在这段时间里,美联储已经累计降息了100个基点——9月降息50个基点、11月和12月各降息25个基点;

在这段时间里,美联储已经累计降息了100个基点——9月降息50个基点、11月和12月各降息25个基点;As the USA stock and bond markets officially enter the Christmas holiday this Wednesday, the US bond market is actually experiencing the overlap of three '100's:

According to the financial link on December 25 (editor: Xiaoxiang), as the USA stock and bond markets officially enter the Christmas holiday this Wednesday, the US bond market is actually experiencing the overlap of three '100's:

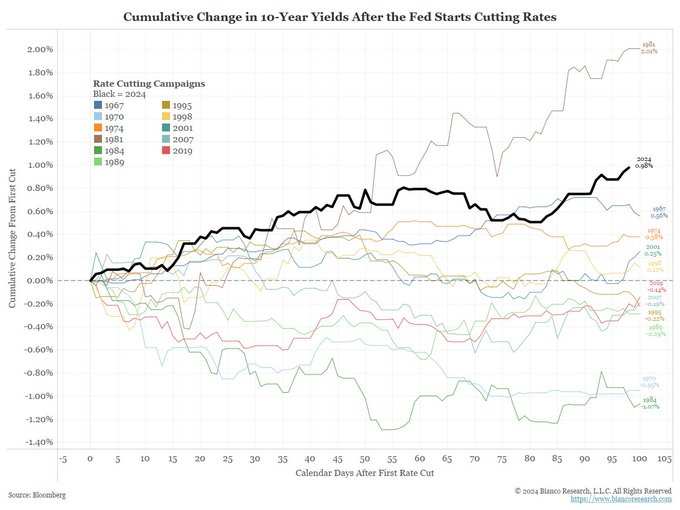

Counting the days, nearly 100 days have passed since the Federal Reserve officially started this round of rate cuts on September 18...

During this time, the Federal Reserve has cumulatively cut rates by 100 basis points - 50 basis points in September, and 25 basis points in both November and December;

While during these 100 days and 100 basis points of rate cuts, the US bond market's trend during this period has actually been like a 'rate hike' of 100 basis points - with the 10-year US bond yield breaching the 4.60 mark on Tuesday, this 'anchor for global asset pricing' has seen an increase of nearly 100 basis points since the Federal Reserve's September meeting.

This kind of scenario, although investors may not feel anything unusual during daily trading - in the context of Trump soon returning to power in less than a month, and the Federal Reserve 'indicating' it will slow its rate-cutting pace next year, the rise in US bond yields, especially long-term bond yields, is not surprising. But when industry insiders review the market during this Christmas holiday, they may still be shocked.

In fact, such a trend is extremely rare; in the past forty-plus rate-cutting cycles, the scenario where the benchmark 10-year US bond yield skyrocketed so much after a Federal Reserve rate cut has only been more exaggerated once, which is an episode that all Wall Street people do not wish to recall - the year 1980.

The broader context of the American economy around 1980 can actually be summed up in two words: stagflation.

This originated from the economic recession and inflation out of control that the USA experienced after the outbreak of the second oil crisis. Against this background, then Federal Reserve Chairman Volcker briefly lowered interest rates in 1980, but this monetary easing action was quickly overturned within just a few months.

According to the NBER definition, the USA entered a recession in the first quarter of 1980. The federal funds rate dropped from nearly 20% in March 1980 to 10% in July. Surprisingly, the economy showed a strong recovery afterward. In October of that year, the Iran-Iraq War broke out, global oil prices surged, and inflation risks returned. Due to the strong rebound in economic activity, coupled with the threat posed by rising oil prices, the Federal Reserve quickly initiated a new round of tightening, raising the federal funds rate from 13% in October of that year back up to 20% in December.

Interestingly, after the Federal Reserve lowered interest rates at that time, investors represented by U.S. Treasury bond traders almost did not believe that the rate cut could be sustained— the yield on 10-year U.S. Treasuries rose by about 200 basis points within 100 days after the Fed's first rate cut. In fact, the more the Federal Reserve shouted about the rate cut, the more tense the bond market became, leading investors to sell off bonds to prevent a severe inflation scenario.

Such a scenario, although not entirely applicable to the current U.S. Treasury market's situation, does share several similarities.

For example, the concerns regarding inflation are actually consistent. Market participants expect that with the election of President Trump and his plans to cut taxes and impose tariffs on a range of imported products, inflation in the USA will accelerate once again. These measures may expand the fiscal deficit, putting pressure on the long end of the yield curve, and pushing up long-term bond yields.

Some industry insiders are even starting to predict that the Federal Reserve will "return to the path of rate hikes". For example, Apollo Global Management's chief economist, Torsten Slok, recently warned that the Federal Reserve may have to return to raising rates in 2025, as the U.S. economy remains strong and the policies planned by President-elect Trump could elevate inflation.

Perhaps Powell may find that after leading the Federal Reserve's most aggressive tightening actions in 40 years, he also needs to revisit the "textbook" that documents the history from over 40 years ago on how to conclude this tightening cycle.

Editor/ping