行情数据数据,截至纽约时段尾盘,2年期美债收益率上涨3个基点报4.351%,5年期美债收益率涨5.5个基点报4.44%,10年期美债收益率涨6.5个基点报4.592%,30年期美债收益率涨5.8个基点报4.78%。

行情数据数据,截至纽约时段尾盘,2年期美债收益率上涨3个基点报4.351%,5年期美债收益率涨5.5个基点报4.44%,10年期美债收益率涨6.5个基点报4.592%,30年期美债收益率涨5.8个基点报4.78%。For Wall Street traders, the USA market trading this week will be split into two segments due to the arrival of the Christmas holiday; however, at least in the first half during less than two complete trading days, US bond bulls still seem to see no signs of relief in selling pressure.

According to a report from the Financial Association on December 24 (editor: Xiaoxiang), for Wall Street traders, the USA market trading this week will be split into two segments due to the arrival of the Christmas holiday. However, at least in this first half during less than two complete trading days, US bond bulls still seem to see no signs of relief in selling pressure.

The yields on US bonds of various maturities rose again on Monday, particularly the selling pressure on long bonds was notably evident — the yield on the 10-year US Treasury bond further reached a nearly seven-month high. The increase in the yields of long-term government bonds significantly outpaced that of short-term government bonds, highlighting the steepening trend of the yield curve in recent weeks.

According to market data, as of the end of the New York session, the yield on the 2-year US Treasury bond rose by 3 basis points to 4.351%, the 5-year yield increased by 5.5 basis points to 4.44%, the 10-year yield rose by 6.5 basis points to 4.592%, and the 30-year yield increased by 5.8 basis points to 4.78%.

According to market data, as of the end of the New York session, the yield on the 2-year US Treasury bond rose by 3 basis points to 4.351%, the 5-year yield increased by 5.5 basis points to 4.44%, the 10-year yield rose by 6.5 basis points to 4.592%, and the 30-year yield increased by 5.8 basis points to 4.78%.

The spread between the yield on the 10-year Treasury bond and the 2-year Treasury bond has currently reached around 25 basis points, far higher than the near-flat levels at the beginning of this month. In fact, just in late June of this year, the yield on the 2-year bond was once 51 basis points higher than that of the 10-year bond, indicating an extreme yield curve inversion.

Andrew Brenner, head of international fixed income at CSI All Share Investment Banking &, stated, "Long-term bonds have been under pressure lately, as investors raised the risk premium they see in bonds. Fiscal conditions are also a factor for the increase in long-term risk premiums, as debt issuance may further increase. Overall, what we are seeing is a normalization of the yield curve."

In recent months, the phenomenon of US bond yields, particularly long bond yields, rising unusually during the Federal Reserve's rate-cutting cycle has attracted increasing attention from market participants. Long bonds are under pressure mainly because traders believe that the pace of rate cuts by the Federal Reserve will slow next year and that the fiscal backdrop of the USA may worsen under President Trump's leadership.

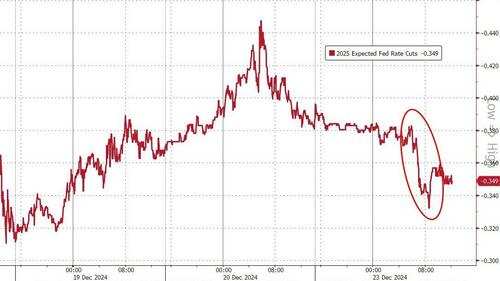

Interest rate swap contracts show that traders' latest bets on rate cuts next year are currently further below the 50 basis points projected by Federal Reserve officials in the dot plot. By the end of 2025, the rate cuts priced in by interest rate contracts are only 34 basis points — closer to just one rate cut.

This also means that despite the US Consumer Confidence report released on Monday being weaker than expected and strong demand for the two-year Bonds auction, US Bonds overall still face selling pressure.

LPL Financial's Chief Economist Jeffrey Roach and Chief Fixed Income Strategist Lawrence Gillum stated in a report on Monday that the biggest surprise in last week's Federal Reserve decision was actually the upward revision of next year's inflation forecast. Federal Reserve officials expect that by the end of 2025, the inflation rate will reach 2.5%, higher than the 2.1% predicted in September, which likely reflects the uncertainty brought about by a potential trade war.

Stifel Nicolaus & Co. strategist Chris Ahrens noted that although the dot plot indicates that the Federal Reserve may slow its easing pace during 2025, the yield curve for the two-year and ten-year Bonds has not re-flattened. This may signal a shift occurring, where fiscal concerns and overall policy uncertainty will lead investors to demand a higher term premium for long-term Bonds.

From the news perspective, it may be influenced by the Christmas holiday, and there will be no Federal Reserve officials speaking for the remainder of this week – which is different from the past when officials liked to make intensive appearances in the week following interest rate decisions. Additionally, there is a lack of important data releases before the Christmas holiday, which may prolong the current pressure on the Bond market. In fact, trading on Monday appeared somewhat subdued, with many traders having already left early ahead of the Christmas holiday.

Before the official start of the Christmas holiday on Wednesday, the trading hours for US Bonds and Stocks on Tuesday will have actually been shortened.

The US stock market will close early at 1 PM New York time on Tuesday (2 AM Beijing time on Wednesday), and Bond market trading will also conclude an hour later. Both markets will not resume trading until Thursday, when the focus will shift to the release of more US economic data, such as initial jobless claims.

Editor/ping