不过, 美联储在本月的会议上暗示明年将减少降息次数,这可能会使收益率走势变得复杂。

不过, 美联储在本月的会议上暗示明年将减少降息次数,这可能会使收益率走势变得复杂。Wall Street listens to the information from the Federal Reserve. They predict that even if Trump's trade and tax policies pose risks to the bond market, short-term US Treasury yields will still decline by 2025.

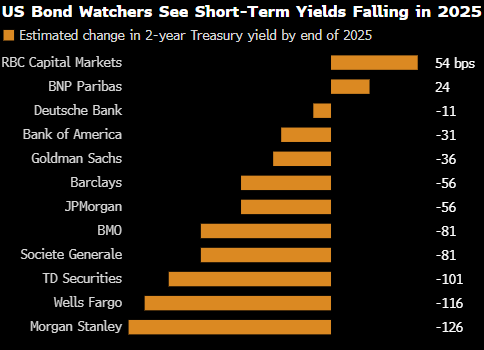

The forecasts from strategists are largely consistent, indicating that the yields on 2-year Treasury bonds, which are more sensitive to Federal Reserve interest rate policies, will decrease. They also expect that the yields will decline by at least 0.5 percentage points from current levels in 12 months.

David Kelly and others from the Morgan Asset Management team stated: "Although investors may be shortsightedly focused on the speed and magnitude of rate cuts next year, they should also take a step back and think about the fact that the Federal Reserve is still on a rate-cutting trajectory in 2025."

However, the Federal Reserve hinted at this month's meeting that it will reduce the number of interest rate cuts next year, which may complicate the trend of yields.

However, the Federal Reserve hinted at this month's meeting that it will reduce the number of interest rate cuts next year, which may complicate the trend of yields.

The median forecast in the Federal Reserve officials' dot plot is that rates will only be reduced by half a percentage point in 2025, which is roughly equivalent to the expected decline in the two-year Treasury yield by Wall Street, but there is a risk that the central bank will pause its easing cycle. After Powell linked the prospect of further rate cuts to inflation, the U.S. Treasury yield curve reached its steepest level since June 2022 on Thursday.

Tracey Manzi, a senior investment strategist at Raymond James, stated that as the pace of rate cuts slows, short-term yields should also follow this trend, and if the yield curve steepens, it is mainly due to the decline in long-term bonds.

The median forecast of 12 strategists is that the two-year Treasury yield will decrease by about 50 basis points to 3.75% in a year. Since the Federal Reserve released its latest economic forecast on Wednesday, this yield has risen by nearly 10 basis points.

For the longer-term 10-year US Treasury bonds, the strategist expects the yield to be around 4.52% on Friday, reaching 4.25% by the end of 2025, which is about 25 basis points lower than the current level.

State Street macro strategist Noel Dixon predicts that regardless of whether it’s the actual growth rate, inflation expectations, or term premium, long-term bonds will always be under pressure. The strategist previously forecasted that the 10-year yield could rise above 5% next year.

They are not only thinking about how fiscal policy may evolve but also considering the Federal Reserve's management of the US Treasury holdings. The end of the central bank's balance sheet reduction may decrease bond supply and thus stimulate demand for purchasing bonds.

Anshul Pradhan and other Barclays strategists wrote in a report, "Even if the Federal Reserve may continue to lower the policy interest rate, bringing down short-term yields, many factors supporting long-term yields to remain high still exist: such as a high neutral rate, increased interest rate volatility, inflation risk premium, and large net issuance in price-sensitive demand."

Bloomberg strategist's view

"Stable economic performance early in 2025 may lead to gradual rate cuts by the Federal Reserve, with rates possibly peaking at 4%. The 10-year yield may only deviate from 3.8%-4.7% in the case of a significant shift in the economy."

---Ira F. Jersey, Will Hoffman

The upcoming Trump tariffs and tax policies in the next few weeks may disrupt Wall Street's outlook.

Pradhan stated: "Higher tariffs and stricter immigration controls will lead to slower growth but rising inflation."

Morgan Stanley and Deutsche Bank hold the most optimistic and pessimistic views on the Bonds market, respectively. Morgan Stanley believes that investors face "downside risks to economic growth" and "unexpected bull markets." The bank expects the Federal Reserve to cut rates faster than other banks and predicts that the 10-year yield will fall to 3.55% by December next year.

Deutsche Bank predicts that the Federal Reserve will not cut rates in 2025, and Matthew Raskin's team forecasts that under strong economic growth, low unemployment, and sticky inflation, the 10-year yield is expected to rise to 4.65%.

They wrote in a report: "The main catalysts supporting our view are our realization that inflation and labor market conditions require a more restrictive Federal Reserve interest rate path than currently priced in."