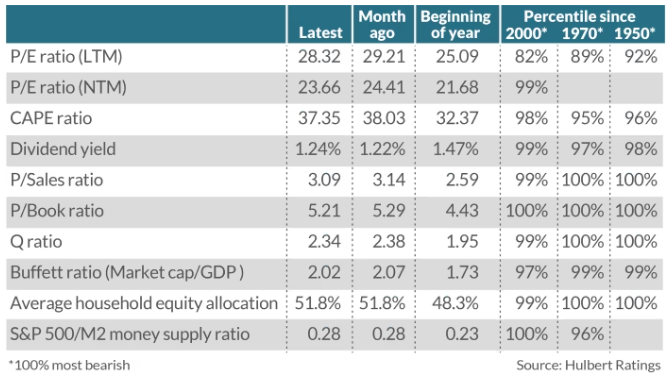

下表中列出了一些在美股预测方面有一定战绩的估值指标,它们能够预测股市的10年预期回报,而且在预测4年回报方面也有可观的记录。平均而言,这些指标显示,

下表中列出了一些在美股预测方面有一定战绩的估值指标,它们能够预测股市的10年预期回报,而且在预测4年回报方面也有可观的记录。平均而言,这些指标显示,Various market indicators indicate that the U.S. stock market will face difficulties during President Trump's term, with the potential for a negative real annual ROI over the next four years.

The newly elected president of the USA, Trump, may face a stock market that is overestimated more than on any other inauguration day in American history on his first day in office.

Trump is known for viewing the stock market as a barometer of his success; therefore, if the market's performance over the next four years is only in line with historical averages, then there is a lot of work to be done.

The following table lists some valuation indicators that have a good track record in predicting the US stock market, capable of forecasting the 10-year expected returns, and they also have a considerable record in predicting 4-year returns. On average, these indicators show that from now until the inauguration day in January 2029, the return on the US stocks may barely keep up with inflation.

The following table lists some valuation indicators that have a good track record in predicting the US stock market, capable of forecasting the 10-year expected returns, and they also have a considerable record in predicting 4-year returns. On average, these indicators show that from now until the inauguration day in January 2029, the return on the US stocks may barely keep up with inflation.

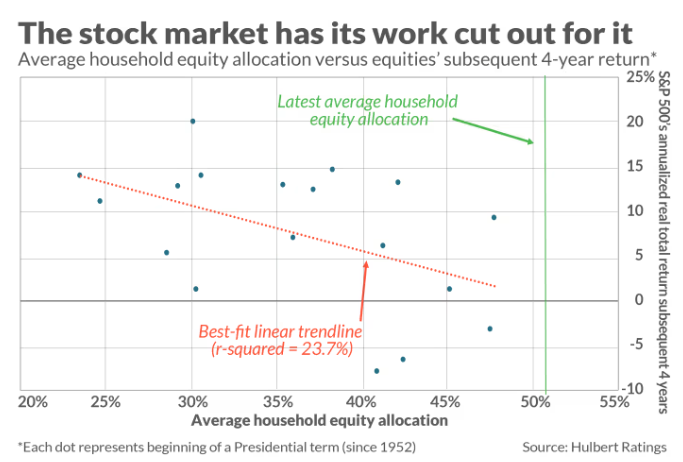

Among the indicators in the table, the one with the most significant predictive capability for the four-year return is the stock allocation of the average American household.

The following graph indicates the position of this indicator on each presidential inauguration day since 1952, as well as the inflation-adjusted total return of the stock market over the subsequent four years. The downward sloping red line indicates that a higher average household stock allocation is associated with lower subsequent four-year stock market returns.

The vertical green line in the chart represents the current level of average household Stocks allocation—51.8%, compared to 48.3% at the beginning of 2024. The inference from the trendlines in the chart indicates that the actual annualized ROI of US Stocks over the next four years is -1.5%.

However, as shown in the figure, despite the data showing a significant downward trend statistically, there is still a lot of noise. The last time household Stock allocation reached a historical high on the day of the presidential inauguration was in 2020, but since then, the inflation-adjusted annualized total return of the S&P 500 Index has reached 9.3%, higher than the average actual return of 7.2% since 1952.

Even so, it can be fairly said that the valuation trends over the next four years will not favor Stocks. The first table has shown the position of valuation Indicators now relative to their distribution in three different historical periods, namely since 2000, 1970, and 1950. A reading of 100% is the most Put, and almost all readings are above 90%, with many at 100%.