On December 18, 2024, local time, the Federal Reserve held a monetary policy meeting, lowering the target federal funds rate Range by 25 basis points to 4.25%-4.50%, while maintaining the pace of balance sheet reduction, which involves Shareholding $25 billion per month in treasury bonds and $35 billion per month in MBS.

Event

On December 18, 2024, local time, the Federal Reserve held a meeting to discuss interest rates, lowering the target Federal Funds Rate Range by 25 basis points to 4.25%-4.50%. The pace of balance sheet reduction remains unchanged, specifically a Shareholding of 25 billion dollars per month in U.S. Treasury securities and 35 billion dollars per month in MBS.

Core Viewpoint

Core Viewpoint

Overall, economic resilience still exceeds the Federal Reserve's expectations, leading Powell to increase tolerance for inflation. Combined with upward adjustments to economic and inflation readings, a reduction in the unemployment rate, and the dot plot, it is likely that the Federal Reserve may start to pause interest rate cuts in January 2025. If employment data worsens, or if risks similar to the major adjustments in U.S. stocks in Q4 2018 arise, the Federal Reserve may resume rate cuts.

In terms of Assets, at the beginning of this month, the Schiller cyclically adjusted PE ratio of the S&P 500 Index reached a high of 38.86 times (the peak in November 2021 was 38.58 times). Coupled with the Federal Reserve's rate cuts being put on hold in 2025 and fiscal policy tightening, the downside risks for U.S. stocks are increasing. Unlike the performance of Chinese Assets, which is often driven by expectations, the trends in U.S. stocks typically show retrospective patterns. The sharp decline of U.S. stocks following this monetary policy meeting bears some similarity to the post-Taper situation in November 2021. However, the continued decline of U.S. stocks post-November 2021 was also related to the U.S. economic recession in the first half of 2022, which may indicate that economic changes will become the core contradiction for U.S. stocks in the next six months. Before the conflict between Russia and Ukraine ends, due to the Federal Reserve pausing rate cuts, rather than the central banks in the USA continuing the rate cut cycle, bond yields and the USD may remain elevated.

Main text

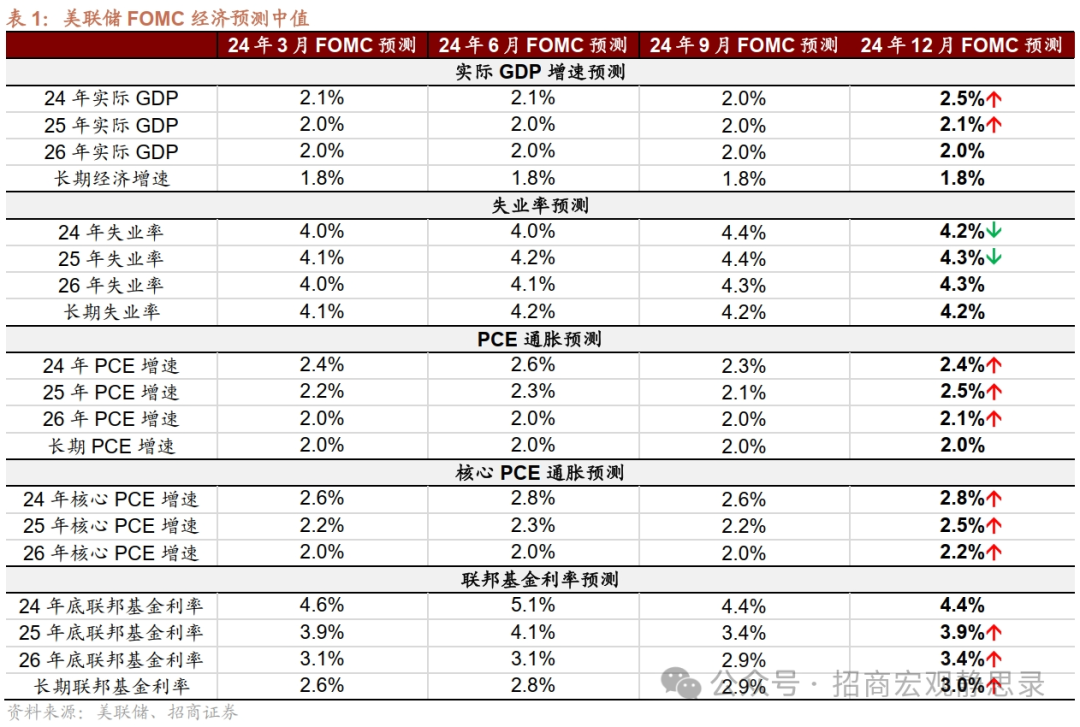

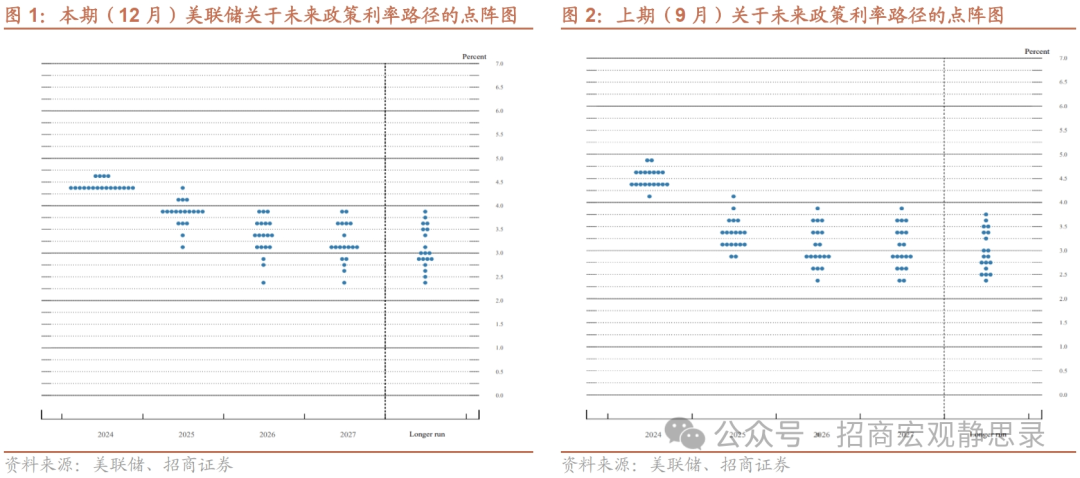

The Federal Reserve's hawkish rate cuts have resulted in upward revisions of economic and core inflation expectations for the coming years, and a downward revision of next year's unemployment rate. The dot plot anticipates a reduction of 50 basis points in both 2025 and beyond. The main changes in the economic forecast are: 1) the median expected GDP growth rates for 2024, 2025, and 2026 are 2.5%, 2.1%, and 2.0%, respectively (the September forecasts were 2.0%, 2.0%, and 2.0%); 2) the median expected core PCE growth rates for 2024, 2025, and 2026 are 2.8%, 2.5%, and 2.2%, respectively (the September forecasts were 2.6%, 2.2%, and 2.0%); 3) the median expected unemployment rates for 2024, 2025, and 2026 are 4.2%, 4.3%, and 4.3%, respectively (the September forecasts were 4.4%, 4.4%, and 4.3%); 4) the median expected federal funds rates for 2024, 2025, and 2026 are 4.4%, 3.9%, and 3.4%, respectively (the September forecasts were 4.4%, 3.4%, and 2.9%). The dot plot anticipates a 50 basis point cut in 2025 and a 50 basis point cut in 2026 (the September forecast was a 100 basis point cut in 2025 and a 50 basis point cut in 2026). Compared to November, the recent FOMC statement included the phrase "consideration of further adjustments to the federal funds rate target Range" followed by "magnitude and timing," indicating that the pace of rate cuts may have begun to slow. Additionally, the president of the Cleveland Fed, Harker, expressed dissent, hoping for a pause in the rate cuts in December.

Signals released from Powell's speech and Q&A: Increased confidence in the economy, extending the anti-inflation realization cycle, and slowing the pace of interest rate cuts.

1) Economy: Continuing to expand at a steady pace. Economic conditions are very good; Consumer spending remains resilient, with increases in equipment and intangible asset investment, while real estate performance is weak; Improved supply conditions support the strong performance of the USA economy over the past year; It is expected that next year will be a good year for the USA economy.

2) Employment: Minimizing downside risks. Although the unemployment rate has increased compared to last year, it remains at a low level; The tightness of the labor market is lower than in 2019; The labor market is not the main source of inflation pressure; Employment growth is now far below the level needed to keep unemployment steady.

3) Inflation: Extending the anti-inflation cycle. Inflation has significantly eased over the past two years but is still above the 2% target; Housing costs are steadily declining; No further easing is needed to bring inflation down to 2%; It may take another 1-2 years to achieve the 2% target.

4) Interest Rate Path: More cautious about rate cuts. When considering further adjustments to the policy rate, we can be more cautious; Regarding 'magnitude and timing,' 'magnitude' means that the possible extent of rate cuts is significantly reduced, and 'timing' indicates that if the economy develops as expected, it is currently or close to the stage of slowing rate cuts; At around 4.3%, policy remains significantly restrictive; An interest rate hike seems unlikely next year.

How to understand the current attitude of the Federal Reserve and the subsequent policy rhythm? A pause in rate cuts may occur in January next year, with a total rate cut of about 50 basis points throughout the year, likely concentrated in the second half. Powell's remarks indicate that as long as the economy and employment remain stable and inflation remains persistent, a pause in rate cuts is highly likely, with rate cuts triggered by an increase in economic and employment risks or rapid declines in inflation. It is expected that under the resonance of stable economy and asset prices, along with upward risks in inflation, the probability of the Federal Reserve pausing rate cuts in Q1 or even H1 next year is higher; If Trump policies trigger an economic slowdown and US stock market ceases to rise, then the Federal Reserve may reconsider rate cuts.

Market reaction: US stocks plummeted, the USD strengthened, US Treasury yields rose, and Gold fell. As previously anticipated, this release of interest rate cut signals is comparable to the Taper in November 2021. The three major US stock indices, the S&P 500, Nasdaq, and Dow Jones Industrial Average, fell by 2.95%, 3.56%, and 2.58%, respectively. The 2-year and 10-year US Treasury yields each rose by 10 basis points to 4.35% and 4.50%; the USD rose by 1.23% to 108.26; COMEX Gold fell by 2.34%.

Judgment on various Assets: US stock market volatility is intensifying, with US Treasury yields and the USD index oscillating at high levels. Currently, the total market value of US stocks has reached 64 trillion USD, more than twice the total economic output of the USA. At the beginning of this month, the Shiller cyclically adjusted PE of the S&P 500 reached as high as 38.86 times (exceeding the peak of 38.58 times in November 2021), coupled with the Fed's interest rate cuts in 2025 and fiscal tightening, the downside risk for US stocks is increasing. Until the end of the Russia-Ukraine conflict, due to the Fed's pause on interest rate cuts, while the People's Bank of China is still in a rate-cutting cycle, US Treasury yields and the USD index may remain at high levels.

Risk warning:

The USA economy exceeds expectations, and the Fed's monetary policy exceeds expectations.

This article is reprinted from the 'China Merchants Macro Insight' WeChat public account, edited by Chen Xiaoyi of Zhitong Finance.