周四和周五早些时候,全球股市也出现类似跌势,直到美国个人消费支出(PCE)数据提供了一些喘息之机。虽然PCE依然强劲,但涨幅低于预期,这有助于减轻美国股市的一些抛售压力。

周四和周五早些时候,全球股市也出现类似跌势,直到美国个人消费支出(PCE)数据提供了一些喘息之机。虽然PCE依然强劲,但涨幅低于预期,这有助于减轻美国股市的一些抛售压力。The Federal Reserve's "shock" to the market, does the bullish sentiment for Gold still need to cool down? The dominance of the dollar is likely to remain unshaken, beware of liquidity shortages amplifying market volatility! Is the recent slump in US stocks a "reverse pick-up"?

This week, the Federal Reserve finally confirmed the long-anticipated "shift" by the market, and the central bank's statement and updates on economic predictions had a massive impact on the market. Market participants currently expect the Federal Reserve to cut interest rates by about 40 basis points by December 2025, and U.S. Treasury yields responded accordingly.

This impact affected various markets, with the U.S. stock market experiencing its worst day since August. The Volatility Index (VIX) saw the second-largest single-day jump in history as the market attempted to digest the Fed's outlook.

On Thursday and early Friday, global stock markets also experienced a similar downturn until the U.S. Personal Consumption Expenditures (PCE) data provided some respite. Although PCE remained strong, the increase was below expectations, which helped ease some of the selling pressure in the U.S. stock market.

On Thursday and early Friday, global stock markets also experienced a similar downturn until the U.S. Personal Consumption Expenditures (PCE) data provided some respite. Although PCE remained strong, the increase was below expectations, which helped ease some of the selling pressure in the U.S. stock market.

The Forex market also exhibited a similar trend, with the dollar generally strengthening and at one point breaking past the 108 level. Gold prices briefly fell below $2600 per ounce but rebounded above that level on Friday.

The Crude Oil Product market continues to feel the pressure of concerns over demand growth, especially with the emergence of expectations for interest rate cuts in 2025, leading to more worries about the continued impact on future demand.

In Asia, the Bank of Japan maintained interest rates, as the improvement in Japanese economic data was not sufficient to convince the Bank of Japan, but the possibility of raising rates in early 2025 is high.

However, as the yen continues to weaken, this may also affect when the Bank of Japan decides to raise interest rates. The central bank stated that interest rate decisions will not be based on exchange rates, but if anything becomes clear, it is that the Bank of Japan's words and actions often do not align.

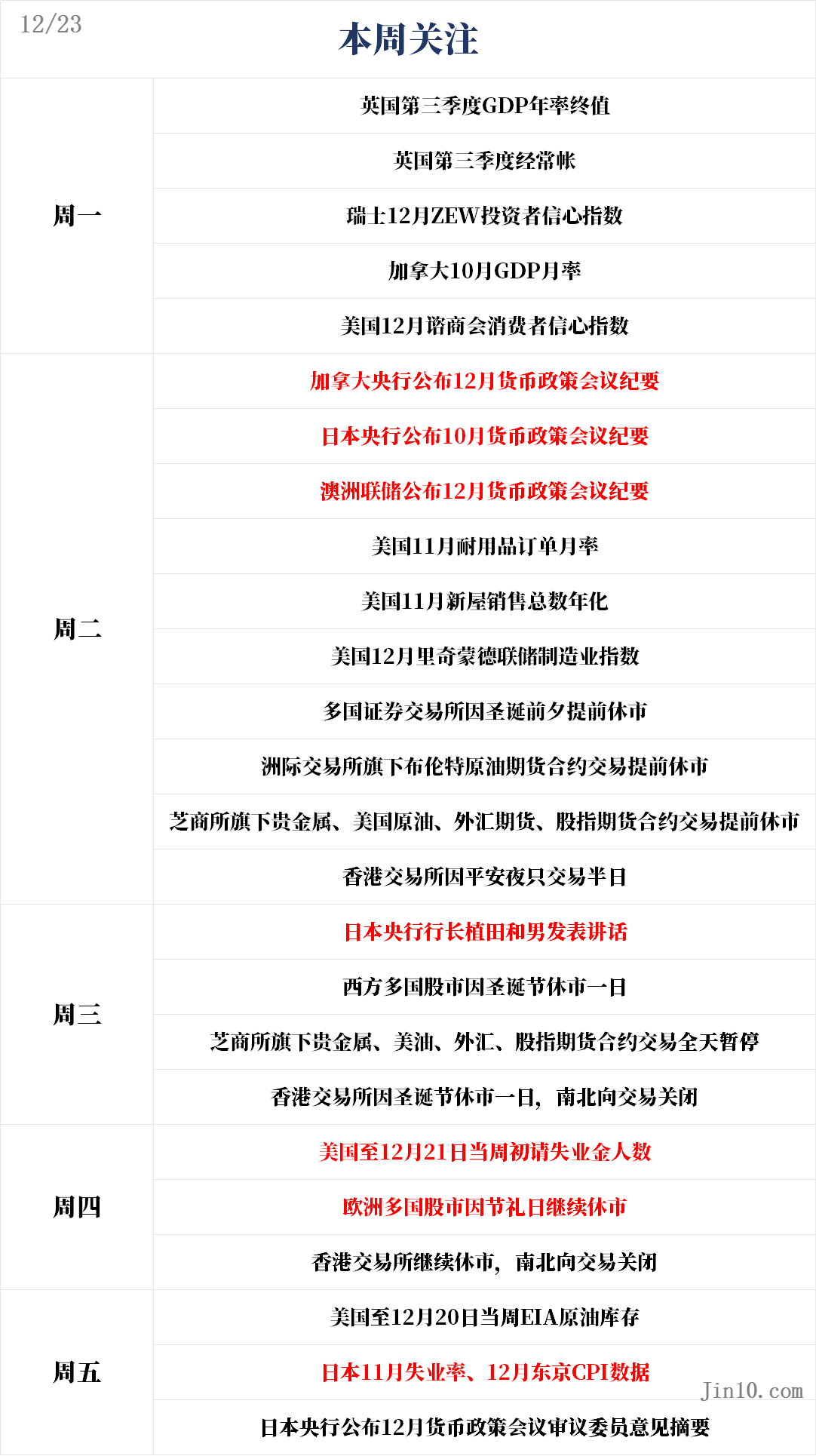

Due to the approach of Christmas, the market will be relatively calm next week, although there will still be some relatively influential data. However, due to thin liquidity, market volatility may become significant. Below are the key points the market will focus on in the new week (all in Beijing time):

Central Bank Dynamics: The Federal Reserve ‘crushes’ the market, and the bullish sentiment in Gold may need to cool down.

Due to the Christmas holiday, there will be no speeches from Federal Reserve officials next week.

The Federal Reserve has just concluded its last policy decision for 2024, and market optimism is lacking. Officials predict only two rate cuts in 2025, each by 25 basis points, leading market participants to expect lower rate cuts in the next 12 months than any other major central bank, except the Bank of Japan, which is raising rates.

Although this was not entirely unexpected, especially after Trump unexpectedly achieved a landslide victory in the U.S. presidential election, the Federal Reserve's hawkish stance still caught the market off guard. Federal Reserve Chairman Powell strongly hinted at the post-meeting press conference that officials had begun considering the potential impact of Trump's policies on the economy and inflation.

The Federal Reserve's reality check on the market suppressed market sentiment before the Christmas holiday and made investors uneasy, with some analysts even predicting that if the incoming Trump administration does not moderate its campaign promises regarding taxes, tariffs, and immigration, rate cuts could even turn into rate hikes.

On Friday, the speeches of Federal Reserve officials highlighted the internal disputes within.

Cleveland Federal Reserve Chair Harmark explained her dissenting vote at this week's Federal Reserve meeting by stating that interest rates should remain stable until more progress is made in cooling inflation. In a statement released on Friday, Harmark wrote: "Based on my assessment, monetary policy is not far from a neutral position, and I tend to maintain policy stability until we see further evidence that inflation is returning to our 2% target level."

Chicago Federal Reserve President Goolsbee stated that he slightly revised up his interest rate expectations for 2025, but added that he still anticipates borrowing costs to "further drop significantly" in the next 12 to 18 months. New York Federal Reserve President Williams also advocated for further rate cuts, stating that the current monetary policy is "quite restrictive."

For Gold, with the approach of 2025, the historic rise of gold in 2024 is far from over; however, many Analysts warn investors to temper their bullish enthusiasm for gold at least in the first half of the year.

Amid the rise in US Treasury yields and the dollar, gold declined sharply over the past week. If the 10-year US Treasury yield remains above 4.50%, gold will likely struggle to maintain the $2600 level and may seem poised to test $2530 again.Resistance。

Many Analysts expect gold prices to reach $3000 per ounce next year but anticipate that gold will only rise in the second half of 2025. Meanwhile, with gold prices consolidating around $2650 per ounce, next year's target will be about 13% higher than this year's nearly 30% increase.

Chantele Schieven, Head of Research at Capitalight Research, recently stated in an interview that gold investors are in a wait-and-see mode as they try to determine the health of the economy in the fight against stubborn inflation.

Michael Widmer, Managing Director and Head of Metal Research at Bank of America, stated at the Bank of America's annual outlook webinar, "We are trapped in an environment where there are no concrete measures to bring investors back to the market."

The commodity Analyst at the USA's second-largest bank stated in its outlook report that Gold is facing significant Resistance, partly because Western investors will have to deal with potentially higher Bonds yields and a stronger dollar. Widmer stated:

"The Trump administration is likely to implement a range of policy combinations that, through stronger growth, higher inflation, higher interest rates, and a stronger dollar, will likely limit investors' interest in increasing Gold purchases in the short term."

Important data: Beware that liquidity shortage may amplify market volatility! The dollar's reign may be difficult to shake.

On Monday at 15:00, the United Kingdom's third quarter GDP year-on-year final value and third quarter current account.

On Monday at 21:30, Canada's October GDP.

On Monday at 23:00, the USA's December Conference Board Consumer Confidence Index.

On Tuesday at 21:30, the USA's November Durable Orders month-on-month.

On Tuesday at 23:00, USA will report the annualized new home sales total for November and the Richmond Fed Manufacturing Index for December.

On Thursday at 21:30, USA will report the initial unemployment claims for the week ending December 21.

On Friday at 00:00, USA will report the EIA Crude Oil Product inventory for the week ending December 20.

On Friday at 07:30, Japan will report the unemployment rate for November and the Tokyo CPI for December.

Due to the Christmas holidays, there will be fewer data releases next week.

First, in the USA, the Conference Board Consumer Confidence Index scheduled for release on Monday may attract some market attention. This index has been rising for the past two months, while one of its sub-indices—the 'Job Hard to Get' index has been decreasing during the same period. The latter is closely correlated to the official unemployment rate, so a further decline in this indicator in December would indicate faster job growth and may further boost the dollar.

On Tuesday, USA will also release the durable goods orders and new home sales data for November, with the market expecting a decline of 0.4% in November following a 0.3% increase in October's durable goods orders. However, investors often prefer the narrower non-defense capital goods orders excluding aircraft, which are less volatile and will be used for GDP calculations.

For the dollar, as the overall stance of the Federal Reserve is more hawkish, it is expected that the dollar will not easily lose its throne gained this year, although low trading volume during the holiday period may cause some unnecessary fluctuations.

Will the Japanese Yen 'rise to prominence' during Christmas?

Although Japan will not release significant data next week, the upcoming data could attract market attention following the Bank of Japan's December policy decision. Investors will also closely watch any verbal or actual Forex market interventions the Bank of Japan may take, as the Yen's free fall does not seem to be over.

The Bank of Japan indicated in the meeting that it may wait at least until after March next year to raise interest rates, at which point it will have a better understanding of how wage pressures evolve after the spring wage negotiations.

Meanwhile, Japan's inflation rate continues to hover above the Bank of Japan's 2% target. The estimate for December's Tokyo CPI will be released before the national CPI data for Japan. In November, Tokyo's core inflation rate rose to 2.2% year-on-year. If this data accelerates further in December, it will bolster expectations for an interest rate hike by the Bank of Japan in March next year, thereby boosting the Yen.

Japan will also include unemployment rate, retail sales, and preliminary data for November industrial production next Friday. Before that, Wednesday's producer prices in the services sector may trigger fluctuations in the Yen, while market trading at that time is expected to be extremely thin; at the same time, attention will turn to the meeting minutes from the Bank of Japan's October meeting released on Tuesday for further clues regarding policymakers' thoughts on interest rate hikes.

The British Pound and Canadian Dollar may also see slight recoveries.

Elsewhere, the Bank of Canada and the Reserve Bank of Australia will release their latest policy meeting minutes on Monday and Tuesday, respectively. In Canada, the GDP data for October scheduled for release next Monday will be another focus for Canadian Dollar traders.

This month, the Canadian Dollar fell to its lowest point against the US Dollar in over four and a half years.Technical aspectIt seems overbought at first glance, making a correction likely.

In the United Kingdom, if the GDP growth for the third quarter is revised upwards in the second estimate, the British Pound may experience a slight rise on Monday.

Overall, any market turbulence during the holiday season is more likely to impact US stocks and US bonds. The Federal Reserve's hawkish stance has not been well-received on Wall Street, and as US Treasury yields continue to rise, selling pressure may intensify. The US Treasury Department plans to auction two-year, five-year, and seven-year Treasury bonds on Monday, Tuesday, and Thursday respectively, which could exacerbate upward pressure on yields if demand is weak.

Company Earnings Reports: Is the recent decline in US stocks a case of 'backing up to pick someone up'?

The earnings season for US stocks has ended, and this week has been a crazy one for US stocks.

US stocks rebounded on Friday as investors digested crucial inflation data showing a slowdown in price increases for November. The Nasdaq Composite Index, which has a high proportion of technology stocks, rose by 1%. The Dow Jones Industrial Average increased by 1.2%, while the S&P 500 Index went up by 1.1%. However, this rebound was not enough to cover the losses of the three major stock indices earlier in the week. All three major US stock indices fell this week, with the Nasdaq Index down 1.8% and both the Dow Jones and S&P 500 indices down approximately 2%.

Some Analysts have begun warning investors that the risk of a pullback in US stocks is high in the near future. Market veteran Ed Yardeni expects US stocks to remain 'stagnant' in January next year, citing profit-taking, potential dock strikes, and a series of executive orders issued after Trump's inauguration.

However, he wrote on Thursday, "We cannot rule out a 10% correction in the stock market, but we believe this is a Buy opportunity, not a reason to panic and flee the market, as we do not expect a recession or a bear market."

"Tom Lee, known as the Wall Street Oracle, also believes that investors need not worry. 'For us, this panic reaction will be short-lived,' wrote the research director of Fundstrat Global Advisors. 'Wednesday was a painful day, but the fundamentals have not changed. That is why we see this as a moment to pick up bargains.'"

He noted that the VIX recorded the second-largest single-day increase on record, and stated that historically, when the VIX Index has had similar surges in the past, the stock market has fully rebounded within a month.

In addition, Lee added that the S&P 500 Index is also testing its 50-day moving average, which is the position where the index has rebounded multiple times this year after receiving support.

He also pointed out that although the Federal Reserve made hawkish comments and the policy "visibility" for the new year has weakened, investors currently still believe that the Federal Reserve will ultimately be dovish.

"In other words, the Federal Reserve still supports the market," Lee wrote. "We interpret the Fed's latest wording more as wanting to 'slow down.'"