This year, driven by the scrap and update policy, the mid-low end market of the car market has rebounded, with low-priced consumption rising.

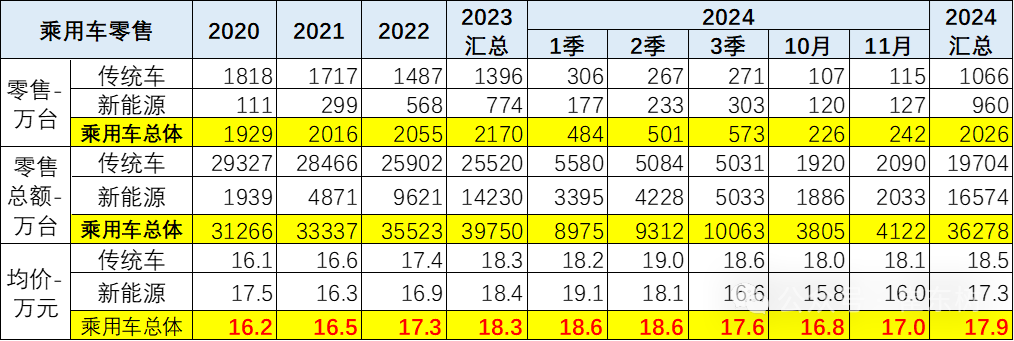

According to the Zhituo Finance APP, Cui Dongshu, Secretary-General of the Passenger Vehicle Association, released the "November Passenger Vehicle Price Segment Market Structure Analysis." Based on the data from the Passenger Vehicle Association, the price segment structure of the national retail market has been continuously rising in recent years, with significant sales increases in high-end New energy Fund models and a decrease in sales of mid-to-low price models. This year, driven by the scrapping and updating policy, the mid-to-low-end market of the car market has rebounded, and mid-to-low price Consumer spending has increased. The market share of 0.15-0.3 million yuan models continues to rise, growing rapidly. The domestic retail share of 0.2-0.3 million yuan models is 17.3% in 2023, and this November it is 18%.

According to the association's data, as of the first half of 2024, the average selling price in the car market has been on the rise, reaching 0.186 million yuan. Benefiting from the country's scrap and update policy as well as trade-in subsidies, the sales proportion of entry-level models has increased. In recent years, the price segment sales structure of the national Passenger Vehicle market has shown an upward trend. The average price of Passenger Vehicles in the country dropped from 0.183 million yuan per unit in 2023 to 0.17 million yuan in November, with strong performance across all price segments. The penetration of private cars in China is still at a low level globally, with an ownership of 200 Passenger Vehicles per 1,000 people, and the falling average price of Passenger Vehicles is driving market penetration and upgrading for comprehensive development, indicating significant future growth potential.

1. The lower the price of passenger vehicles, the more expensive they get.

1. The lower the price of passenger vehicles, the more expensive they get.

The main influence on price changes is the effect of structural changes. In recent years, car prices have shown a continuous upward trend, with 0.151 million yuan in 2019, 0.162 million yuan in 2020, and an average of 0.179 million yuan accumulated this year, with 0.17 million yuan in November. In recent years, the average selling price of Passenger Vehicles has been consistently rising, and this year, boosted by scrap and update and trade-in subsidy policies, sales of mid-low end models have notably increased. Hence, since the third quarter, the average price has dropped to 0.176 million yuan, falling to 0.168 million yuan in October and rebounding to 0.17 million yuan in November, with reduced average prices promoting comprehensive market growth.

In November, the sales proportion of entry-level Electric Vehicles and plug-in hybrids increased, resulting in an average price of 0.17 million yuan for November, which is lower than the annual average price of 0.179 million yuan. The structural reason for the average price decline in recent months is the increased proportion of entry-level pure electric vehicles, while the percentage of higher-priced hybrid and range-extended vehicles has decreased, creating structural pull. Meanwhile, the average sales price of existing RBOB Gasoline vehicles has also dropped, and the entry-level performance in RBOB Gasoline vehicles has improved.

2. Market sales structure of passenger vehicles by price segment

According to passenger car data, in recent years, the price segment structure of the nationwide retail market has been continuously rising, with significant sales increases in high-end new energy vehicles and a decrease in sales of mid to low-end models. This year, driven by the scrapping and updating policy, the mid to low-end market in the automotive sector has warmed up, and consumer spending in the mid to low price range has rebounded.

The percentage of vehicles priced below 0.05 million yuan continued to rise from 2021 to 2022 compared to 2020, mainly due to the contribution of sales from micro Electric Vehicles. However, since 2023, there has been a continuous decline, with a recovery to 3.6% after the third quarter of 2024, and the sales share of vehicles priced below 0.05 million yuan in November 2024 was 4%, an increase of 1 percentage point compared to 2023. The decline in sales of conventional vehicles priced between 0.05-0.15 million yuan, after being offset by the growth of New energy Fund vehicles, still indicates an overall declining trend.

The market share of models priced between 0.15 and 0.3 million yuan has been continuously rising, with a rapid increase. Models priced between 0.2 and 0.3 million yuan accounted for 17.3% of domestic retail sales in 2023, and this rose to 18% in November of this year.

In recent years, the market shares of various segments of models priced above 0.3 million yuan have been continuously rising, but this year has seen a decline. The retail market share of models priced between 0.3 and 0.4 million yuan was 10% in 2023, stabilizing in 2024, though it dropped to 8% in November. Models priced above 0.4 million yuan accounted for 5% of domestic retail sales in 2023, which dropped to 3% in November of this year. The breakthrough in domestic high-end vehicles reflects a significant trend in the growth of passenger vehicle new energy sectors, but the decline of traditional luxury vehicles is more severe.

3. Passenger vehicle sales structure by level

Recently, the highest penetration rate of Electric Vehicles is seen in small cars, with the penetration rate of microcars reaching 100% in November, A0 level small cars reaching 74%, and the A-grade New energy Fund showing rapid improvement.

The penetration rate of B-class and C-class vehicles has increased significantly, reflecting the significant advantages of high-end electrification.

The increase in the penetration rate of new energy in high-end vehicles mainly reflects the trend of autonomous improvement.

4. Structure of Electric Vehicles in Passenger Vehicles.

The domestic retail of pure electric New energy Vehicles continues to grow significantly, while plug-in hybrids have performed outstandingly over the past three years, with range-extenders experiencing continued slight growth. Traditional Passenger Vehicle sales are under persistent downward pressure.

In 2023, the proportion of Electric Vehicles reached a strong 36%, and in November 2024, the penetration rate for Electric Vehicles is expected to reach 52%, with a slight increase in the contribution of Electric Vehicles in the future.

5. The price and sales structure of various power types in 2024.

Currently, the core Block Orders market for Passenger Vehicles in the country is characterized by a price range of 0.05-0.15 million yuan, mainly due to the high proportion of traditional RBOB Gasoline vehicles. There is a significant difference between traditional cars and Electric Vehicles, while the structure of plug-in hybrids is relatively concentrated in the mid-range.

6. The sales structure of internal power types across different price segments in November 2024.

In the price segment market, the distribution of power is relatively uneven. Among them, pure electric vehicles perform the strongest in the market below 0.05 million yuan, while range-extended electric vehicles have a relatively strong performance in the high-end market, and hybrid vehicles perform relatively well in the 0.2-0.3 million yuan range.

Traditional RBOB Gasoline vehicles perform relatively well in the 0.1-0.15 million yuan range, creating a characteristic of differentiated distribution, especially with hybrid vehicles having a relatively narrow distribution, primarily consisting of mid-to-high priced products. Plug-in hybrids mainly belong to the mainstream models, performing excellently in the 0.1 million yuan class. The low-end market has shrunk significantly at the beginning of the year, which has also been significantly impacted by weak Consumer demand.

7. Conventional fuel passenger vehicle structure.

The high-end product structure of traditional fuel vehicles is more obvious, mainly the high growth of models priced above 0.15 million yuan, which is a direct reflection of consumption upgrade. Recently, the declining speed of fuel vehicles priced below 0.1 million yuan has slowed down. Under the high growth of pure electric vehicles, fuel vehicles have shown a sharp decline.

8. Changes in the product structure of Electric Vehicles - significant growth in the high-end segment.

With the decrease in costs and product improvements, Electric Vehicles below 0.05 million yuan are recovering quickly, while those from 0.15 to 0.3 million yuan are performing strongly. Among these, Tesla still ranks above 0.2 million to prevent excessive structural fluctuations.

Driven by the scrapping and renewal policy, there has been significant growth in New energy Fund vehicles below 0.1 million yuan recently. The proportion of Electric Vehicles in the 0.1-0.15 million yuan range has decreased, with some Electric Vehicles being the Block Orders for ride-hailing, and the A-class Electric Vehicle market has not performed strongly in the past two years. As the price of lithium carbonate falls, the micro Electric Vehicle market is recovering.

9. Changes in the product structure of Plug-in Hybrid Vehicles - significant growth in the mid-to-high-end segment.

The growth of plug-in hybrid vehicles is mainly in the Low Stock Price Range, and after mastering domestic plug-in hybrid technology, significant market share has been gained in the mid to low price market. The explosive growth of plug-in hybrids priced at 100,000 yuan in 2024 is driving their strength.

10. Changes in extended-range product structure - strong performance at the high end.

Extended-range vehicles as a branch of pure electric vehicles have been included in plug-in hybrids, and their performance has continued to strengthen over the past few years with strong demand in the high-end and 150,000 yuan segments.

Recently, the growth of extended-range vehicles has noticeably slowed, with a significant decrease in the high-end proportion, while the growth in the 100,000 to 150,000 yuan range is not very rapid.

11. Changes in the high-end share of regular hybrid products.

The market share of hybrid vehicles is also continuously increasing. The supply improvement in 2024 is leading to a gradual increase in share. The market demand driven by policy is shifting towards plug-in hybrids. The market performance of joint venture hybrids is average.

12. Changes in product share among various types of automotive companies.

In 2024, domestic brands performed very well, with the New energy making significant efforts, and both pure electric and narrow hybrid models performing excellently. Overall, the advantages of New energy are particularly notable in the high-end oil-electric hybrids brought by independent innovative technologies, while the structure of new forces fluctuates greatly. The range extender models perform better, and the market for pure electric vehicles is gradually strengthening, jointly diverting the RBOB Gasoline vehicle market. In November, independent RBOB Gasoline vehicles accounted for only 35% of the independent total.