她称,美联储本周降息25个基点的决定非常“惊险”(it’s a close call),也就是说暂不降息其实也在考虑之中,有分析认为,这是戴利在为明年1月、甚至是3月都暂停降息的预期铺路。

她称,美联储本周降息25个基点的决定非常“惊险”(it’s a close call),也就是说暂不降息其实也在考虑之中,有分析认为,这是戴利在为明年1月、甚至是3月都暂停降息的预期铺路。Analyses have pointed out that although San Francisco Fed Chair Daly and New York Fed Chair Williams both acknowledge that interest rate cuts will continue next year, they also stated that there is no rush to lower rates. All Federal Reserve officials emphasized the importance of data and acknowledged the uncertainty in the outlook. However, the Chicago Fed President, who will be a voting member next year, made more dovish comments, believing that inflation is still cooling and that interest rates need to be significantly lowered within a year and a half, which boosted U.S. stocks to open low and rise high while Treasury yields fell.

On December 20, Friday, before and after the release of the November Personal Consumption Expenditures (PCE) data, which is the inflation Index that the Federal Reserve is most concerned about, several Federal Reserve officials gave media interviews, among which the San Francisco Fed Chair, seen as Powell's "dovish ally," spoke in hawkish terms.

This year's voting committee member Daly stated: the Federal Reserve has passed the phase of policy recalibration, and the number of rate cuts next year may be less than two.

U.S. San Francisco Fed Chair and FOMC voting member Daly bluntly told Bloomberg in an interview: "My prediction is that the number of rate cuts next year will be much less than we imagine," she also mentioned that she is very satisfied with the median expectation of two rate cuts in 2025 according to the dot plot.

She stated that the Federal Reserve's decision to cut rates by 25 basis points this week was very "close call," meaning that not cutting rates was also considered, and analysts believe this is Daly paving the way for expectations of pausing rate cuts in January or even March next year.

She stated that the Federal Reserve's decision to cut rates by 25 basis points this week was very "close call," meaning that not cutting rates was also considered, and analysts believe this is Daly paving the way for expectations of pausing rate cuts in January or even March next year.

Daly stated that the current U.S. policy and economic situation is good and can return to a "more typical gradual approach," she specifically mentioned, "I feel that the Federal Reserve has passed the policy recalibration phase":

"We are entering the next stage, which is to truly examine the information we are receiving."

She also mentioned that the Federal Reserve's focus remains on inflation and unemployment, expressing concern about the current inflation rate of 2.5%, noting that inflation progress has slowed compared to the Federal Reserve's expectations, and warned, "We must remain flexible:"

We may ultimately have fewer than two rate cuts. If inflation falls more quickly, or if the labor market shows obvious signs of weakness, we may have to react, and the final number of rate cuts would be more. I am willing to wait for data to be released, and the Federal Reserve will make actual responses based on that data. We need to exercise caution now and then decide on further rate cuts.

Analysts say that Daly typically leans towards a dovish stance and is aligned with Powell, but her remarks today sound completely non-dovish and rather hawkish. The Futures market indicates a 90% probability of pausing rate cuts in January next year, and nearly a 50% chance of not cutting rates in March.

In the dot plot released on Thursday, the Fed raised the median interest rate for 2025 by 50 basis points to 3.9%, corresponding to a reduction in expected rate cuts from 4 to 2, and raised the median rate for 2026 by 50 basis points to 3.4%, implying two rate cuts. The long-term median rate was raised by 10 basis points to 3.0%.

Williams, the "third-in-command": Policy adjustments must rely on data, will continue to cut rates, but the outlook is quite uncertain.

After the release of the November PCE inflation data, which was lower than expected, Williams, the "third-in-command" of the Federal Reserve, a permanent voting member during his tenure, and president of the New York Fed, stated in an interview with CNBC that despite the unclear outlook, the Federal Reserve is still expected to continue cutting rates, as inflation has significantly dropped over the past two years and the process of inflation reduction is still ongoing.

He also reiterated, like Daly, that adjustments to policy must depend on data, and since September, the inflation data in the USA has been "slightly high," and economic growth has been "slightly stronger than" expected, with an estimated economic growth rate slowing to around 2% next year, and the unemployment rate remaining stable at current levels.

We have time to truly assess the data, evaluate what is happening, and make the best judgment based on data, outlook, and the risks of achieving the Federal Reserve's dual objectives. I believe that for the future, we are in a good position and are prepared.

Regarding the future monetary policy direction of the Federal Reserve, Williams hinted that interest rate cuts would continue, but data needs to be waited for and observed, so he would not rush to cut rates. He believes that the monetary policy after the interest rate cut this week "remains quite restrictive," and the Fed's "basic trajectory is moving toward the neutral rate (downward), and I estimate that the neutral rate is 0.25 percentage points higher than before the pandemic."

He specifically mentioned that in 2025, there is "considerable uncertainty" regarding the inflation outlook and many other factors, and acknowledged that Trump's policy proposals have begun to influence his views and economic forecasts:

"In my personal predictions, future fiscal policy, immigration policy, and other policies have been taken into account, as these are important factors affecting the economic outlook. But I want to emphasize that there is still much uncertainty regarding what these impacts will actually be."

He stated that some of the goals Trump wants to achieve regarding immigration may have already occurred, and it is expected that the number of immigrants to the USA will slow down, "We need to wait and see what the fiscal and trade policies will be," and that everything the Federal Reserve is doing now "is to prepare for any situations next year."

Previously, many economists warned that the tariffs and immigration restrictions touted by Trump could exert upward pressure on inflation, but Fed Chair Powell stated this week that the newly released forecast of "inflation slowly declining to 2%" is based on current data, not future government policy expectations.

Voting members next year: Inflation is still cooling, and interest rates need to be significantly lowered within a year and a half; this year's dissenting voting member: Waiting for inflation progress.

Similarly, after the PCE inflation data was released, 2025 voting member and Chicago Fed President Goolsbee also accepted an interview with CNBC and stated that "the expected rate cut by the FOMC in 2025 will be lower than previously estimated."

However, some analysis suggests that due to his praise for the progress in cooling inflation, believing that the inflation data released on Friday was a positive signal because it was below expectations, and the Fed is still expected to achieve the 2% inflation target, this led to US stocks opening lower and then rising, and US Treasury yields declining.

Goolsbee confirmed that although the Federal Reserve will take a cautious stance, interest rates may still decline further next year. He believes that the inflation data indicates that "the robust inflation in recent months is more of a barrier than a change of path."

His remarks are more dovish, as he mentioned that the existing policy interest rates are restrictive, "still far above the final stopping point of around 3%", and the decline in inflation means that the Federal Reserve "will need to significantly lower the policy rate in the next 12 to 18 months."

However, he admitted that the previous prediction of a 100 basis point rate cut in 2025 has now been revised to a flatter rate cut path for next year. The uncertainty of policies has led him to change his rate cut bets, but "still believes that the Federal Reserve rates will decrease by a judicious amount next year." He stated that the uncertainty of the policies of incoming President Trump has increased the difficulty of predicting the neutral rate and inflation.

He also reiterated that inflation and unemployment data will determine the central bank's future monetary policy. The labor market is stable, and it is necessary to maintain employment stability by reducing interest rates to the neutral level, but it is still "far from the neutral level." He mentioned that the Federal Reserve must also "address/deal with" the measures taken by Trump's next administration regarding inflation and employment.

In addition, at this week's FOMC meeting, the only one to express dissent and support a pause in rate cuts was the newly appointed Cleveland Fed President Harmack, who issued a written statement on Friday stating that inflation is still "elevated," the rate cut process is "unbalanced," and the strong economy is not suitable for further rate cuts at this time. He hopes for more evidence that inflation is moving towards the 2% target before rate cuts can be made:

"According to my estimates, monetary policy is not far from the neutral rate. The risks seem tilted towards rising inflation. Long-term inflation remaining above 2% may undermine the anchoring of inflation expectations, making it more difficult for inflation to return to our target level."

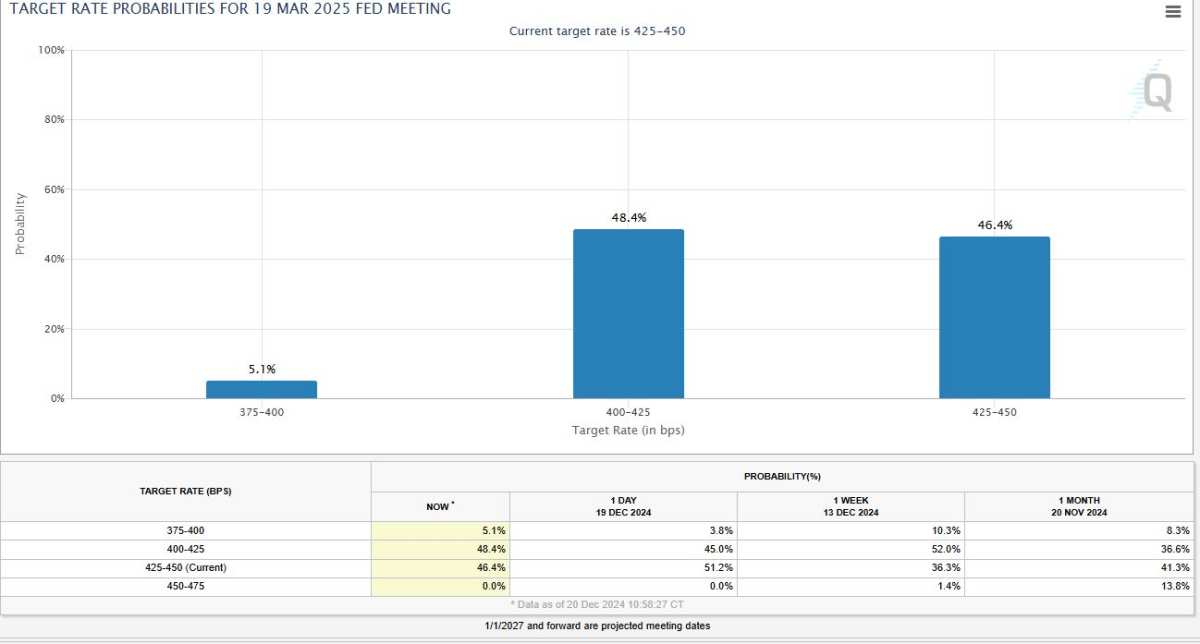

The financial market currently believes that the Federal Reserve will resume interest rate cuts in March 2025, with a possible second rate cut in October.

Editor/lambor