Waiting for the predicament to turn around.

Author | Lone Ranger

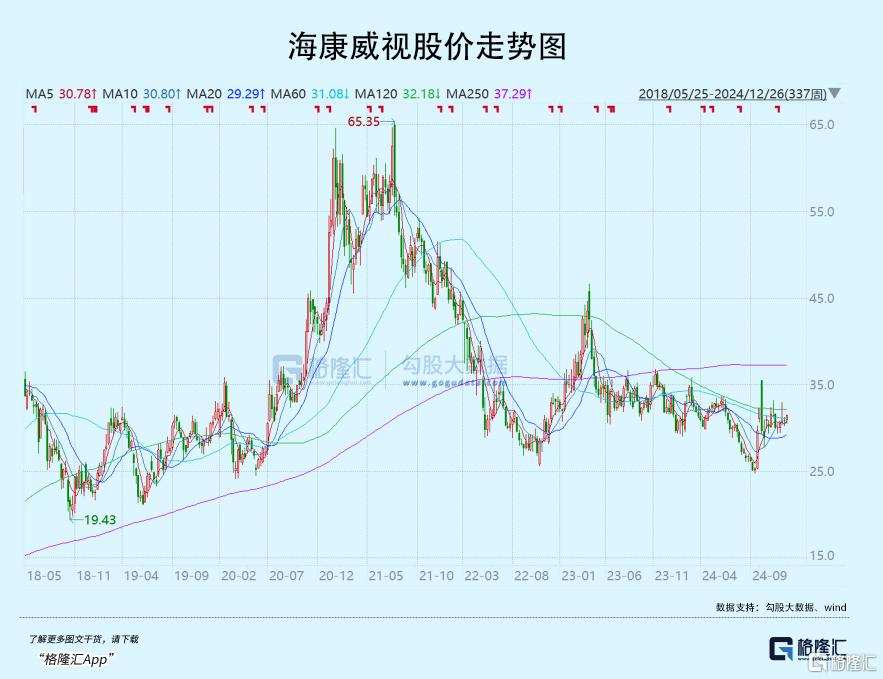

Data Support | Pythagoras Big Data ()

Since the beginning of this year, as AI large models have ignited a new wave of technological industry upgrades globally, many domestic and international software and hardware technology giants have experienced explosive growth in their stock prices.

However, as one of the once most core star blue-chip stocks in the A-shares, Hangzhou Hikvision Digital Technology, which has a high hard technology attribute, seems to have disappointed investors with its stock price trend.

Since the peak in July 2021, Hangzhou Hikvision Digital Technology has dropped by a cumulative 50%, with a market cap evaporating by over 300 billion yuan, and its stock price has fallen by 9.27% this year, which is quite rare among numerous hard technology giants.

Why has Hangzhou Hikvision Digital Technology's market performance been so sluggish? More importantly, can it bounce back in the future?

01

Hangzhou Hikvision Digital Technology has been on a downward trend for three and a half years, with a brief rebound due to AI Concept, but it quickly faded. The deeper reason lies in the company's ongoing poor fundamental performance.

Before and in 2021, Hangzhou Hikvision Digital Technology maintained double-digit growth in revenue and net income attributable to shareholders for many years, and the market was happy to give growth stocks a high valuation. However, after that, the company's performance suddenly hit the brakes, in stark contrast to previous high growth.

In 2022-2023 and the first three quarters of 2024, the revenue growth rates of Hangzhou Hikvision Digital Technology were 2.14%, 7.42%, and 6.06% year-on-year, while the year-on-year net income growth rates were -23.59%, 9.89%, and -8.4%, respectively.

Looking at the company's profitability, by the end of the third quarter of 2024, the sales gross margin was 44.76%, remaining relatively stable, but still down 1.77 percentage points from 46.53% in 2020. In terms of net margin, the latest figure is 13.71%, significantly down 7.8 percentage points from 21.5% in 2021.

The significant disparity in gross margin and net margin is mainly due to the continuous rise in the three expenses ratio of Hangzhou Hikvision Digital Technology. On one hand, the sales expense ratio has continued to increase to the latest 13.37%, hitting a new high since 2006 when financial data was disclosed, rising significantly by 2.82 percentage points compared to 2021. This to some extent indicates that competition in the security market has become more intense.

On the other hand, the company's R&D expense ratio continues to rise, currently at 13.44%, a significant increase of 3.31 percentage points compared to 2021. Generally speaking, a company that significantly increases its R&D investment is beneficial for enhancing market competitiveness in the long run; however, in the short to medium term, it can greatly harm the company’s profitability.

For Hangzhou Hikvision Digital Technology, increasing R&D investment may be a necessity. One major characteristic of the security market is that users, applications, and products are dispersed, and there is a high customization attribute among customers. Fragmented scenarios also require companies to continuously increase investment to meet market demands.

In addition, the security industry has gradually entered the smart era since 2016, evolving from traditional security facilities to providing comprehensive solutions through the Internet of Things, Big Data, and AI technology, involving major areas such as safe cities and smart transportation. Since 2020, the security market has increasingly shown a trend of transforming and upgrading from hardware and software product sales to data operation and Cloud Computing services.

The security industry is facing market and technological changes while being pressured by the USA, along with strong competitors like Huaw in the market. Hangzhou Hikvision Digital Technology may only maintain its original market position by increasing R&D investment and enhancing product competitiveness.

This is actually similar to the fate of most manufacturing enterprises; due to constant changes in market demand and industry technology, substantial investment is needed to maintain the existing business foundation and growth. This is incomparable to high-end Consumer business models like Kweichow Moutai, which hardly requires R&D, as the market structure is quite stable, relying on brand power for continuous price increases and sustained improvement in performance and profitability (of course, the Baijiu industry is also currently facing significant growth pressure issues).

02

Looking ahead, is there hope for Hangzhou Hikvision Digital Technology to return to rapid growth?

This requires analysis from the perspectives of domestic security business, overseas security business, and innovative business.

Hangzhou Hikvision Digital Technology's domestic security business is mainly divided into three parts: the Public Services Group (PBG), the Enterprise Business Group (EBG), and the Small and Medium Business Group (SMBG). The PEG business, represented by government clients, was once the largest source of revenue for Hangzhou Hikvision Digital Technology, but since 2021, it has become a drag on the overall business performance.

From 2021 to 2023, Hangzhou Hikvision Digital Technology's PBG revenue declined from 19.161 billion yuan to 15.354 billion yuan, a total decline of 20%. In the first half of 2024, the revenue was 5.693 billion yuan, again declining more than 9% year-on-year.

It is evident that PBG business growth has hit a ceiling. The reason for this is directly related to the sharp decline in local government fiscal revenues, which is closely tied to the Real Estate cycle. It is important to note that 2021 was the year when land finance saw a turning point, with total land sales income of 8.7 trillion yuan, which dropped to only 5.8 trillion yuan in 2023, a reduction of 2.9 trillion yuan.

The continued sharp decline in land revenue, combined with the need for localities to resolve hidden debt risks, has led to a very tight financial situation for local governments, which naturally tends to reduce investments in urban public services such as security. This is actually a deeper reason for the continued decline of Hangzhou Hikvision Digital Technology's PBG business.

Moreover, due to factors such as population decline and high household leverage, the Real Estate cycle in China is unlikely to return to the prosperous periods of the past.

As a result, the pressure on Hangzhou Hikvision Digital Technology's PBG business in the future can be said to be ever-present.

In addition to the PBG business, the company's EBG and SMBG businesses have also slowed down, with year-on-year growth rates of only 7.05% and 0.64% respectively in the first half of 2024. These B2B businesses are closely related to the pressure on the macro economy, and related demand will take a significant amount of time to clearly recover.

In terms of overseas Business revenue, from 2021 to 2023, it was 18.926 billion yuan, 22.032 billion yuan, and 23.977 billion yuan respectively, with year-on-year growth rates of 15.09%, 16.41%, and 8.83% respectively. It is evident that the development momentum of the overseas market has indeed slowed down.

The reason is that before 2018, the overseas market was in a globalized environment with fewer obstacles to overseas expansion. However, afterwards, the trend of de-globalization has become increasingly apparent, especially with Trump's re-election as president of the USA, which might lead to significant tariffs on other countries, negatively impacting the performance of the global economy and intensifying the tearing of globalization.

In such a situation, Hangzhou Hikvision Digital Technology's layout in the overseas market has inevitably been affected. In fact, another domestic security leader, Zhejiang Dahua Technology, had already sold its wholly-owned subsidiary in the USA due to geopolitical impacts and withdrew from the American market.

Therefore, Hangzhou Hikvision Digital Technology has tightened the allocation of resources towards developed countries' markets, while redirecting more resources to developing countries. Of course, the market scale of developing countries is smaller, but the growth rate is comparatively higher.

According to Caitong's Statistics, the year-on-year compound growth rate of the Southeast Asian security market, led by India, Thailand, and Indonesia, has been 20%-30% in recent years, higher than that of the European market led by the UK, France, and Germany, as well as the North American market.

Overall, the overseas market still presents significant opportunities for Hangzhou Hikvision Digital Technology, but the challenges cannot be overlooked.

In addition, Hangzhou Hikvision Digital Technology has also long placed part of its efforts on innovative Business, attempting to build new growth engines. This mainly includes Robotics, Smart Home, thermal imaging, automotive electronics, and storage Business.

From 2018 to 2021, the compound annual growth rate of Hangzhou Hikvision Digital Technology's innovative Business revenue was 65.7%. In 2022-2023, as the Business volume increased, it gradually slowed down to over 20%, showing strong growth potential.

However, currently, the revenue from innovative business is an order of magnitude lower than the main security business, and it will take considerable time to grow into a new major growth engine in the future.

03

Due to the decline in Hangzhou Hikvision Digital Technology's fundamentals, the attitude of institutions led by public funds has also changed significantly, with many reducing their shareholding levels.

As of June 30, 2021, public funds held more than 1.5 billion shares of Hangzhou Hikvision Digital Technology, with a market cap of up to 87 billion yuan, ranking as the fifth largest heavy stock, second only to Kweichow Moutai, Contemporary Amperex Technology, Wuliangye Yibin, and TENCENT. At that time, it also received favor from top fund managers like Zhang Kun, Liu Yanchun, Xie Zhiyu, and Zhou Yingbo.

However, with the decline in performance and stock price, the latest number of shares held by public funds in Hangzhou Hikvision Digital Technology has dropped to only 0.35 billion shares, a decline of over 75% from the peak, and top fund products have also successively withdrawn.

However, Feng Liu of Gao Yi Assets has moved against the trend; since entering the top five shareholders in the third quarter of 2020, he has maintained and increased his holdings, with the latest holding ratio being 4.24%, a market cap of up to 12.16 billion yuan (as of December 19, slightly reduced by 0.22% from the end of the third quarter), ranking as the fourth largest shareholder. However, it appears that Feng Liu, the private equity star, has not achieved ideal returns, experiencing a roller coaster.

In addition, northern-bound funds have seen their holdings drop from nearly 10% to 0.68% as of September 30, 2024, due to various factors such as the "entity list" and fundamentals, with a holding market value of only about 2 billion yuan.

From a valuation perspective, Hikvision's current PE valuation is 21.76 times, which is at a low level for the past decade. Nowadays, many domestic Technology sectors are rapidly reinvigorating under the AI boom, and there's hope that Hikvision, as a core leader in the security field, will see its valuation rise sooner rather than later. (End of text)