在本文中,我们通过数据驱动的视角

在本文中,我们通过数据驱动的视角Author: Tanay Ved Source: Coin Metrics Translation: Shan Ouba, Golden Finance

As 2024 is about to end, it contrasts sharply with the crypto winter of 2022. We want to take a moment to reflect on this remarkable year for the Cryptos Industry.

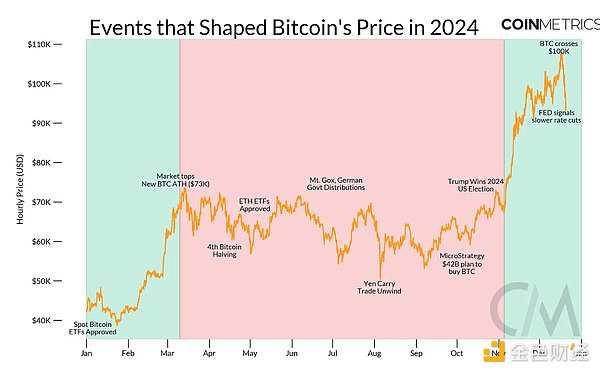

2024 is set to be the most influential year in the history of Cryptos in many aspects, beginning with the launch of the Bitcoin ETF and concluding with Bitcoin surpassing 0.1 million USD after the election.

In this article, major developments shaping the Digital Assets Industry in 2024 are re-examined from a data-driven perspective.

In this article, major developments shaping the Digital Assets Industry in 2024 are re-examined from a data-driven perspective.

Driven by the explosive success of Bitcoin ETF in January, the Crypto market experienced a strong growth phase in the first quarter, with Bitcoin soaring to a historic high of 0.073 million USD. This was followed by a relatively calm consolidation phase characterized by a weakening of catalysts and a significant redistribution of supply among major market participants. Now, as 2024 approaches its end, optimism has returned, buoyed by support for Cryptos from the USA government and the onset of interest rate cuts.

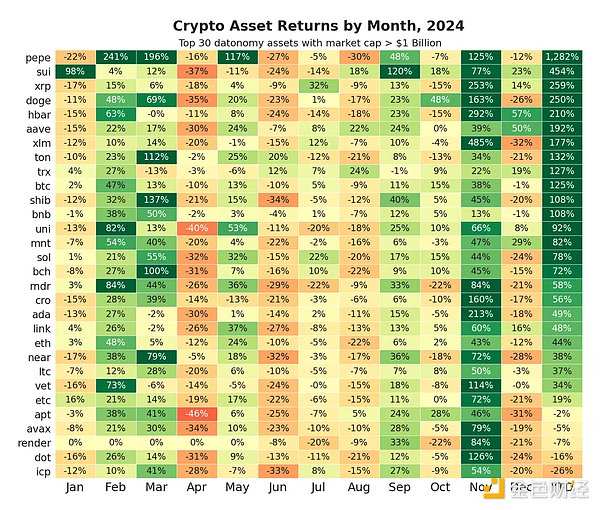

Bitcoin (BTC) is undoubtedly the focus this year, with an increase of 125% year-to-date, outperforming traditional asset classes and Crypto assets. Solana (SOL) has frequently led the market during this cycle, achieving a 78% rise by the end of the year, while Ethereum (ETH) continues to perform poorly, rising only 44% over the year.

The above image shows the top 30 crypto assets in the datonomy TM field, with a market cap exceeding 1 billion USD. Driven by retail enthusiasm, meme coins like DOGE and PEPE have garnered widespread attention, while "dinosaur coins" like Ripple (XRP) and Stellar (XLM) surprisingly made a comeback. Alternative Layer-1s like Sui (SUI) and established blue-chip DeFi protocols like Aave have also gained attention, reflecting investor sentiment and the thematic rotation shaping the market in 2024.

Q1: The ETF floodgates open, Memecoin frenzy, Ethereum expands with Blob.

The emergence of spot Bitcoin ETFs has triggered a wave of widespread adoption, opening the floodgates for Wall Street. The total assets under management (AUM) of 11 issuers currently exceed 105 billion USD, holding over 1.2 million Bitcoins. This accounts for 5.6% of Bitcoin's current supply, with demand from corporate balance sheets further accelerating the pace at which supply is absorbed. In less than a year since its launch, the spot Bitcoin ETF has experienced strong liquidity, solidifying its position as the most successful debut in the history of any ETF category.

Weekly flows show continued accumulation, with net increases exceeding 2 billion USD in peak weeks, despite occasional outflows during the summer market consolidation.

As Bitcoin drives institutional adoption and boosts the overall market, meme coins begin to attract a lot of attention, resulting in a surge driven by extreme risk. At the beginning of March, the spot trading volume of meme coins reached 13 billion USD, with the market cap of major meme coins hitting 60 billion USD.

Although mature large memecoins have seen some growth, most of the activity has come from a large number of newly launched meme coins on Solana. A platform called pump.fun has become the center of explosive growth in memecoins in the first quarter, facilitating the creation of over 75,000 tokens and pushing the number of active wallets on Solana to a record 2.06 million at that time. While these high levels of activity have not been sustainable, memecoins made a comeback with trading volume exceeding 23 billion USD in November. New AI agent platforms like Virtuals on Base have injected new vitality into this phenomenon.

March was also an important milestone for Ethereum, as Ethereum deployed EIP-4844 in the Dencun upgrade. Soon after, Ethereum's second-layer Rollup adopted a new blob transaction fee market concurrently with the mainnet. This laid the foundation for Ethereum to expand its execution range with the help of second layers like Base, Optimism, and Arbitrum, while lowering the settlement costs on the first layer, making transactions on the network more affordable. The demand for blobs has remained strong, with Ethereum hitting the target capacity of 3 blobs per block just seven months after launch.

While this has made the Ethereum ecosystem more accessible, it can be argued that the reduction in Layer 1 fees has hindered the accumulation of ETH value, leading to a more fragmented user experience. However, there are no signs of exhaustion in the sector, with well-known exchanges like Kraken and Uniswap, Deutsche Bank, and multinational corporations (Sony) driving the development of Layer 2, and an increase in blob capacity is also on the horizon.

Q2: Summer Market: Supply Season Begins

The second quarter was characterized by a consolidation phase, with the market experiencing range fluctuations due to a lack of catalysts. In April, Bitcoin underwent its quadrennial halving event, reducing the daily issuance from 900 coins to 450 coins. Like the halving event, this marked a turning point for the mining industry, forcing miners to adapt to the decline in block subsidies. This event triggered upgrades to more efficient ASIC hardware, further consolidation in the mining industry, and prompted some miners to repurpose their infrastructure for AI datacenters to diversify income sources.

As shown in the figure below, trading fees have become a key component of mining revenue, partially offsetting the decline in block subsidies. Despite this, the overall hash price (daily USD income per TH/s) remains under pressure, reflecting that miners are increasingly relying on network activity to maintain sustainability.

Adding to these challenges is additional supply pressure. The most notable is the long-awaited distribution of Mt. Gox bankruptcy assets, with thousands of BTC returning to the market. Similarly, the German government sold over 50,000 BTC seized in criminal investigations, which increased selling pressure and intensified supply dynamics. Despite these sell-offs, Bitcoin's liquidity remains resilient, absorbing the supply without causing significant disruption to market stability. Looking ahead, as FTX creditors are expected to receive cash distributions in 2025 and possibly re-enter the market, selling pressure may ease.

Q3: The Spring of Stablecoins and Tokenization

Stablecoins are recognized as the "killer application of cryptocurrencies," with their global importance beginning to penetrate beyond the cryptocurrency industry. Stablecoins continue to export USD around the world, with total supply exceeding 210 billion USD. USDT (138 billion USD) and USDC (42 billion USD) still dominate, while most stablecoin supply tends to operate on the Ethereum network, which has a supply of 122 billion USD. Overall, stablecoins facilitated a monthly (adjusted) transaction volume of 1.4 trillion USD in November.

While the role of stablecoins as mediums of exchange and store of value in emerging economies has been widely explored, their utility in payment and financial services infrastructure has further accelerated with Stripe's acquisition of Bridge. Furthermore, 99% of stablecoins are pegged to the USD, with Tether and Circle directly investing nearly 100 billion USD in US Treasury bonds, reinforcing their status as essential tools in maintaining the USD's dominance globally.

Meanwhile, Blackrock has entered the tokenization field by launching the Blackrock US Dollar Institutional Digital Liquidity Fund (BUIDL), which invests in cash and US Treasury bills as USD-equivalent assets. The supply of BUIDL rapidly reached 0.5 billion, expanding the landscape of tokenized securities on public blockchains. The ecosystem will expand in 2024, offering stablecoins with different risk profiles, liquidity, collateral, and savings mechanisms. Ethena's USDe stands out, with its market cap growing from 91 million USD to 6 billion USD, becoming the third-largest stablecoin, offering attractive returns to holders by utilizing positive financing rates during market uptrends. Meanwhile, First Digital USD (FDUSD) has gained fame as a source of liquidity and a widely used quote currency on exchanges.

Regulatory attention to stablecoins is increasing, reflecting the growing importance of stablecoins in the global financial system. The EU has implemented specific requirements for stablecoins under the Markets in Crypto-Assets (MiCA) regulation, which has begun to reshape the stablecoin industry pegged to the euro.

Q4: Election Frenzy

The 2024 USA presidential election has had a profound impact on the digital asset market, pushing Bitcoin to surpass 0.1 million USD for the first time. In the Coin Metrics datonomy TM field, dedicated coins (including meme and privacy coins) and Asia Vets platforms have shown outstanding performance, with returns of 129% and 84% respectively since the election.

On the eve of the election, we also witnessed the rise of prediction markets like Polymarket, which played a key role in gathering collective intelligence on election results. At its peak, Polymarket's open contracts were valued at over 0.45 billion USD. Although activity on the platform has now quieted, it demonstrates the utility and potential of information markets on public blockchains.

Post-election, market optimism is high, thanks to government support for Cryptos, which is in stark contrast to the previous regulatory resistance from the SEC. The demand for ETFs and corporate Bonds has driven the rise of Bitcoin, with MicroStrategy's holdings reaching 444,262 BTC, funded by its Stocks and convertible bond issuance. Institutional interest in the derivatives market has reached new highs, reflected in CME's Bitcoin Futures open contracts setting a record of 22.7 billion USD, while total contracts exceed 52 billion USD, and Options-type ETFs have also been launched successively.

Despite the strong momentum, the implementation and timeline of Crypto-friendly policies remain uncertain. While there are clear signs that the regulatory environment will be more supportive of Cryptos, including the appointment of advocates for Cryptos to key positions like the SEC Chair and Crypto Czar, the specific regulatory framework is still unclear. Market enthusiasm is also tempered by expectations of interest rate cuts, with participants taking a cautiously optimistic view towards 2025.

Nonetheless, 2024 leaves us with a solid foundation: the launch of spot Bitcoin ETFs, accelerated adoption of stablecoins, significant improvements in on-chain infrastructure and applications, and a pro-Crypto government beginning its term amid a rate-cutting cycle. As we enter the next year, please stay tuned for our 2025 Crypto Outlook report, where we will explore the key themes and trends that will affect the coming year.