Witness history.

Author | Godzilla

Data Support | Pythagoras Big Data ()

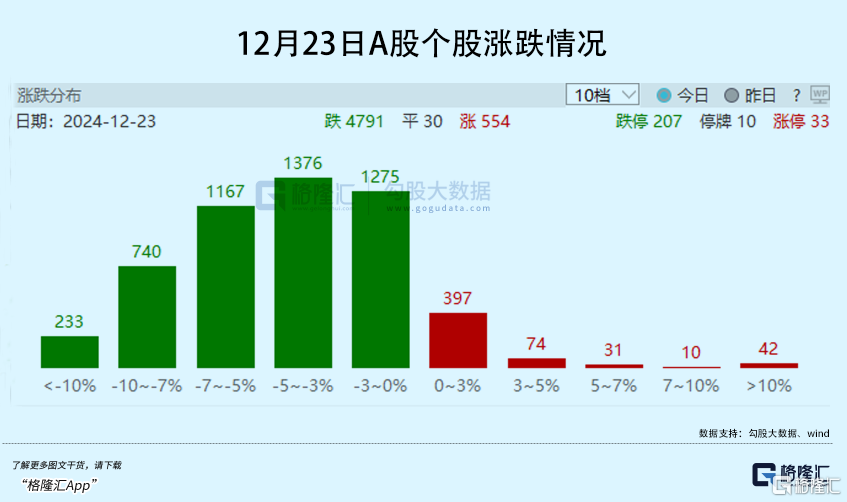

Today, the A-share market witnessed history again!

On one side, the four major banks all hit historical highs, with Industrial And Commercial Bank Of China, Agricultural Bank Of China, Postal Savings Bank, and China Merchants Bank all surging over 2%, driving a strong rise in the financial sector.

On the other side, the market overall fell, with the Shanghai and Shenzhen indices dropping by 0.5% and 1%, respectively. There were 4,791 stocks declining in the entire market, with over 200 stocks falling more than 10%. The median drop was around 5%, with some micro-cap indices even dropping over 7%.

Such drastic differentiation feels a bit unreal.

But if this differentiation continues for a while, would it be believable?

01

From the perspective of many people, the current Banking Sector has numerous issues that are not very appealing.

According to theory, against the backdrop of the current macroeconomic situation and interest rate trends, the risks in Banking Business Operations may rise, such as the contraction of net interest margins, potential increase in loan delinquency rates, reduction in profitability from intermediary businesses, and even risks of impairment in some equity investments (such as real estate projects), among others.

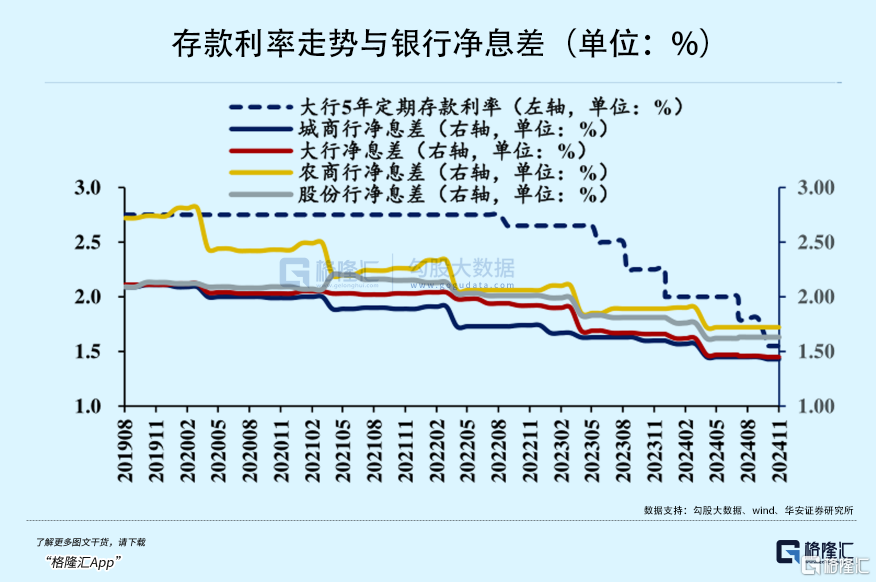

The real data from the banking industry also reflects this, such as the net interest margin of large banks and city commercial banks, which indicates that it has dropped below 1.5% overall in November.

At the same time, as a banking industry under the socialist system, it may face demands to benefit the public in the context of a weakening economy (in reality, many concessions have indeed been made in various areas), which could negatively impact bank profits.

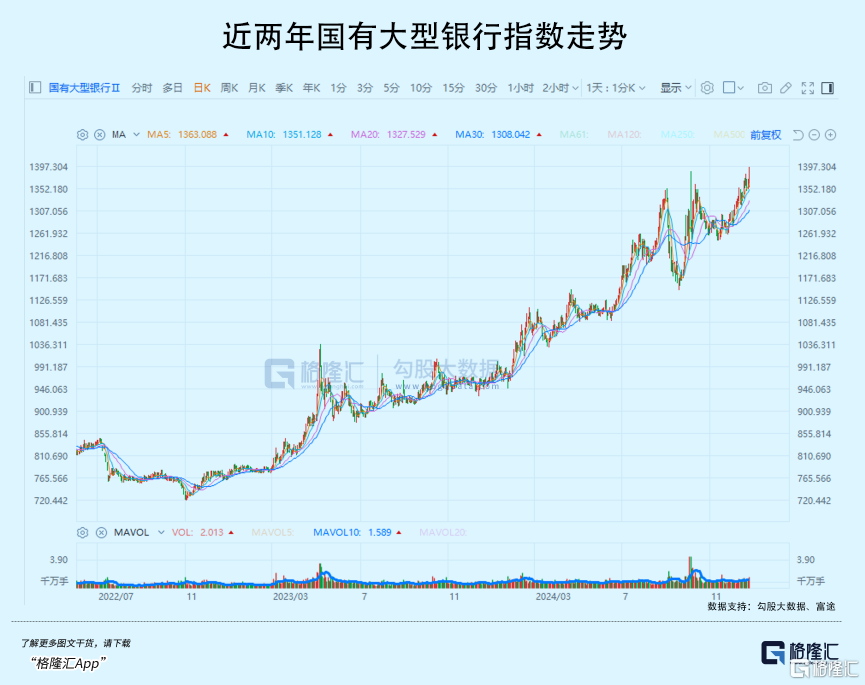

Additionally, over the past two years, the Banking Sector has been continuously rising. Just this year, large state-owned banks, joint-stock banks, city commercial banks, and agricultural commercial banks have surged by 43.8%, 38.43%, 40.81%, and 40.22% respectively, with the large state-owned banks experiencing the most significant increase. If calculated from 2023, the rise is even close to 80%, which is astonishing compared to the Shanghai Composite Index's mere 8.5% increase over the past two years.

In this context, the valuation attractiveness of banks seems to be less appealing than before.

However, the actual situation of domestic banks presents a different picture.

From the data, while large state-owned banks’ stock prices have rarely soared in the past two years, they still remain the lowest PE/PB rare assets in the All Market.

From the beginning of 2023 to now, the overall PE of large state-owned banks has risen from only 4 times to 6.3 times; the overall PB has increased from 0.4 times to 0.56 times. Their overall latest dividend yield is generally still around 4.5%, significantly outperforming 99% of other industries in the A-shares market.

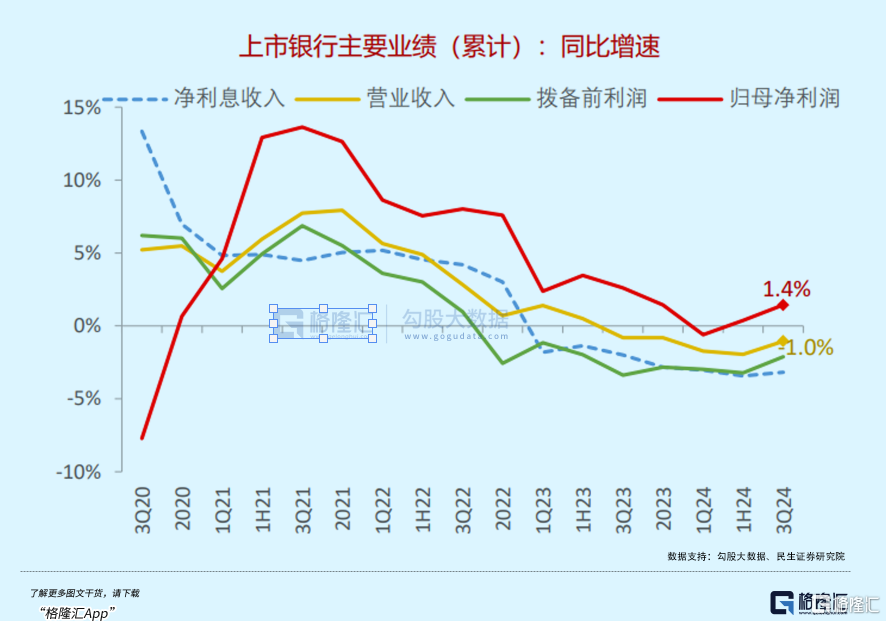

The reason for this is that large banks are still very profitable, in the first three quarters of 2024:

The net income attributable to the parent company of Industrial And Commercial Bank Of China is 269.025 billion yuan, a year-on-year increase of 0.13%;

The net income attributable to the parent company of Agricultural Bank Of China is 214.372 billion yuan, a year-on-year increase of 3.38%;

The Net income attributable to the parent company of Bank Of China is 175.763 billion yuan, an increase of 0.52% year-on-year;

The China Construction Bank Corporation reported a net income of 255.776 billion yuan, with a year-on-year increase of 0.13%.

Although profit growth is not high, stability in growth is valuable and is also improving. According to data from brokerages, the net income attributable to the parent company of listed banks has rebounded in the latest two quarters.

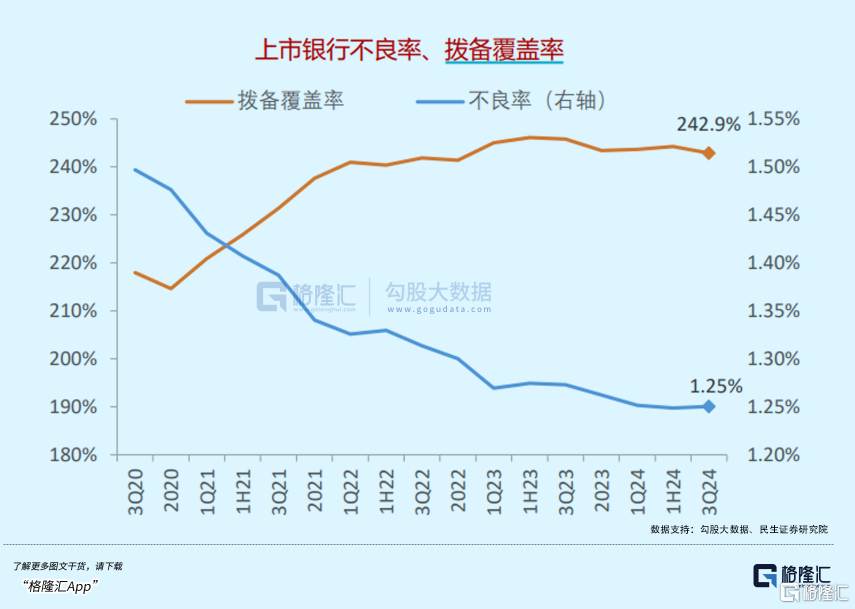

Among these, there is indeed a portion due to a decrease in the provision coverage ratio compared to the previous period; however, this indicator itself has been at a high level for the past two years (Q3 was 242.9%), and there is potential for further reduction, which means it will help improve profitability going forward.

Although domestic interest rate expectations continue to decline and the banks' Net interest margins are also narrowing, banks have their countermeasures, and the policies from regulatory authorities have been very supportive.

For example, regarding the protection of 'Net interest margin', on September 24, at the press conference of the State Council Information Office, it was clearly stated to 'guide Financial Institutions to optimize their layout, hone their internal skills, and actively respond to the risks of narrowing net interest margins and interest spread losses.' Such instructions have appeared multiple times.

In terms of measures, this year the regulatory authorities have continuously proposed strategies to help banks replenish their core Tier 1 capital, including reserve requirement cuts, capital increases, and share expansions, to support banks in better managing debt and expanding businesses. Additionally, banks have adjusted their business structures, particularly increasing their financial market operations, effectively boosting non-interest income.

In the first three quarters of 2024, the investment income of 42 A-share listed banks increased by 23.89% year-on-year, and financial investments accounted for 27.8% of revenue contribution, which improved by 2.3 percentage points compared to 2023.

Among them, trading Bonds provided a noticeable incremental contribution.

On another note, regarding banks' asset quality issues, many are concerned that the current macroeconomic environment will accelerate the deterioration indicators of banks, but in reality, for the past few quarters, the non-performing loan ratios of listed banks have remained very stable with almost no fluctuations.

Although the non-performing loan generation rates of city commercial banks and rural commercial banks have shown slight upward trends, after state-owned banks and joint-stock banks write off and transfer out loan impairment provisions, the non-performing generation rate indicators have overall declined (with a significant decline in corporate non-performing rates).

This may also be one reason why state-owned banks perform relatively better in the market.

02

The regulatory authorities' policy guidelines for market value management and dividend management of state-owned enterprises that are below net asset value are also an important reason for the market's enthusiastic pursuit of Banks.

Last week, the State-owned Assets Supervision and Administration Commission of the State Council issued several opinions on improving and strengthening the market value management of central enterprises' listed companies, stating that central enterprises should improve and strengthen the market value management of their controlling listed companies in six major aspects: mergers and acquisitions, market-oriented reforms, information disclosure, investor relations management, investor returns, and share buyback.

As mentioned above, the PE of large state-owned banks is still at a relatively low level, and the PB is in a deep state of being below net asset value, which is definitely a key "guidance target" for the regulatory authorities.

What is more directly impactful?

After significant rises, several major state-owned banks in the A-share market still have a dividend yield of about 4.5%, which is much more stable and higher than the vast majority of industries in the market. From the perspective of stability and dividend return, they can be regarded as a very high-quality long-term bond similar to long-term government bonds.

However, what many may overlook is that the major state-owned banks not only made super profits in the past but also had very considerable dividends, but in reality, their dividend payout ratio has long only maintained at around 30%.

Now, the regulatory authorities have clearly called for an increase in dividend returns. If these Banks' dividend rates are raised from 30% to 40%, 50%, or even higher, what will this mean? (In comparison, Kweichow Moutai has clearly increased its dividend rate from 50% to over 75%).

The dividend yield can significantly increase by several percentage points!

This approach is far more effective than generating profits through business growth, and it can be changed at any time as long as regulators allow it.

This also brings very positive confidence for the market to continue being bullish on large Banks.

Therefore, the day after the release of the "Opinion", sectors led by state-owned enterprises, such as "Central Valuation" and "CSI Central State-owned Enterprises Dividend Index", opened with significant gains, followed by continuous rises in the Banking sector, all of which are based on logical reasoning.

In addition, we must not overlook an important underlying trend since the beginning of this year: the state is vigorously guiding various long-term funds to invest in the stock market, along with a series of measures.

These include easing restrictions on equity investments, supporting the issuance of index funds, and even providing financial support, among other policies.

These measures are clearly aimed at boosting the stock market.

Currently, the investment limits for equity investments by Banks, Insurance, Funds, and other Institutions have been significantly expanded, and Funds are also issuing a large number of new broad-based Funds. Especially the Funds, since September alone, the net asset value scale of A-share ETFs has skyrocketed from 2.76 trillion yuan in August to the latest 3.78 trillion yuan, with an increase of over 1 trillion yuan.

This massive incremental capital is flowing into the stock market or waiting for better entry opportunities, and a significant portion is bound to flow into 'bond-like assets' such as large Banks that offer high security, stable growth, and high dividend returns.

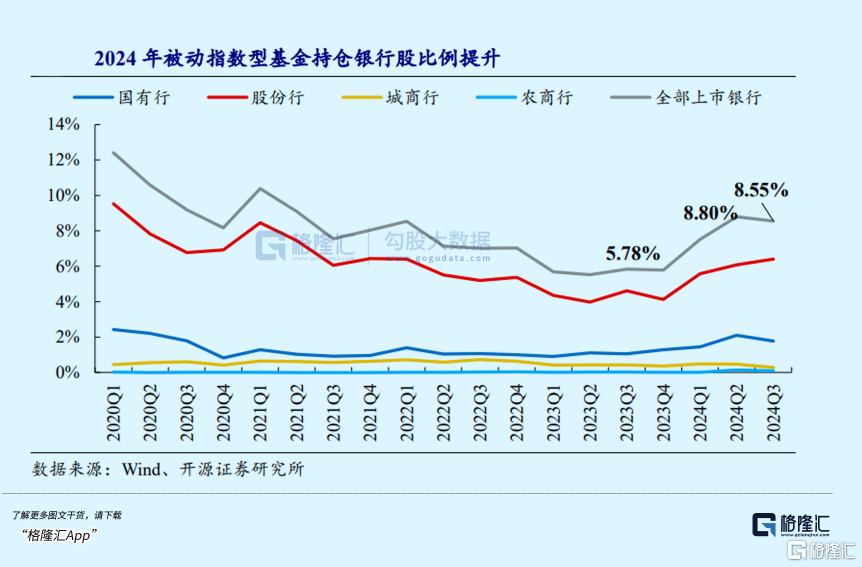

Data shows that this year, the proportion of passive index-type actively held bank stocks is indeed increasing, rising from 5.78% in Q3 2023 to 8.55%, but there is still considerable room for improvement compared to over ten percentage points a few years ago.

In other words, for the major Banks, performance is sufficiently supported, policies have enough protection, dividend return expectations are quite attractive, and they are also supported by massive incremental capital. With so many bullish buffs adding up, it's not surprising that their stock prices are reaching new highs and continue to rise.

03

Epilogue

Since the beginning of this year, major Financial Institutions, including Banks, have been actively trading government bonds, driven merely by risk aversion in the context of an asset shortage, while also earning stable returns.

However, with the 10-year Treasury yield reached, and the 30-year ultra-long Treasury yield reached, coupled with the recent constant warnings from the central bank about the overheating of the bond market, the path of pooling funds to aggressively exploit long bonds seems to have reached its limit.

High-quality large bank stocks also represent a second option aside from long bonds.

Even sectors such as Energy, Utilities, and some high-dividend core leaders from the manufacturing industry will enjoy this dividend. The future trend of these sectors is likely to rise easily while experiencing difficulty in decline, until their normal dividend yield no longer has significant cost-effectiveness.

Within this, there are still many long-term opportunities. For those investors who are both eager to play and inexperienced, rather than making random operations, it would be better to focus on these high-quality, high-dividend large blue-chip stocks, make fewer trades, minimize losses, and even make profits. (The end of the article)