沃尔玛的支持者们对其前景持乐观态度,他们相信公司在广告、第三方市场和配送服务等新业务领域的多年投资将开始收获成果,从而显著提升毛利率。这些业务的增长动态将成为4月份零售商投资界会议的焦点,届时市场专家将密切关注相关进展。

沃尔玛的支持者们对其前景持乐观态度,他们相信公司在广告、第三方市场和配送服务等新业务领域的多年投资将开始收获成果,从而显著提升毛利率。这些业务的增长动态将成为4月份零售商投资界会议的焦点,届时市场专家将密切关注相关进展。Source: Zhito Finance

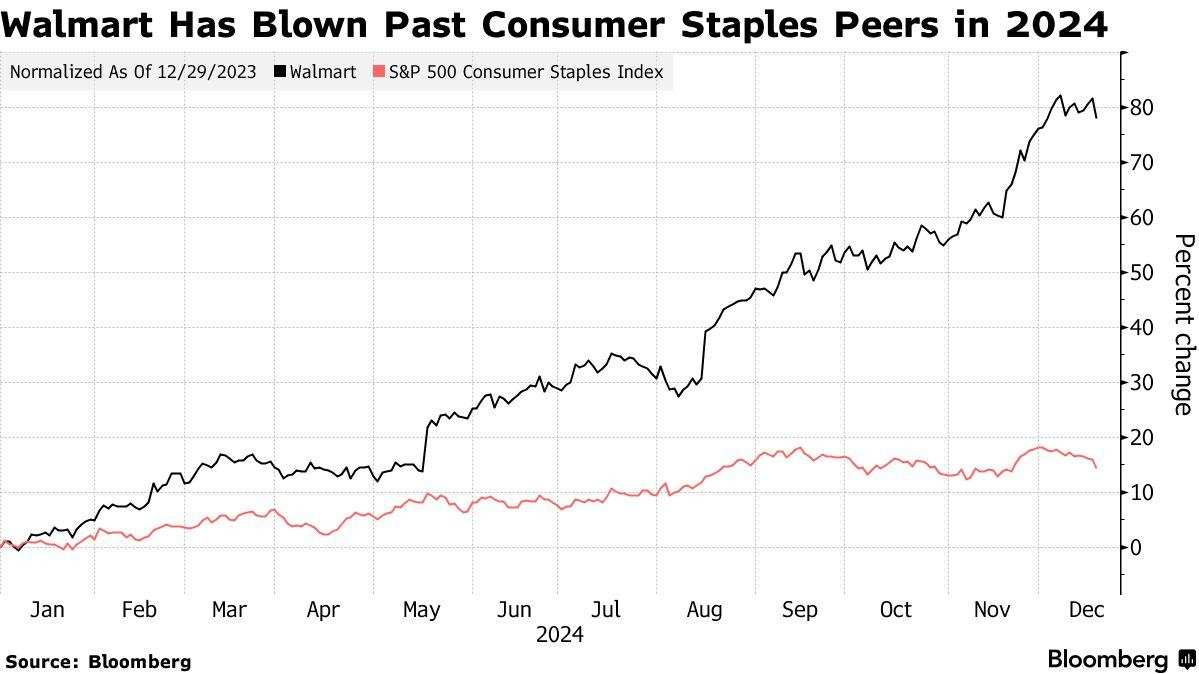

Against the backdrop of signs of economic slowdown in the USA and doubts about Consumer resilience, $Walmart (WMT.US)$Walmart has emerged as a strong contender, demonstrating robust growth momentum. As the world's largest Retail Trade, Walmart is not only known for its discounted prices but has also made significant progress in advertising and the online market, with expectations to achieve its best performance year since 1998 this year. Its stock price surged by 80%, and Market Cap increased by approximately 330 billion USD, far exceeding peers like $Dollar Tree (DLTR.US)$and$Dollar General (DG.US)$, and outperformed competitors. $Target (TGT.US)$ 、$Amazon (AMZN.US)$and $Costco (COST.US)$ Analysts and investors predict that Walmart will continue to stand out in the future, with its high-margin auxiliary business further expanding market share and increasing profits.

As the best-performing company in this year’s S&P 500 Consumer Index, Walmart contributed about half of the 14% increase in the Index. Walmart's success is primarily attributed to its focus on selling household essentials, convenient delivery options, renovated stores, and a broader range of products, attracting a wider customer base that includes high-income consumers. In particular, households with annual incomes of $100,000 or more contributed about 75% to Walmart's Market Share growth in the third quarter.

Supporters of Walmart are optimistic about its prospects, believing that years of investment in new Business areas such as advertising, third-party markets, and delivery services will begin to pay off significantly, thus enhancing gross margin. The growth dynamics of these businesses will be the focus of the retail investment community meeting in April, where market experts will closely follow the relevant developments.

Supporters of Walmart are optimistic about its prospects, believing that years of investment in new Business areas such as advertising, third-party markets, and delivery services will begin to pay off significantly, thus enhancing gross margin. The growth dynamics of these businesses will be the focus of the retail investment community meeting in April, where market experts will closely follow the relevant developments.

Currently, about one third of Walmart's revenue comes from advertising and membership services, and the growth in this proportion has provided the company with the ability to expand profit margins while maintaining competitive pricing for Commodities. Steven Shemesh, an analyst from Royal Bank of Canada Capital Markets, believes this gives Walmart a "significant competitive advantage," as other competitors that have not yet matured in these areas will face difficult choices: either compress margins to maintain price competitiveness or risk losing Market Share by allowing price gaps to widen.

Shemesh gave Walmart Stocks a "Buy" rating and listed it as a top investment for 2025. Additionally, Analysts and investors are closely monitoring the development trends of Walmart's E-Commerce Business. Walmart announced in June that its U.S. E-Commerce division is expected to be profitable in the next two years, further boosting market confidence in Walmart.

Analysts' Views.

Keith Buchanan, Senior Portfolio Manager at GLOBALT Investments, stated that Walmart's stock performance "looks more like a Technology stock," and its growth and profit margin expansion have made some large Tech companies envious. Although GLOBALT has reduced its Shareholding due to Walmart's stock price increase this year, Buchanan still predicts that by 2025, Walmart's stock performance will surpass the Large Cap Index and remarked that Walmart is currently in its prime.

Citigroup Analyst Paul Lejuez predicted that Walmart will continue to seize market share from dollar stores by enhancing its delivery options and increasing awareness of the Walmart+ Assist program (which allows eligible government assistance recipients to join Walmart+ at a discount). Meanwhile, the renovation of Walmart stores has optimized the shopping experience for Outfits, Housewares, and beauty products, and strengthened the Pet Supplies department, which may pose a threat to Target and pet supply vendors, he added.

"Over the past three years, Walmart has consistently held our top position, and we have never wavered in our Bullish view of it," Lejuez said, giving Walmart Stocks a "Buy" rating. He further pointed out that the acceleration of daily necessities sales is expected to inject "a new round of growth momentum" into Walmart's stock price.

Analyst Daniela Nedialkova from Redburn Atlantic predicted that the trend of differentiation within the Retail Trade sector will further intensify in 2025 amid ongoing macroeconomic pressures. Although she is also Bullish on Walmart, she believes that the stock price increase in 2025 may not replicate this year's brilliance.

However, Walmart's success is not without controversy. Walmart's current expected PE is around 34 times, significantly higher than its average PE over the past decade – about 21 times, and far exceeds the overall PE level of the S&P 500 Index. By this measure, even the relatively high-valued Amazon has a PE of only 32 times, which appears relatively low.

Nonetheless, Analysts and investors generally believe that Walmart is hard to compare with any other company. Lejuez from Citigroup pointed out that Walmart, as a large retailer, not only has an impressive scale but also possesses younger and higher-margin business segments, exhibiting characteristics of a 'junior version of Amazon.'

John San Marco, the portfolio manager investing in Walmart through the Neuberger Berman Next Generation Connected Consumer ETF, stated: 'Walmart has risen to be a leader among high-quality retailers, fundamentally different from ordinary retail businesses. I firmly believe that discussing Walmart's competitive advantage a year from now is highly probable.'

Overall, Walmart has become a highly favored stock, with its fan base continually growing. At the beginning of this year, nearly 80% of analysts tracked by Bloomberg recommended buying Walmart. This percentage has steadily risen to over 90%, nearing historical highs.

Analysts and investors generally believe that Walmart's competitive advantages are very evident and it is expected to continue maintaining strong growth momentum in the future. Despite its high valuation, its significant competitive advantages and diversified business model make it difficult to be replaced by other companies.

编辑/jayden