“三巫日”指的是每季度一次的ETF、股票和指数期权同时到期的日子,分别发生在每年3、6、9、12月的第三个星期五,通常会导致美股交易量飙升和价格突然波动。

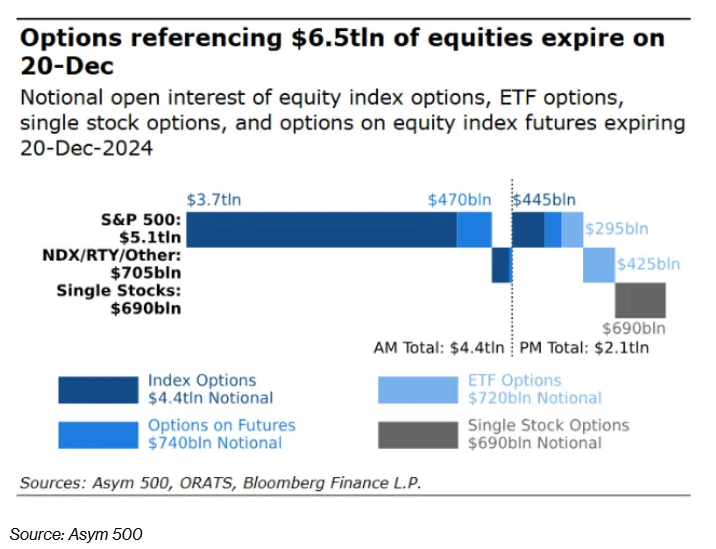

“三巫日”指的是每季度一次的ETF、股票和指数期权同时到期的日子,分别发生在每年3、6、9、12月的第三个星期五,通常会导致美股交易量飙升和价格突然波动。This Friday, the size of the Options maturing will reach about 6.5 trillion dollars, which ranks among the highest in history, and it coincides with the Index adjustment again.

As Wall Street traders respond to the Federal Reserve's outlook for a slower pace of interest rate cuts, Friday's historically volatile "Triple Witching Day" is the last barrier before they enter a calm period at the end of the year.

According to estimates from derivatives analytics firm Asym 500, about $6.5 trillion in Options will expire on this "Triple Witching Day," which is the largest scale since the beginning of the year and ranks among the largest in history, although slightly lower than a year ago.

"Triple Witching Day" refers to the quarterly expiration day when ETF, Stocks, and Index Options expire simultaneously, occurring on the third Friday of March, June, September, and December each year, usually leading to a spike in trading volume and sudden price fluctuations in U.S. stocks.

"Triple Witching Day" refers to the quarterly expiration day when ETF, Stocks, and Index Options expire simultaneously, occurring on the third Friday of March, June, September, and December each year, usually leading to a spike in trading volume and sudden price fluctuations in U.S. stocks.

The expiration of Options this quarter coincides with a critical moment for market adjustments, following the Federal Reserve's decision to cut interest rates for the third consecutive meeting on Wednesday while signaling a readiness to slow the pace of cuts. Although Wall Street investors sometimes exaggerate risks, during Options expiration, trading volumes in stocks typically spike as traders roll over existing positions or establish new ones, leading to sudden price movements.

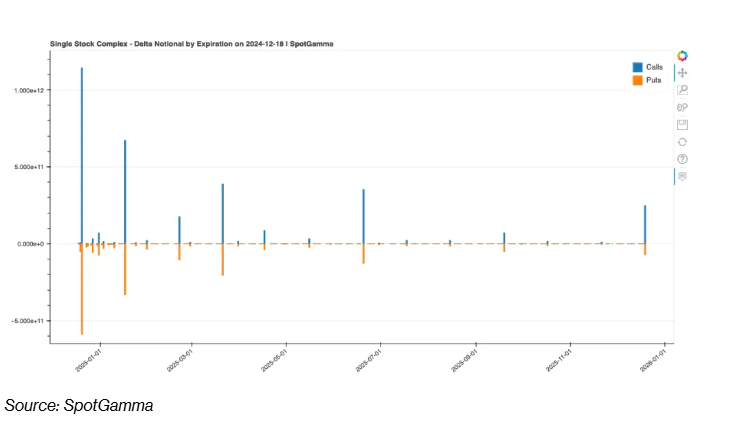

Brent Kochuba, the founder of the Options Trading platform SpotGamma, stated that in the nearing expiration of Options, the ratio of Calls to Puts is 2 to 1, a situation that has helped the stock market achieve four weeks of increases in the past six weeks.$S&P 500 Index (.SPX.US)$The stocks with the largest expiration size include some of the stocks with the largest weight in the Index, such as$Tesla (TSLA.US)$、$NVIDIA (NVDA.US)$、$Apple (AAPL.US)$、$Meta Platforms (META.US)$、$Microsoft (MSFT.US)$and$Amazon (AMZN.US)$。

Kochuba said, "We suspect that traders will sell some December expiration Put Options on Thursday and Friday, which is why the market has stabilized slightly. Closing positions may release volatility again at the end of the year."

Additionally, the expiration time of the Options coincides with the rebalancing of benchmark indexes including the S&P 500 Index on the same day, which indicates that a large number of investors will actively trade around these positions. Before the market opens on Monday,$Apollo Global Management (APO.US)$and$Workday (WDAY.US)$will replace$Qorvo (QRVO.US)$and$Amentum Holdings (AMTM.US)$to become a component of the S&P 500 Index.

Although this is still a highly watched event, the rise of short-term Options allows traders to hedge risks in a more refined manner, thus reducing reliance on contracts expiring on the third Friday of each month, which weakens the drama of "Triple Witching Day."

Chris Murphy, co-head of derivatives strategy at Susquehanna International Group, stated: "Due to the existence of zero-day Options, there are many contracts expiring daily, hence the impact of each specific expiration date contract is smaller. Additionally, since the S&P 500 Index has been rising since the election, most of the open interest in Put Options is already out of the money and cannot be exercised."

According to data compiled by Bloomberg, although the S&P 500 Index set 57 historical highs in 2024, on Wednesday it broke the record of not falling more than 1% for 21 consecutive trading days. This pushed the Cboe Global Markets Volatility Index (VIX, which measures expected volatility of the S&P 500 Index) to its highest level since early August, coinciding with a large-scale unwinding of yen arbitrage trades that unsettled the Global Bonds market.

Rocky Fishman, founder of Asym 500, stated that the S&P 500 Index has risen 2.3% since election day, "which makes the strike price of most expiring contracts well below the current market level, thus the gamma effect may be limited."

The end-of-year Options market may undergo another major change, potentially paving the way for increased volatility in 2025. Kochuba noted that on December 31, JPMorgan's Hedged Equity Fund (JHEQX) will roll over a short position in S&P 500 Index Call Options worth $21 billion, which will unwind 45,000 contracts traded at a strike price of 6055, expected to bring greater volatility to the market.

Use the option price calculator to calculate the theoretical option price in the future!

Stock Page > Options > Options Chain > Select an Option > Option Price Calculator > Change conditions to calculate the future theoretical price of the Options!

Editor/ping