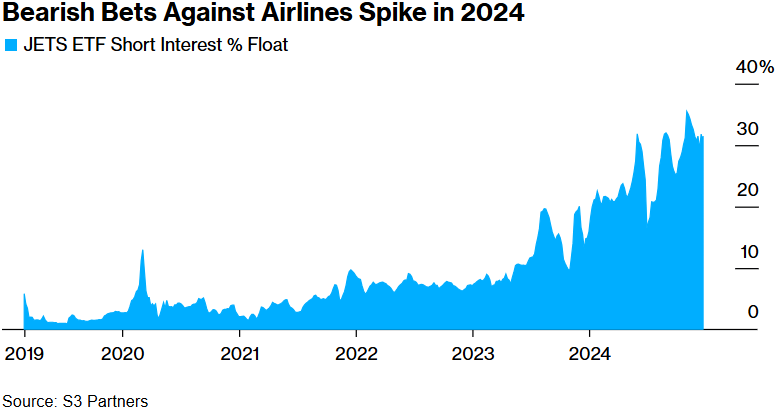

In 2024, bearish bets on Airlines are also increasing.

At the same time, the US Global Jets ETF (JETS.US), which has a scale of $1.1 billion, is the hottest ETF in the US market most closely associated with airlines focused on international travel routes. The recent growth in short positions related to the US Global Jets ETF has also risen alongside the surge in prices, indicating that some fund managers or retail investors do not believe that this long-underperforming US ETF's impressive increase of 36% this year can continue into early 2025, betting that the ETF may undergo significant adjustments.

Analyst Ravi Shankar from Morgan Stanley pointed out that the position size in the aviation/airlines industry remains very low among asset management institutions focusing on long-term strategies. However, he noted that the position size for leveraged hedge funds and retail investors has significantly rebounded. Shankar stated that if traditional asset management institutions focusing on long-term holdings increase their positions in the aviation/airlines industry, it means that the future outlook for this industry remains optimistic. He also mentioned that the threshold for exceeding investor performance expectations "is undoubtedly higher than it was 12-18 months ago," but "compared to the average performance growth threshold, it is still relatively low overall."