其次,大摩预计2025年对美债的需求将强于预期,主要是由银行、外资和养老基金的买盘推动,这将使长期美债收益率仍保持在较低水平。

其次,大摩预计2025年对美债的需求将强于预期,主要是由银行、外资和养老基金的买盘推动,这将使长期美债收益率仍保持在较低水平。Morgan Stanley believes that the fiscal deficit in the USA is expected to decrease next year, while the fiscal deficits in China and Germany are likely to increase, which may lead to a convergence of interest rates between the USA and Europe, subsequently triggering a significant depreciation of the dollar. In addition, Morgan Stanley also anticipates a strong recovery in the demand for US Treasury bonds, that the euro is expected to "shine brightly," and that the Bank of England may shorten the interest rate cut cycle.

As 2024 is about to pass, on December 20, the global macro team led by Morgan Stanley analysts Matthew Hornbach and Andrew M Watrous published the latest research report outlining the top ten unexpected events that may occur in the global capital markets next year.

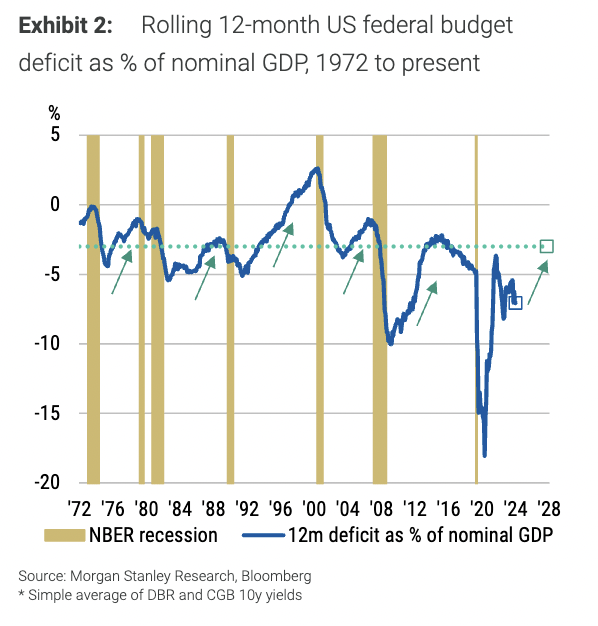

Specifically, Morgan Stanley expects that next year the fiscal deficit in the USA may not be as aggressive as anticipated, whereas fiscal expenditures in Germany and China will expand, indicating that interest rates in the USA, Europe, and China will converge, which would subsequently lead to a significant depreciation of the dollar.$USD (USDindex.FX)$It is expected to reach a level of 101 by the end of next year and face greater downside risks.

Secondly, Morgan Stanley anticipates that demand for U.S. Treasury bonds in 2025 will be stronger than expected, primarily driven by bids from banks, foreign capital, and retirement funds, which will keep long-term U.S. Treasury yields at low levels.

Secondly, Morgan Stanley anticipates that demand for U.S. Treasury bonds in 2025 will be stronger than expected, primarily driven by bids from banks, foreign capital, and retirement funds, which will keep long-term U.S. Treasury yields at low levels.

Despite the market's generally pessimistic view on the euro's trajectory, Morgan Stanley believes that under the circumstances of stronger-than-expected interest rate cuts, trade shocks that are less severe than anticipated, and large-scale capital repatriation, the euro is likely to 'shine brightly'.

With interest rates in the USA, Europe, and China converging, the dollar may face significant depreciation.

Morgan Stanley believes that the fiscal deficit in the USA is expected to decrease next year, while the fiscal deficits in China and Germany are likely to increase, potentially leading to a convergence of interest rates in the USA, Europe, and China, subsequently prompting a substantial depreciation of the dollar.

The nominated next U.S. Treasury Secretary, Becerra, previously stated that reducing the deficit-to-GDP ratio to 3% would be a priority. Morgan Stanley noted in the report that this commitment is widely considered difficult to achieve in the next presidential term, but there may be some progress in 2025.

The report indicates that considering the potential shift towards more conservative fiscal policy in the USA by 2025, the yields on US Treasury Bonds will decline to levels below expectations. Morgan Stanley forecasts that the USD could reach 101 by the end of 2025, with increased downside risks.

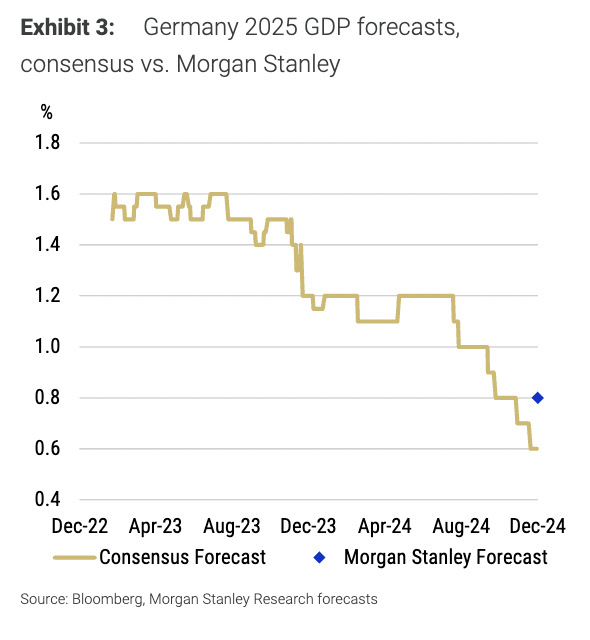

Regarding Germany, the largest economy in the Eurozone, the report suggests that the upcoming elections in February next year will likely reduce policy uncertainty with the formation of a new government, thereby boosting economic growth and providing room for more financial spending.

The report anticipates that Germany's economic growth rate will reach 0.8% in 2025, exceeding the general expectation of 0.6%.

As of the time of writing, the USD is reported at 108.108.

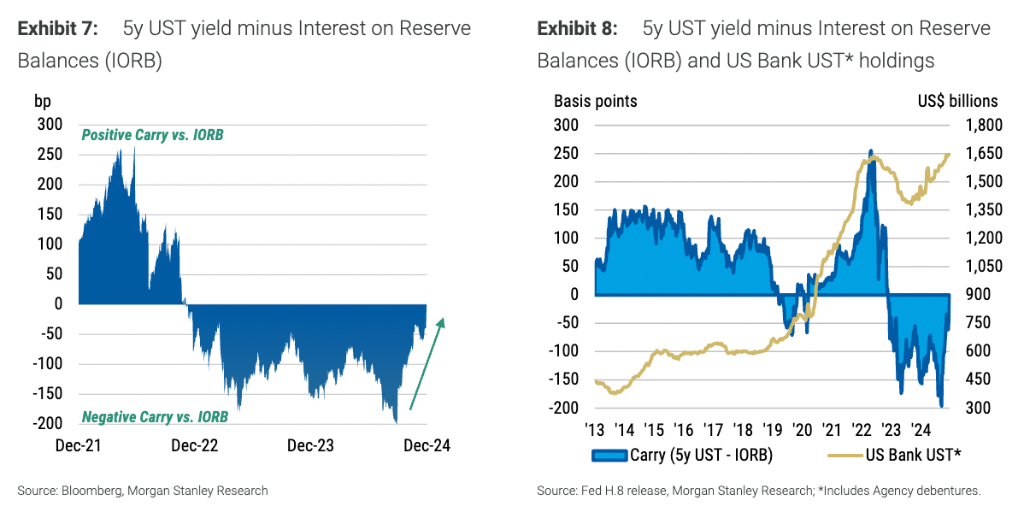

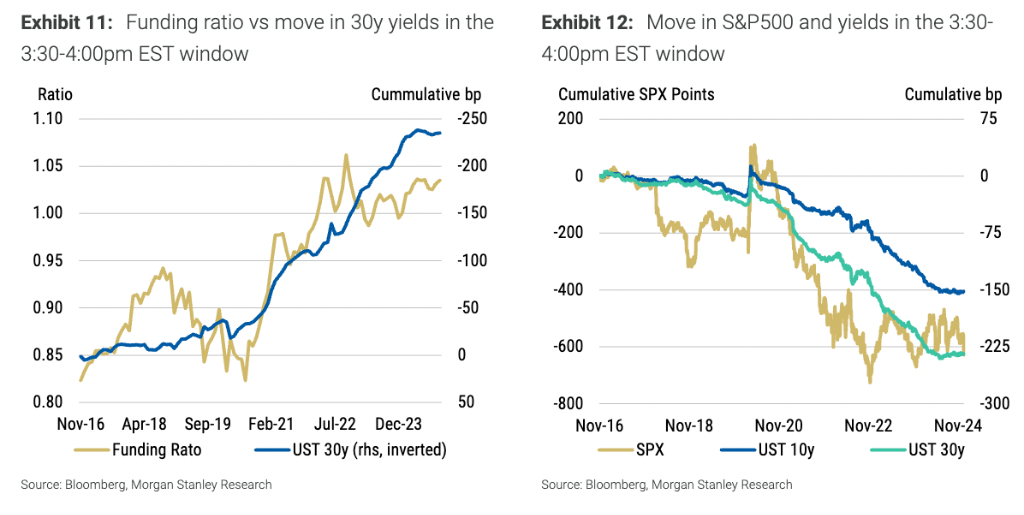

The demand for US Treasury Bonds has strongly recovered, with long-term bond yields continuing at low levels.

The report believes that the demand for US Bonds in 2025 will be stronger than expected, primarily driven by the Bids from Banks, foreign capital, and Retirement Funds.

Based on the expectation that inflation and deficit prospects under Trump's return to the White House will drive up long-term US Bond yields, investors have been selling long-term US Bonds in the fourth quarter of this year. However, Morgan Stanley disagrees with this viewpoint and expects long-term US Bond yields to remain at low levels until next year.

The report states that the downward trend in long-term US Bond yields next year will not only increase buying pressure but also the structural demand may be stronger than expected, mainly coming from the Bids of Banks, foreign capital, and Retirement Funds.

On the Banks' side, the increased uncertainty of the Federal Reserve's policy path will lead to Banks increasing their holdings of US Treasury Bonds, especially since the medium and long-term US Bonds prospects are more "attractive" due to the positive holding period yield (US Bond yield > overnight index swap rate) continuing to attract demand.

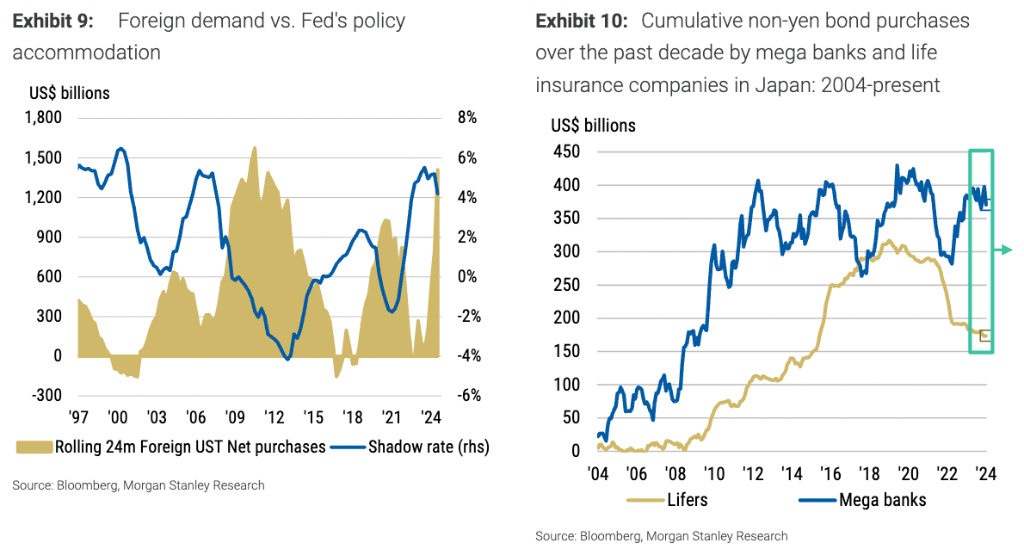

For foreign investors, the focus will shift to the impact of the new government's fiscal policy on negative growth, thus the expectation of interest rate cuts has revived foreign capital's demand for US Bonds.

The report gives an example that Japanese investors have been on the sidelines over the past year, but attractive arbitrage trades and hedging costs will shift investment returns from Japan to non-yen Bonds.

Regarding retirement funds, the report believes that their asset surplus situation is relatively good (the market value of assets exceeds the present value of future liabilities). The fund will rebalance its portfolio and choose a de-risking strategy, shifting from Stocks to long-term Government Bonds, especially in a situation where long-term interest rates remain high while Stocks continue to rise.

The performance of the EUR is outstanding.

The report indicates that although the market holds a pessimistic view on the EUR, the low expectations mean that Europe is more likely to exceed expectations, especially with private consumption driving growth.

Trump's return to the White House has caused concerns about trade policy globally, putting pressure on an already challenging economic outlook for Europe. However, Morgan Stanley believes that despite the generally pessimistic expectations, the European economy may instead deliver surprises.

On the one hand, Morgan Stanley believes that the fundamentals of trade policy may not be as aggressive as many investors fear, particularly regarding policies related to Europe, and that the EUR carries a "considerable" trade-related risk premium.

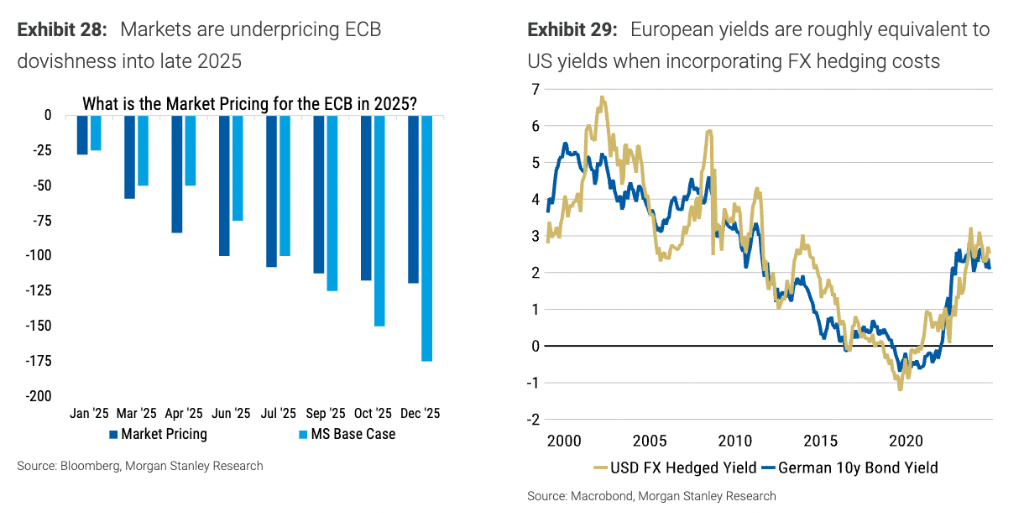

The report adds that the market has underestimated the intensity of the current interest rate cut cycle from the ECB, by about 75 basis points, and it can be anticipated that there is still upward potential for the economy under more significant rate cut stimuli.

Better-than-expected economic growth, unexpected positive political news domestically and internationally, and a lower threshold of expectations may all lead domestic and foreign investors to reallocate capital.

On the other hand, the report considers fund repatriation to be a particularly important potential surprise area. Taking the ten-year Treasury bond as an example, the nominal yield of US Treasury bonds is more than 200 basis points higher than that of German bonds, but once foreign exchange hedging costs are taken into account, this yield advantage disappears.

Although Morgan Stanley expects yields in the USA and Europe to decline, the fact that the US curve is unlikely to experience a meaningful inversion indicates that if Europe's situation begins to show unexpected upward movement, European investors may be willing to deploy more funds in Europe.

The report also states that, although the market generally holds a pessimistic stance on the EUR, $EUR/USD (EURUSD.FX)$It has been trading within a relatively narrow Range, and any significant unexpected bearish sentiment from investors could push the EUR/USD to break through the upper part of the Range.

The Bank of England shortens the interest rate cut cycle, and the yield curve of Japanese bonds flattens...

In addition to the three points above, the report also presents the following possible "surprise" events that may occur in 2025:

The SOFR (Secured Overnight Financing Rate) swap spread curve flattens. The issuance of US Treasury bills falls short of expectations, leading to an expansion of the swap spread. The Federal Reserve may increase purchases of short-term US Treasury bonds to adjust the maturity structure of its balance sheet.

The Bank of England shortens the easing cycle. Persistent inflation limits the Bank of England's ability to cut interest rates further, thus restricting the performance of the UK bond market.

The Japanese Government Bond yield curve is flattening. In the case of a hard landing for the USA economy or if Japanese wage growth does not meet expectations, the Japanese Government Bond yield curve may take on a Bullish flattening, rather than a Bearish flattening.

The yield curve for European bonds for 10-30 years is slowing down. Although the macro background supports a steepening of the yield curve for European bonds, the European Central Bank's interest rate cut actions and slight re-pricing of volatility may pose risks to this position in the first few months of 2025.

The dollar's response to tariffs may not be significant. The dollar is unlikely to be affected by aggressive tariff policies, but a slowdown in the US economy or a more sensitive response from the Federal Reserve compared to other central banks could bring downside risks to the dollar.

US inflation expectations are declining. Although the Trump administration's policies may be seen as boosting inflation prospects, if the damage to demand and the impact of tariffs outweigh initial inflation, inflation expectations may fall.

Emerging Markets local bonds are rebounding. Due to a weakening dollar, local currency bonds in Emerging Markets may perform excellently, especially high real yield bonds from countries like Brazil, Mexico, Indonesia, and South Africa.

Editor/Rocky