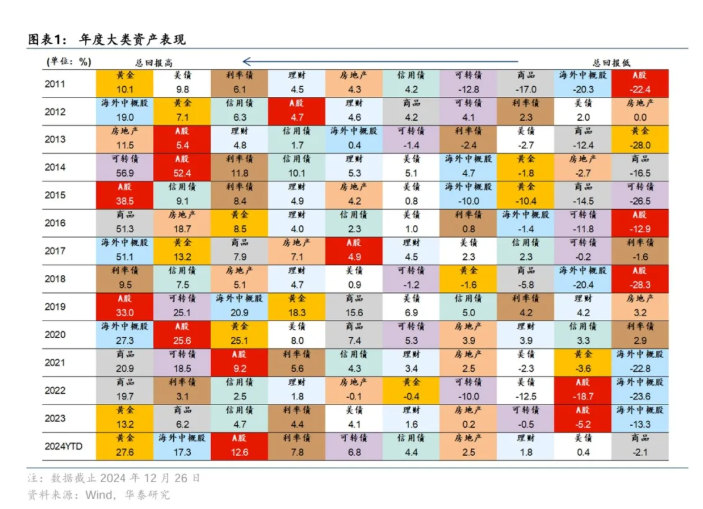

Huatai Fixed Income states that the leading Assets in 2024 will include Bitcoin, Gold, US stocks, and China long-term bonds, while lagging Assets will include domestic Commodities, Euros, and Crude Oil Product. From the perspective of the Industry and individual stocks, the leading Assets are backed by long-term trends such as changes in the AI Technology Industry Chain, China's emotional Consumer chain, and safe-haven Assets in an uncertain environment.

Core Viewpoint

Since 2024, the "exception theory" of US Assets, the strengthening of the theme of the era, and the frequent rotation of global funds are the three core factors driving the prices of major asset classes. In an uncertain environment, certainty and growth have become scarce assets. In terms of asset performance, the main line that continues in 2024 is "seeking certainty". Macro factors such as the Federal Reserve's interest rate cuts, the suspense of the US election, and the policy game in China are gradually being resolved, requiring greater precision and flexibility in investment operations. On the level of major assets, the assets that performed well in 2024 include Bitcoin, Gold, US Stocks, and China's Long Bonds, while poorly performing assets include domestic commodities, the Euro, and Crude Oil Products. From the perspective of industry and individual stocks, the leading assets are underpinned by changes in long-term trends such as the AI Technology Industry Chain, China's emotional consumption chain, and safe-haven assets in an uncertain environment.

Main text

Main text

Year-end review of major assets

As 2024 comes to a close, we conduct a year-end review of the performance of various assets. In an environment of rapid global fund rotation and international geopolitical turbulence, certainty and growth have become scarce assets, manifested in the strength of Gold and the repeatedly hit highs of US Stocks in AI, breaking traditional valuation frameworks. From the perspective of institutional behavior, market pricing power has changed hands multiple times, highlighting the differences in investors’ flexibility and allocation capabilities, with passive and flexible funds being favored. Looking back over the past year, we find that the asset performance embodies profound mainstream trends of the era. The financial market has witnessed miracles, while also presenting many interesting phenomena.

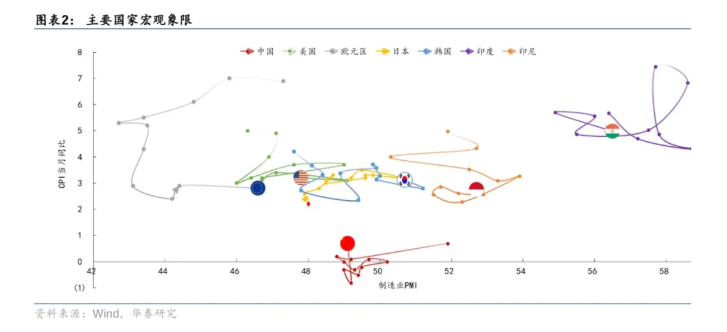

First, from a macro perspective, the global economy is also undergoing a profound transformation, with evident mismatch characteristics.

The US economy shows resilience, with increased policy uncertainty after the election, focusing on the rebalancing of economic growth and inflation.

The Chinese economy exhibits characteristics of low inflation, and the continued push for steady growth policies has reduced tail risks.

Japan is showing signs of re-inflation, with the central bank acting as a counterforce against the global trend of interest rate cuts, while political turmoil increases.

Europe is facing a competitiveness crisis, with constraints on economic recovery resilience.

Notably, Spain has emerged as the best-performing economy among developed countries, actively promoting structural reforms to achieve long-term economic growth. The Economist compiled data on five economic and financial indicators for 37 mainly developed countries in 2024, including GDP, stock market performance, core inflation rate, unemployment rate, and government deficit. Spain ranked first based on its economic performance, with both economic growth and employment growth exceeding that of the USA. In terms of industry structure, there is a shift from traditional manufacturing to emphasis on service industry development, driving growth through tourism. Diplomatically, an open policy towards immigration is maintained, along with active efforts in attracting investment. Thus, the developed tourism industry and immigrant employment growth contribute to local housing prices, while investment and production also support domestic economic growth.

In terms of asset performance, the main theme in the market for 2024 continues to be 'seeking certainty'. Macroeconomic factors such as the Federal Reserve's interest rate cuts, the US election, and the suspense of China's policy game will successively materialize, requiring greater precision and flexibility in investment operations. The core logic behind the rotation of global assets in 2024 is:

1. The 'exception theory' of USA Assets: In a high interest rate environment, the fundamentals of the USA remain resilient, with US stocks continuing to lead the upward trend for the past two years.

2. Strengthened themes of the era: The global election year combined with frequent geopolitical disturbances has led to a brewing impact of the era's background on asset prices, with Gold performing exceptionally, while the AI theme has begun to develop more deeply after over a year of 'crazy growth', with a surge of strong stocks in the related Industry Chain.

3. Frequent rotation of global funds: The valuation gap between different assets has widened, with global funds frequently rotating and switching between high and low, whether between countries (Japan, India/China), or between styles (large/small cap US stocks, domestic growth/dividend).

In terms of major asset categories, assets that are expected to perform well in 2024 include:

1) Bitcoin: Often regarded as a risk-on asset, primarily priced based on its de-dollarization attributes, regulatory relaxations following Trump's presidency, and strict supply constraints, with higher acceptance of Cryptos in developed countries like the USA.

2) Gold: Primarily a risk-off asset, driven by international turmoil, the USA's interest rate cut cycle, concerns regarding the sustainability of debt in developed countries affecting the US dollar monetary system, along with central banks in Emerging Markets purchasing Gold, leading to record high Gold prices.

3) Stocks in the USA: The fundamentals of the USA remain resilient in a high interest rate environment, making US stocks a leading asset over the past two years, driven by corporate profit growth from the AI Technology revolution and a soft landing interest rate cut wave, with temporary adjustments during the process of crowded positions.

4) China's long-term bonds: weak price signals + real estate downturn cycle + loose monetary policy + significant institutional allocation pressure, domestic interest rates continue to decline, duration strategy achieves high capital gains.

Assets that underperformed throughout the year include:

1) Domestic Commodities: The real estate market continues to cool, with supply-demand contradictions worsening, the commodity market showing more trading realities, and a noticeable pullback in domestic black commodities;

2) Euro: The recovery pace of Europe's fundamentals is significantly weaker than that of the USA, with Germany and others undergoing fiscal tightening, presenting tail risks, leading to a weak operation of the euro under the interest rate differential logic.

3) Crude Oil Product: The demand side is constrained by the high interest rate environment lacking strong driving forces, while the supply side faces potential production increase pressure from OPEC and the USA, compounded by Trump's trade actions, resulting in a weaker commodity.

From the perspective of industry and individual stocks, leading assets reflect changes in long-term trends:

1) AI Technology Industry Chain: A year after the emergence of ChatGPT, trading has gradually returned to rationality from the initial frenzy, but its popularization speed far exceeds that of other historical technological revolutions. Large technology companies with platform advantages and businesses with barriers in specific vertical fields still hold significant advantages. The AI technology revolution has triggered an "arms race" among companies, leading to an exponential increase in computing power demand. The hardware manufacturer NVIDIA, benefiting as the "shovel seller," has seen its stock rise significantly, with an increase of 179% since the beginning of 2024. Additionally, the diffusion of AI hardware to upstream infrastructure like electrical utilities and downstream software has occurred, with Vistra Energy, which provides infrastructure services, increasing over 270% since the beginning of the year. The USA's Mag7 has recorded a 70% increase since the beginning of the year, leading the US stock market, making long positions in US technology stocks the most sought-after and crowded trading line in 2024. Domestic reflections include Cambrian (with a recent increase of over 380%) and the recent AI application "Doubao" concept.

2) The emotional consumption chain in China: In an environment where consumer sentiment is declining, the market space for segmented areas such as emotional consumption, self-indulgent consumption, and fan economy is experiencing strong growth with advantages and barriers. Although traditional consumer demand remains sluggish, self-indulgent consumption represented by the "Guzi Economy" is developing rapidly, with "Guzi Products" based on two-dimensional IP generating high added value and experiencing rapid market growth. Among them, POP MART, as the leading company in the advantageous industry, reported a revenue growth of 120% to 125% year-on-year in the third quarter of 2023, with performance exceeding market expectations for several consecutive quarters, and an annual stock price increase of more than 300%.

3) Safe-haven assets in an uncertain environment: The main market trend over the past two years has been in search of certainty, with high-dividend assets such as Precious Metals and Bank Stocks becoming advantageous assets in a declining interest rate environment and low-risk appetite, seeking performance certainty. Throughout the year, the banking sector's increase exceeded 40%, yielding nearly 20 percentage points of excess return over the Csi 300 Index, ranking among the best across various sectors. On one hand, this may be due to the more favorable risk-return profile of the banking sector, attracting the preference of low-risk capital such as insurance funds; on the other hand, the banking operations remain relatively stable, achieving a 10% ROE and positive profit growth through provisioning adjustments, which has made them a focal point for safe-haven fund allocations in the absence of a main market trend.

Author of this article: Zhang Jiqiang and He Yingwen from HTSC Fixed Income Research, original title: "[HTSC Asset Allocation] Weekly Review: Year-End Summary of Major Assets"

Zhang Jiqiang S0570518110002 Researcher

He Yingwen S0570522090002 Researcher