Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Betterware de México, S.A.P.I. de C.V. (NYSE:BWMX) does have debt on its balance sheet. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first step when considering a company's debt levels is to consider its cash and debt together.

What Is Betterware de MéxicoP.I. de's Net Debt?

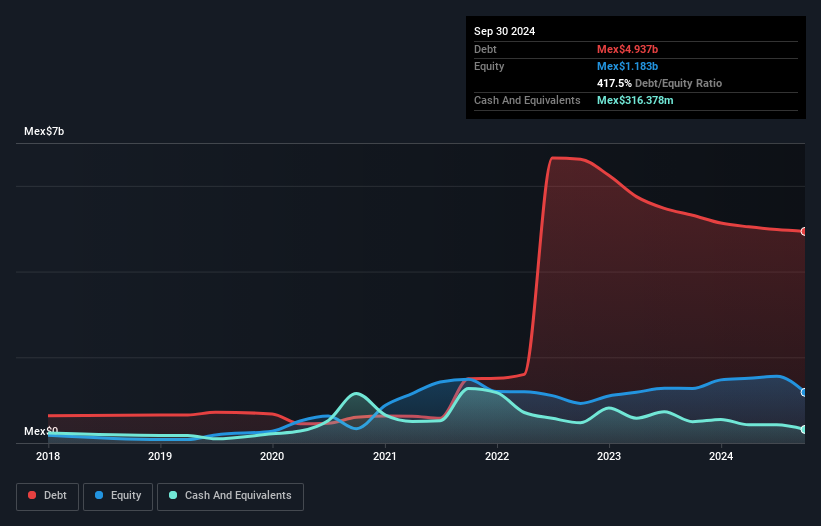

You can click the graphic below for the historical numbers, but it shows that Betterware de MéxicoP.I. de had Mex$4.94b of debt in September 2024, down from Mex$5.31b, one year before. However, because it has a cash reserve of Mex$316.4m, its net debt is less, at about Mex$4.62b.

A Look At Betterware de MéxicoP.I. de's Liabilities

According to the last reported balance sheet, Betterware de MéxicoP.I. de had liabilities of Mex$4.42b due within 12 months, and liabilities of Mex$5.28b due beyond 12 months. Offsetting these obligations, it had cash of Mex$316.4m as well as receivables valued at Mex$1.27b due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by Mex$8.11b.

According to the last reported balance sheet, Betterware de MéxicoP.I. de had liabilities of Mex$4.42b due within 12 months, and liabilities of Mex$5.28b due beyond 12 months. Offsetting these obligations, it had cash of Mex$316.4m as well as receivables valued at Mex$1.27b due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by Mex$8.11b.

Since publicly traded Betterware de MéxicoP.I. de shares are worth a total of Mex$71.9b, it seems unlikely that this level of liabilities would be a major threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Betterware de MéxicoP.I. de's net debt is sitting at a very reasonable 2.1 times its EBITDA, while its EBIT covered its interest expense just 3.0 times last year. While these numbers do not alarm us, it's worth noting that the cost of the company's debt is having a real impact. Unfortunately, Betterware de MéxicoP.I. de saw its EBIT slide 5.6% in the last twelve months. If that earnings trend continues then its debt load will grow heavy like the heart of a polar bear watching its sole cub. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Betterware de MéxicoP.I. de's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last three years, Betterware de MéxicoP.I. de recorded free cash flow worth a fulsome 80% of its EBIT, which is stronger than we'd usually expect. That positions it well to pay down debt if desirable to do so.

Our View

On our analysis Betterware de MéxicoP.I. de's conversion of EBIT to free cash flow should signal that it won't have too much trouble with its debt. However, our other observations weren't so heartening. For instance it seems like it has to struggle a bit to cover its interest expense with its EBIT. When we consider all the elements mentioned above, it seems to us that Betterware de MéxicoP.I. de is managing its debt quite well. But a word of caution: we think debt levels are high enough to justify ongoing monitoring. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 3 warning signs for Betterware de MéxicoP.I. de you should be aware of, and 2 of them shouldn't be ignored.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.