Seeking Alpha知名撰稿人The Asian Investor近日发文称,执着于估值对于有可能在短期内实现业绩剧增的AMD来说毫无意义,当它被持续大幅抛售时正是“逢低买入”的绝佳良机,当前资金流显示逢低买盘正在持续涌入该股,推动AMD近日超跌反弹步伐;并且长期有一股势力押注它将蚕食英伟达在数据中心AI芯片领域高达90%的份额,这也是它估值长期高企的逻辑。

Seeking Alpha知名撰稿人The Asian Investor近日发文称,执着于估值对于有可能在短期内实现业绩剧增的AMD来说毫无意义,当它被持续大幅抛售时正是“逢低买入”的绝佳良机,当前资金流显示逢低买盘正在持续涌入该股,推动AMD近日超跌反弹步伐;并且长期有一股势力押注它将蚕食英伟达在数据中心AI芯片领域高达90%的份额,这也是它估值长期高企的逻辑。Source: Zhithon Finance

Author: Rousseau

AMD can be considered the strongest force to challenge NVIDIA's monopoly in the AI infrastructure field in the coming years.

Leaders in the PC and Datacenter Chip fields. $Advanced Micro Devices (AMD.US)$ The stock price recently plummeted below $120, and although investor sentiment has been negatively impacted, some Institutions still believe its risk profile is quite attractive for investment, and even some Wall Street investment firms are betting that AMD's stock price may reach the historical high of $200 within the next 12 months. Additionally, there is still a group of 'AI faithful' betting that AMD's Datacenter Business Segment will demonstrate huge growth potential with the MI300X and subsequent updates of its AI product line, enabling it to compete against NVIDIA's absolute dominance in the Datacenter AI GPU market.

Seeking Alpha's well-known contributor, The Asian Investor, recently stated that focusing on valuation is meaningless for AMD, which could see a significant performance surge in the short term. The recent heavy sell-off presents a great opportunity for ‘buying the dip’. Current funding flows indicate ongoing Bid activity into the stock, driving AMD's recent oversold rebound; additionally, there is a long-term force betting it will capture up to 90% of NVIDIA's share in the Datacenter AI Chip sector, which also explains its high valuation over the long term.

Seeking Alpha's well-known contributor, The Asian Investor, recently stated that focusing on valuation is meaningless for AMD, which could see a significant performance surge in the short term. The recent heavy sell-off presents a great opportunity for ‘buying the dip’. Current funding flows indicate ongoing Bid activity into the stock, driving AMD's recent oversold rebound; additionally, there is a long-term force betting it will capture up to 90% of NVIDIA's share in the Datacenter AI Chip sector, which also explains its high valuation over the long term.

AMD's increasingly mature Software and Hardware collaborative ecosystem, along with more Cloud Computing giants like Oracle and Microsoft ramping up their purchases of AMD's AI GPUs, Server CPUs, and other AI Hardware infrastructure from the AMD ecosystem, positions AMD as the strongest force to challenge NVIDIA's monopoly in the AI infrastructure sector in the coming years. The Asian Investor noted that AMD's upcoming M300X AI GPU upgrade version – MI325X, along with the MI350 and MI400 series expected in the next year or so, combined with the vigorous growth of its Server CPU-led Datacenter business, is expected to significantly boost AMD's revenue, gross profit, and free cash flow by FY2025.

Since AMD released its third-quarter Earnings Reports in October, its stock performance has disappointed investors. Although AMD reported that its Datacenter Business revenue for the third quarter ending in September grew more than double year-on-year, the relatively modest total revenue outlook for the fourth quarter has created significant negative sentiment among U.S. stock market investors.

A series of major AI products from Advanced Micro Devices may drive a sharp increase in performance. Is it already a good opportunity to buy on the dip?

Benefiting from the AI boom, storage giant Micron Technology (MU.US) recently released revenue forecasts for the current fiscal quarter that fell significantly short of market expectations, further exacerbating the downward pressure on valuations and stock prices of many semiconductor giants, including AMD, undoubtedly intensifying the market’s negative sentiment. However, with AMD’s stock price recently dropping to around $120, and AI ASIC leader Broadcom (AVGO.US) expressing extreme optimism regarding AI Chips and related infrastructure, promising to challenge NVIDIA's monopoly, AMD's latest risk profile seems very attractive, potentially leading to a massive influx of 'buying the dip'.

After AMD submitted its third quarter earnings report, due to its promising product line in AI accelerators, The Asian Investor from Seeking Alpha strongly recommends buying AMD Stocks on dips, and this renowned financial commentator emphasized that the strong expectations from "AI believers" and some investment Institutions for the rapid revenue growth of AMD's Datacenter business are hardly reflected in AMD's recent stock price and Market Cap after its sharp decline.

The Asian Investor wrote: "AMD has strong momentum in its Datacenter business, but I think investors have not fully recognized this... Currently, over half of the company’s total revenue comes from Datacenter. As AMD plans to increase the delivery of its MI300X Instinct AI GPU products in the fourth quarter and fiscal year 2025, AMD has significant potential to encroach on NVIDIA's near-monopoly in the Datacenter AI GPU market, which has dominated the Datacenter AI infrastructure hardware market for the past two years. The continued high valuation of AMD means nothing to me; I believe its risk situation is extremely attractive for investment right now."

AMD entered the Datacenter AI infrastructure hardware market relatively late, thus long lagging behind NVIDIA, but recently, with the launch of its AI GPU that surpasses the performance of NVIDIA's Hopper architecture and a continuously improving ecosystem for hardware-software collaboration, it has finally caught up with the MI300X Datacenter AI GPU. This AI GPU provides Datacenter operators with a hardware alternative surpassing the overall performance of NVIDIA's H100/H200 AI GPUs. Given the current tight supply of NVIDIA's H100/H200 and Blackwell GPUs, cloud computing giants like Oracle are beginning to shift towards AMD AI hardware infrastructure, making the shipping prospects for MI300X increasingly optimistic.

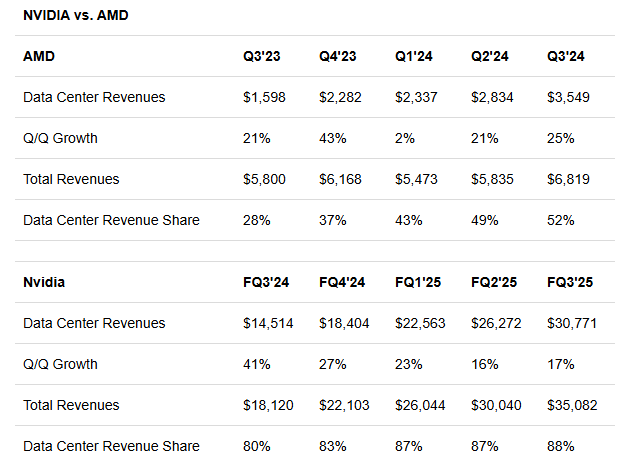

The Asian Investor stated that despite NVIDIA’s significant increases in revenue, gross profit, and earnings due to the outstanding success of H100/H200 and Blackwell in the Datacenter sector, it still enjoys a clear advantage over AMD, namely that its thriving Datacenter business accounts for a much larger share of its total revenue: in the most recent quarter, the Datacenter business constituted 88% of total revenue, whereas AMD only accounted for 52%. However, The Asian Investor emphasized that AMD's share of revenue in the Datacenter business has greatly increased over the past year, nearly doubling year-on-year, indicating that if this momentum continues, AMD's total revenue will also accelerate growth, which is a part that the market has not fully priced in.

AMD's product line is very comprehensive, with plans to release a new AI GPU—MI325X, along with the MI350 series AI accelerators, by 2025. Institutions on Wall Street generally expect this to significantly boost the company’s Datacenter business revenue. With over half of AMD’s total revenue currently coming from Datacenter (compared to about a quarter in the third quarter of 2023), the accelerated growth of Datacenter business revenue is also expected to significantly drive AMD's overall revenue growth, as well as gross profit and free cash flow, further elevating its valuation and stock price.

AMD, the strongest competitor to NVIDIA in the field of PC discrete graphics cards and Datacenter Server AI GPUs, is doing its utmost to quickly launch new server AI GPUs and edge AI chips suitable for AI PCs, attempting to weaken NVIDIA's absolute dominance of up to 90% in the lucrative Datacenter AI Chip market while striving to gain an early competitive advantage over peers in the edge AI market.

The MI300X AI accelerator developed by AMD has significant advantages in memory bandwidth and capacity compared to NVIDIA's Hopper architecture AI GPU, making it particularly suitable for the demanding parallel computing workloads of generative AI model training and inference tasks. Oracle's collaboration with AMD to build an AI supercomputing center indicates that AMD has formidable competitiveness in hardware design and AI-related software ecosystem support, especially in the integration of hardware and software systems required for high-performance computing and AI workloads. For AMD, which currently has less than 10% market share in the datacenter AI GPU market, there is an opportunity to leverage Oracle's substantial influence in the global Cloud Computing services market to expand the MI300X's market share in the datacenter AI GPU sector.

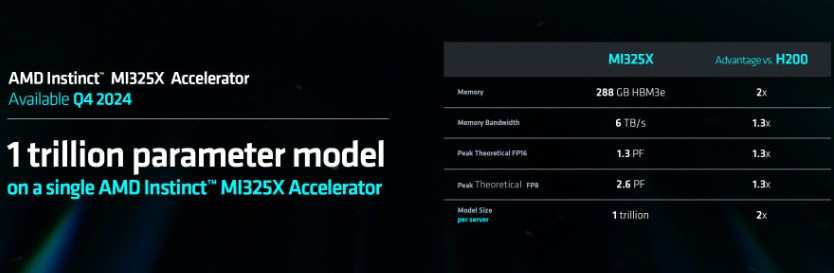

The upgraded version of AMD's M300X designed for datacenter AI servers—the MI325X—will begin mass production and sales in the fourth quarter, while AMD's more advanced MI350 series will be launched in 2025, and the MI400 series will follow a year later. AMD's newly introduced MI325X continues the robust CDNA3 architecture based on TSMC's 3nm manufacturing process and, like NVIDIA's H200, employs a fourth-generation HBM memory system—HBM3E, significantly increasing memory capacity to 288GB and bandwidth to 6TB/s, greatly enhancing overall performance; other benchmark specifications and compatibility largely remain consistent with the MI300X, facilitating a smooth upgrade transition for AMD customers.

Dr. Su expressed that the performance enhancement of the MI325X AI is the largest in AMD's history, with over a 1.3 times improvement compared to the competitor NVIDIA H200; the peak theoretical FP16 of AMD MI325X is about 1.3 times that of H200, with memory bandwidth also 1.3 times that of H200, based on the model size per Server being 2 times that of H200.

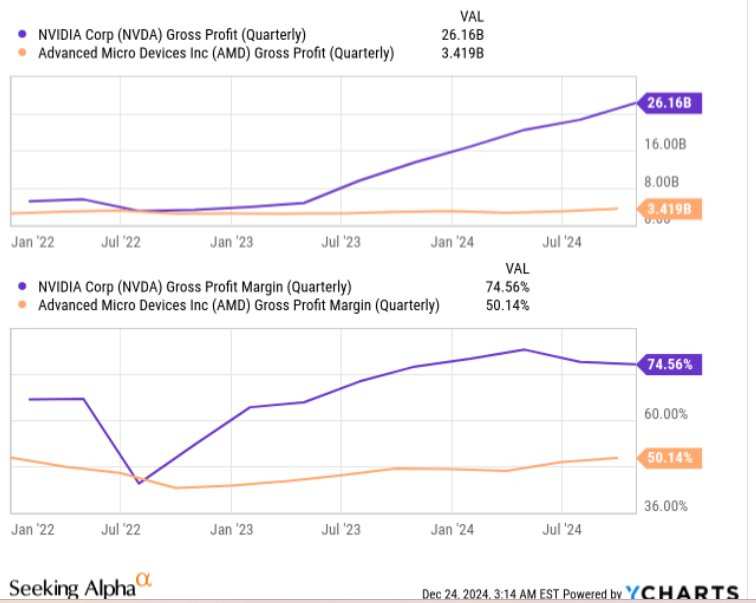

Some Wall Street Analysts noted that in terms of gross profit, NVIDIA's profitability still far exceeds that of AMD, but AMD's gross profit trend also shows significant improvement, which is directly related to the company's success in the datacenter AI GPU market. When the next generation of AI GPU products at higher prices comes to market next year, if AMD accelerates in capturing NVIDIA's market share, it may even have greater potential to expand its gross margin.

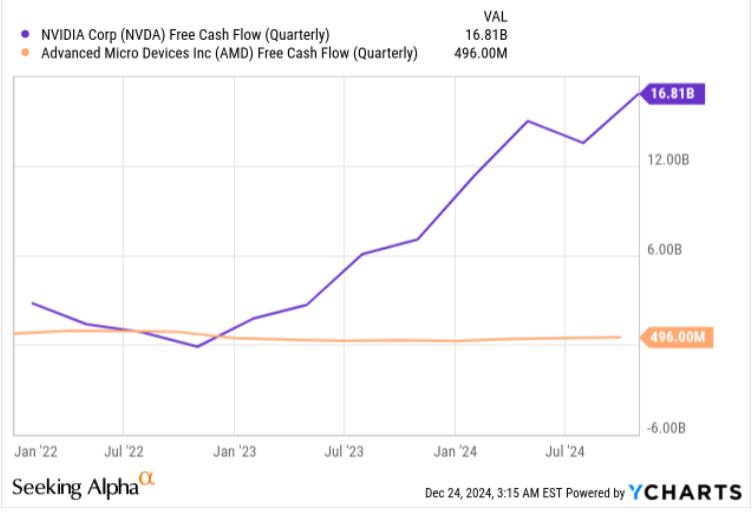

NVIDIA's free cash flow grew by 138% last quarter, while AMD's grew by 67%, with NVIDIA's growth rate of this important metric being twice that of AMD. However, AMD has the potential to catch up to NVIDIA, primarily due to its datacenter business showing strong growth momentum in the second and third quarters of 2024. The Asian Investor states that although AMD is currently lagging significantly behind NVIDIA in datacenter business growth rates, the substantial increase in shipments of MI300X, MI325X, and MI350X could have a significant impact on the performance of this semiconductor giant in 2025.

The globally renowned strategic consulting firm Bain predicts that the rapid proliferation of Artificial Intelligence (AI) technology is disrupting businesses and the economy, with all markets related to AI expanding, reaching 990 billion USD by 2027. In its fifth annual Global Technology Report released on Wednesday, the consultancy pointed out that the overall AI market, including AI-related services and foundational hardware, will grow annually by 40% to 55% from last year’s 185 billion USD. This means that revenues will amount to between 780 billion to 990 billion USD by 2027.

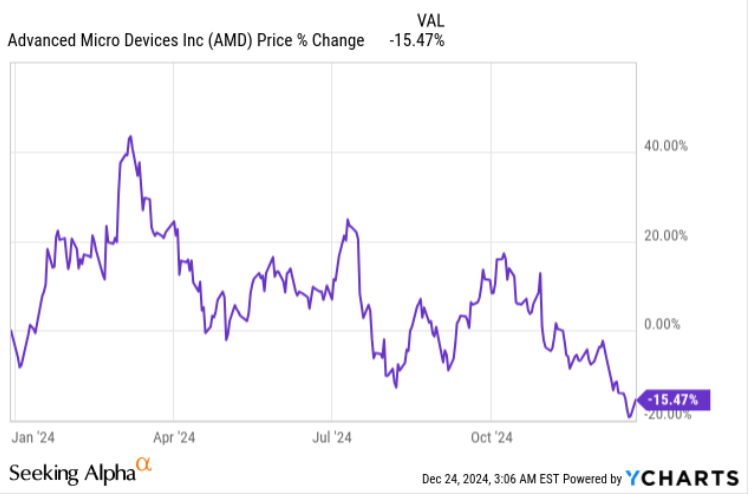

This year, with stock prices continuing to languish, is AMD gearing up to challenge 200 USD?

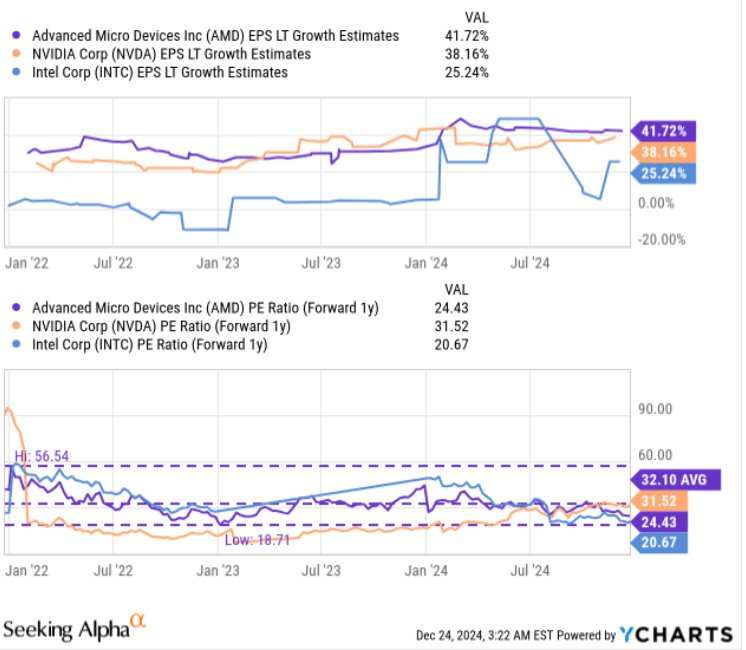

The Asian Investor stated that, in addition to having a promising product line in MI300X, MI325X, and MI350X AI acceleration hardware, AMD's valuation currently shows a certain competitive advantage over the expensive NVIDIA.

There’s no doubt that NVIDIA remains the highest-valued semiconductor company in the US stock market, with an expected PE of 31.5x. On the other hand, AMD currently has an expected PE of about 24.4x, which far exceeds the industry valuation, but is at a 24% discount to AMD's long-term benchmark—the 3-year average PE—and surprisingly presents a 22% discount compared to NVIDIA's latest valuation. Just about three months ago, NVIDIA and AMD had roughly the same expected PE. However, NVIDIA has extremely strong investment positioning and a continuously warming performance outlook, which is why Wall Street believes investors should seize the opportunity to buy NVIDIA on dips.

AMD's outlook for the fourth quarter of 2024 disappointed investors—the semiconductor company anticipates revenue of about 7.5 billion USD, fluctuating by 0.3 billion USD, while the market expected 7.6 billion USD—resulting in negative market sentiment that has caused AMD's stock price to continue to plummet, down as much as 15% this year, significantly underperforming the S&P 500 Index, while NVIDIA’s impressive 180% increase cannot be compared. However, some analysts believe this pricing is unreasonable. First, the expected deviation of AMD is only slight (expected revenue benchmark of 7.5 billion USD, while the expectation is 7.6 billion USD); secondly, AMD's datacenter business segment has already seen a significant upward trend in revenue, directly related to MI300X Instinct.

The Asian Investor stated in its latest article that, based on a fair value at an expected PE of 36x and an expected earnings range of 6-7 USD per share for fiscal year 2025, AMD's stock fair value is between 216-252 USD per share, while the market currently expects only 5.10 USD per share in earnings next year. AMD's latest closing price was 126.290 USD, which shows significant upside potential compared to The Asian Investor’s expectations.

Given that this semiconductor giant has achieved encouraging growth in the datacenter AI infrastructure field and the shipment of AI GPUs is significantly increasing, especially in the first half of 2025, The Asian Investor believes the market’s expectations may be overly conservative. Considering the potential significant growth drivers for AMD's datacenter business and its management’s strong execution in 2024, this financial writer believes AMD's current stock price compared to expected EPS is unreasonable.

Based on the current price and valuation, analysts have pointed out that buying AMD on dips will not only yield "Christmas and New Year gifts," but this semiconductor giant is at the forefront of significant revenue growth related to datacenters, which should simultaneously enhance AMD's gross profit and free cash flow for the fiscal year 2025. AMD's AI product line might be the best for the company in years, especially the AI GPUs aimed at data center operations and the constantly optimized and improved ROCm software ecosystem. Through its MI300X AI accelerator and the ROCm software acceleration ecosystem, AMD is indeed a formidable force challenging NVIDIA's dominance in datacenter AI infrastructure.

Despite NVIDIA's stock price having recently consolidated, from the perspective of expected price-to-earnings ratio, AMD's stock price is currently about 22% cheaper than NVIDIA, which may lead more US investors focusing on the artificial intelligence investment craze to buy AMD on dips before the market recovery in 2025. Particularly, AMD's datacenter business has several catalysts, the most important being the launch of next-generation AI accelerator hardware in fiscal year 2025, which may become the core catalyst for significant expansion in AMD's datacenter business.

On Wall Street, there are many investment institutions that are bullish on AMD. Roth MKM, Citigroup, and Benchmark are all optimistic about AMD hitting $200 in the next 12 months and reiterate a "Buy" rating; the major international bank UBS Group is bullish up to $205, and another well-known investment institution Rosenblatt Securities is even more bullish at $250. The Asian Investor has provided a target price range of 216-252, and these bullish target price expectations for AMD entering a bull market indicate that the stock has a very high possibility of once again challenging the $200 mark after a 10-month hiatus, with AMD's new round of "main rising wave" primed to start.

Editor/Jeffy