此次美债大举抛售使得对于美联储政策变化更为敏感的短期美债收益率普遍上涨超过10个基点,达到数周以来的最高水平。美元方面,“彭博美元现货指数”周三大涨1%,对于该指数来说有很长一段时间未出现类似幅度涨幅,这一衡量美元强弱的指数一举升至2022年以来的最高点。美元走强导致其他主要货币走低。当日,欧元、英镑和瑞士法郎兑美元汇率均下跌1%,美元指数今年迄今已上涨超过7%,相对于发达国家的所有货币均大幅升值,有望创下自2015年以来的最佳年度表现。

此次美债大举抛售使得对于美联储政策变化更为敏感的短期美债收益率普遍上涨超过10个基点,达到数周以来的最高水平。美元方面,“彭博美元现货指数”周三大涨1%,对于该指数来说有很长一段时间未出现类似幅度涨幅,这一衡量美元强弱的指数一举升至2022年以来的最高点。美元走强导致其他主要货币走低。当日,欧元、英镑和瑞士法郎兑美元汇率均下跌1%,美元指数今年迄今已上涨超过7%,相对于发达国家的所有货币均大幅升值,有望创下自2015年以来的最佳年度表现。The Federal Reserve has given traders reason to expect only one rate cut in 2025, leading to a violent rise in yields across all maturities of U.S. Treasuries, with the USD reaching its highest point since 2022.

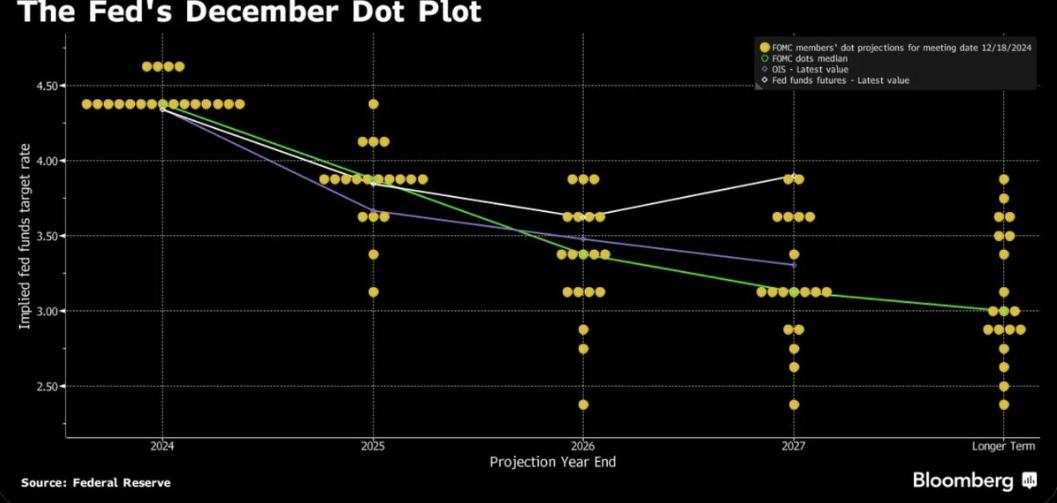

According to Zhitong Financial APP, following the Federal Reserve's interest rate decision which played out as a "hawkish rate cut" as the market expected, the management of expectations has officially entered a new phase, where it is currently in or about to slow down rate cuts. The highly anticipated "dot plot" shows that Fed officials generally expect only two rate cuts in 2025, down from the basic expectation of four cuts indicated in September, while the median long-term federal funds rate is adjusted to 3%. Following a hawkish policy statement and hawkish remarks from Powell, the U.S. Treasury market collapsed, yields on Treasuries soared, with the 10-year Treasury yield breaking 4.5%, and the USD jumped to its highest point since 2022, as traders viewed the Fed's revised forecasts as a core reason for a significant reduction in next year's rate cut expectations.

The so-called "hawkish rate cut" refers to the Federal Reserve announcing a rate cut at the December rate meeting, but the policy statement and Powell's remarks at the press conference present a strong hawkish stance. Indeed, the modified policy statement's wording indicates that the Fed is about to slow down its rate-cutting pace, with Chairman Powell showcasing "hawkish expectation management language" at the press conference following the rate cut announcement, emphasizing that inflation remains sticky and decision-makers can be more cautious when considering further rate adjustments, with any rate cut decision by the Fed in 2025 based on incoming data.

The massive sell-off of U.S. Treasuries has caused short-term Treasury yields, which are more sensitive to changes in Fed policy, to rise by over 10 basis points, reaching the highest level in several weeks. On the dollar side, the Bloomberg Dollar Spot Index surged 1% on Wednesday, marking a significant increase not seen for quite a while, while this measure of dollar strength shot up to its highest point since 2022. The strengthening dollar led to declines in other major currencies. That day, the euro, British Pound, and Swiss Franc fell 1% against the dollar, with the USD index having risen more than 7% this year, experiencing significant appreciation against all currencies of developed countries and aiming for the best annual performance since 2015.

The massive sell-off of U.S. Treasuries has caused short-term Treasury yields, which are more sensitive to changes in Fed policy, to rise by over 10 basis points, reaching the highest level in several weeks. On the dollar side, the Bloomberg Dollar Spot Index surged 1% on Wednesday, marking a significant increase not seen for quite a while, while this measure of dollar strength shot up to its highest point since 2022. The strengthening dollar led to declines in other major currencies. That day, the euro, British Pound, and Swiss Franc fell 1% against the dollar, with the USD index having risen more than 7% this year, experiencing significant appreciation against all currencies of developed countries and aiming for the best annual performance since 2015.

As expected by the market, the Federal Reserve cut rates three times on Wednesday Eastern Time, while also signaling that the pace of rate cuts may slow significantly next year. Traders responded accordingly to the Fed's new expectation management model by significantly lowering their rate cut expectations for 2025. The CME FedWatch Tool shows that interest rate futures traders generally bet on only one rate cut next year, compared to an expectation of around three cuts before the Fed's rate decision.

Priya Misra, a portfolio manager at Morgan Stanley Asset Management, stated after Powell's speech: "This is absolutely a hawkish style of Fed rate cut." The Fed's forecasts indicate that officials now generally expect only two rate cuts next year, each by 25 basis points, and have given traders reason to see only one rate cut in 2025—swap market traders even expect fewer cuts, betting on just one rate cut in 2025.

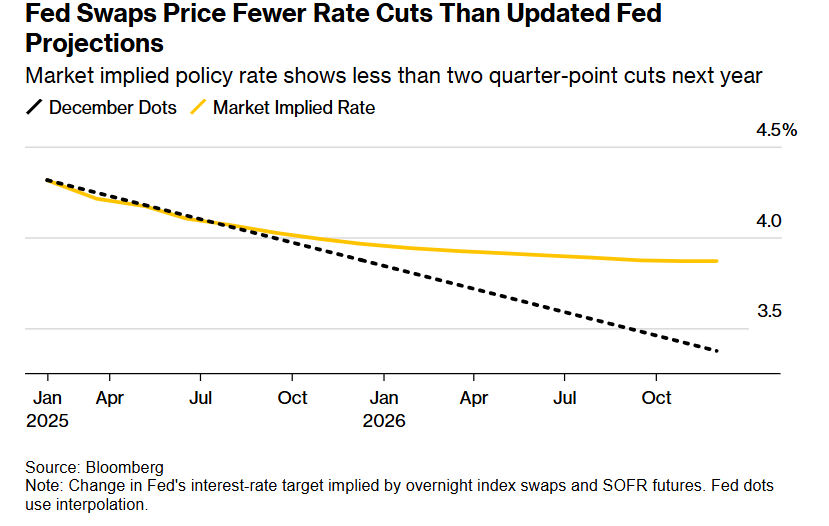

The interest rate cuts implied by the Federal Reserve swap pricing are fewer than the latest Fed forecast - the market-implied policy rates suggest that the rate cuts next year will not exceed two times.

In the policy statement on Wednesday, the Federal Reserve conveyed its monetary policy signals and a slightly cautious tone regarding the shift to a hawkish 'expected management tone', announcing a reduction of the federal funds rate target range to 4.25%-4.5%. At the same time, Fed Chairman Powell pointed out in a press conference that the recent rise in inflation is the main reason for raising the interest rate guidance.

The revised 'median quarterly forecast for the federal funds rate' by the Federal Reserve shows that Fed officials generally expect the rate to be 3.875% by the end of 2025 and 3.375% by the end of 2026. Both of these medians are a full 50 basis points higher than the median in September. The latest median expectation for the long-term neutral rate (the theoretical level that neither stimulates nor restricts economic expansion) has been raised from 2.90% to 3%.

Ed Hosseini, an interest rate strategist at Columbia Threadneedle Investments, stated that the so-called dot plot and related economic forecasts indicate that a considerable number of Federal Open Market Committee voting members (i.e., Fed FOMC voters) no longer consider the current policy path to be restrictive.

After announcing a 25 basis points rate cut on Wednesday, the benchmark interest rate level set by the Federal Reserve is a full percentage point lower than the recent peak level - the highest level in over twenty years. Powell mentioned that after the latest measures, the policy rate is now 'closer to neutral levels.'

The latest interest rate predictions in the dot plot are closer to investors' expectations before the meeting, even more 'hawkish' than most investors expected. Since mid-September, based on economic growth and inflation data, investors' expectations for the neutral rate have risen significantly. Before the interest rate decision was announced, swaps pricing related to future decisions by the Federal Reserve indicated a 25 basis points rate cut today and another 50 basis points next year, with a low likelihood of a cut in January. After the dot plot was released and Powell's press conference, swap pricing for rate cuts next year was significantly reduced, even starting to price in no cuts next year. A recent report from Deutsche Bank indicated that the bank expects that the Federal Reserve will pause rate cuts for the entire year next year, anticipating a fundamental stagnation in the Fed's easing cycle.

U.S. Treasury yields surged, breaking above 4.5%, which is the 'anchor of global asset pricing.'

In the US bond market, the yield on the two-year US Treasury bond, which is most sensitive to interest rate expectations, rose by 11 basis points to 4.35%, exceeding the three-month US Treasury bond yield for the first time since March 2023. The rise in longer-term Treasury bond yields was relatively small. Nevertheless, the yield on the 10-year US Treasury bond, known as the "anchor for global asset pricing," has broken through the important threshold of 4.5%, and is expected to set the record for the largest interest rate hike since the benchmark statistics on the day of the Federal Reserve meeting in June 2013, when signals that the central bank's asset purchases would soon slow caused a collapse in the US Treasury bond market.

The policy rate set by the Federal Reserve is a key influencing factor for Treasury bond yields. Since September, traders' expectations for further interest rate cuts have gradually weakened, pushing the 10-year US Treasury bond yield back above 4%, reaching its highest level since July. The 10-year US Treasury bond yield, regarded as the benchmark for risk-free returns, is still hovering above 4.5% and has risen over 85 basis points since mid-September, resulting in losses for those investors who bought at lower yield levels.

The latest revised economic forecast summary from Federal Reserve officials indicates that the US economy will grow faster than the predictions made by Federal Reserve officials in September, while they also expect the unemployment rate to decline at a faster pace, although they anticipate inflation rates may be higher than the expectations from September.

Bond investors have also noticed that the tax and tariff policies advocated by incoming president Donald Trump, who will officially take office next month, may significantly boost economic growth, but the likelihood of inflation resurgence has greatly expanded, and the increasing scale of the US government deficit may continuously push up the yield curve for 10-year US Treasury bonds.

Top US asset management firm T.Rowe Price believes that as the fiscal dilemma in the USA worsens and Trump’s policies lead to rising inflation, the 10-year US Treasury bond yield may rise to 6% for the first time in over 20 years. T.Rowe's Chief Investment Officer for Fixed Income, Arif Husain, stated in a report that the benchmark 10-year US Treasury bond yield may first reach 5% in the first quarter of 2025 and may rise further. Husain further raised his forecasts for US Treasury bond yields due to Trump's tax cuts during his second presidential term continuing to sustain the US budget deficit, and the potential tariffs and immigration policies will keep US price pressures persistent.

As traders begin to worry that Trump’s policies will stimulate inflation and increase fiscal pressure in the USA, the outlook for US Treasury bonds has become increasingly bleak. T.Rowe Price’s expectation of a yield as high as 6% for the 10-year bond seems more pessimistic than some peers, while ING Groep believes the 10-year US Treasury bond yield could reach 5% to 5.5% next year, and Franklin Templeton and JPMorgan Asset Management expect it to reach 5%.

From a theoretical perspective, the 10-year US Treasury yield corresponds to the risk-free interest rate indicator r in the important valuation model for the stock market—DCF valuation model. If other indicators (especially cash flow expectations on the numerator side) do not show significant changes, a higher denominator level or sustained operation at historical highs will put pressure on the valuations of risk assets such as US technology stocks, high-risk corporate bonds, and Cryptos, which are at historically high valuations.

Gregory Farinello, head of US Interest Rates Trading and Strategy at AmeriVet Securities, said, "We even think the Fed will have completed its task by next year. The Trump administration will pull the trigger, and the Fed will be on guard."

The Fed's anti-inflation ambition is to try to bring down the inflation rate to a long-term average of 2% or even below, but the inflation rate rose to 2.3% in October. The November PCE inflation indicator, expected to be released on Friday, is projected to show a year-on-year increase of 2.5%, while core PCE may rise to 2.9%.

"It was expected that US Treasury yields would rise after Trump was elected in November," said Bridge Kulana, a portfolio manager at Wellington Management. "I expect that if inflation remains at the current level, the Fed may stand pat for the entire year next year."

The dollar surged to its highest level in two years and is expected to continue rising in 2025.

After the Fed hinted that it would significantly slow down monetary easing next year, the dollar index rebounded to its highest level in over two years. The Bloomberg Dollar Spot Index rose by 1% on Wednesday Eastern Time, reaching its highest level since 2022. This surge caused other sovereign currency Exchange Rates to drop sharply, with the euro, British Pound, and Swiss Franc all falling more than 1% against the dollar that day.

So far this year, the dollar index has risen by more than 7%, increasing against all sovereign currencies of developed countries, and is on track to have the best performance since 2015.

Skyler Montgomery Conning, a forex strategist at Barclays, stated after the Federal Reserve meeting that as economic data is strong, the Federal Reserve's expectations have become more hawkish, supporting the rise of the USD.

Helen Given, a forex trader at Monex, said: "Given the change in median inflation forecasts, the Federal Reserve seems to be beginning to expect the potential inflation impact of Trump's new trade policies." "This is the secret to the USD strengthening at least before the monetary policy meeting in January next year, or at least not experiencing substantial weakness."

President-elect Donald Trump vowed to impose severe tariffs on many American trading partners, which helped the USD to surge prior to Trump's official inauguration. As the economic performance of the USA and levels of Treasury yields surpass those of many other countries, the rebound continues. Meanwhile, many central banks globally will have to significantly lower borrowing costs to help boost weak economic data.

"The Federal Reserve's policy statement and every detail of Powell's speech are undeniably hawkish," said Paresh Upadhya, head of fixed income and forex strategy at Amundi US. "All of this indicates that the USD will strengthen significantly as it continues to amplify the narrative of 'growth exceptionalism' under Trump's leadership of the USA."

On Wednesday, a benchmark measuring emerging market currencies against the USD fell 0.4% to its lowest level since August. The Brazilian Real dropped about 3% against the USD that day, reaching a historical low as investors grew increasingly concerned about the country's fiscal crisis.

"As monetary policy paths diverge and other factors emerge, we believe the USD will strengthen significantly by 2025," said Brendan McKenna, an emerging markets economist and forex strategist at Wells Fargo & Co in New York, prior to the Federal Reserve's interest rate decision. Wells Fargo predicts an average appreciation of about 5% to 6% for the USD against the major currencies of the Group of Ten (G10) next year.

However, Wall Street strategists are beginning to predict that the world's reserve currency, the USD, may peak as early as mid-next year before significantly declining against other sovereign currencies later in 2025, as global easing cycles begin to recover and economic growth in countries outside the USA starts to outperform that of the USA. From Morgan Stanley to JPMorgan, about six well-known sell-side strategists now predict that the USD may peak as early as mid-next year and then start to decline; Société Générale expects that the ICE USD index will drop by about 6% before the end of next year, stating recently: "The strength of the USD is nauseating, and we are pushing the price of an asset to a level that is unsustainably high in the long term."