这家全球市场份额排名第三的NAND闪存产品制造商在经过多年复杂且范围极其广泛的谈判后上市,这些谈判涉及贝恩资本、韩国财团SK Inc.、西部数据公司以及日本政府。该公司的IPO价格处于其首次公开发行前夕所提议的IPO价格区间的中间位置。相比之下,日本交易所集团的数据显示,今年登陆日本股市的大多数给出价格区间的上市交易最终都以IPO区间上限以上的价格首次亮相。

这家全球市场份额排名第三的NAND闪存产品制造商在经过多年复杂且范围极其广泛的谈判后上市,这些谈判涉及贝恩资本、韩国财团SK Inc.、西部数据公司以及日本政府。该公司的IPO价格处于其首次公开发行前夕所提议的IPO价格区间的中间位置。相比之下,日本交易所集团的数据显示,今年登陆日本股市的大多数给出价格区间的上市交易最终都以IPO区间上限以上的价格首次亮相。The chip manufacturer Kioxia's stock price surged by 17% on its first day of listing in Tokyo; asset management institutions indicated that Kioxia's IPO returns reflected the market's optimistic outlook on the recovery of memory chip demand.

According to the Zhitong Finance APP, after presenting a downward trend during the opening phase of the Japanese stock market, Kioxia significantly rose against the trend on its debut day in the Japanese stock market, with the increase gradually expanding, and its stock price far exceeding its IPO price, reflecting a recovery in investment enthusiasm for memory chips in the Capital Markets. Since July, the bleak investment sentiment towards memory chips had once severely impacted the stock prices of memory giants SK Hynix, Samsung, and Micron, but recently, the market's bullish sentiment towards memory chips has clearly re-emerged, which also explains Kioxia's decision to delay its listing in Japan until December. This bullish wave has propelled Micron (MU.US) to rebound significantly by 15% since December in the US stock market. Some asset management institutions noted that Kioxia's IPO returns on the first day reflected the market's optimistic outlook on the recovery of Consumer storage demand.

On December 18, after Kioxia debuted on the Japanese stock market, its latest valuation reached approximately 877 billion yen (about 5.7 billion USD); by Wednesday's close in the Japanese stock market, Kioxia's stock price closed up over 11%, having once soared more than 17% during the day. However, this latest market cap remains only a small fraction of what Bain Capital-led financial consortium paid when acquiring the company for 18 billion USD in 2018. Kioxia's stock price closed up 1601 yen on its first day of listing, peaking at 1689 yen, while its initial public offering price was 1455 yen.

This manufacturer of NAND flash products, ranked third in global market share, went public after years of complex and extensive negotiations involving Bain Capital, the South Korean consortium SK Inc., Western Digital, and the Japanese government. The company's IPO price was set in the middle of the proposed IPO price range just prior to going public. In contrast, data from the Japan Exchange Group indicates that most companies listed in the Japanese stock market this year that provided price ranges eventually debuted at prices above the upper limit of the IPO range.

This manufacturer of NAND flash products, ranked third in global market share, went public after years of complex and extensive negotiations involving Bain Capital, the South Korean consortium SK Inc., Western Digital, and the Japanese government. The company's IPO price was set in the middle of the proposed IPO price range just prior to going public. In contrast, data from the Japan Exchange Group indicates that most companies listed in the Japanese stock market this year that provided price ranges eventually debuted at prices above the upper limit of the IPO range.

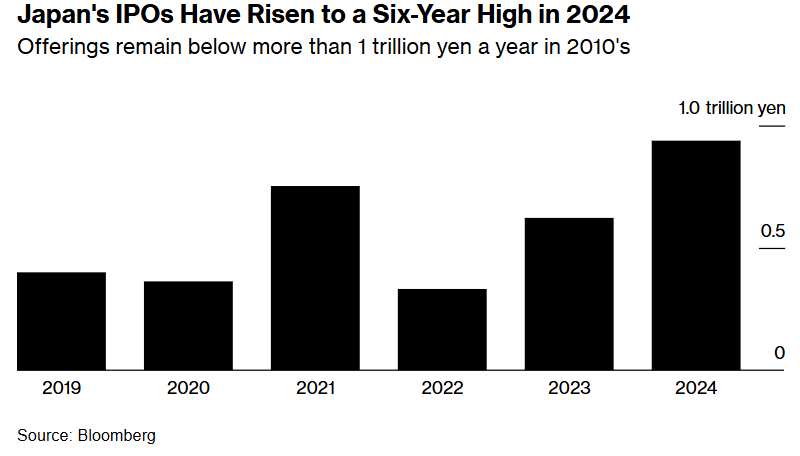

In 2024, the number of initial public offerings (IPOs) in Japan has risen to its highest level in six years.

Seiichiro Iwamoto, a fund manager at Japan's top asset management company Asset Management One, stated: "The stock price movements reflect expectations for both the company and the recovery of Consumer storage chips." He mentioned that the relatively low IPO price also aids in attracting Bid power from global investment institutions.

According to data compiled by Bloomberg, Kioxia's PB is about 1.87x, while its competitor Micron Technology from the USA has a PB of about 2.67x.

This year, major companies raised about 938 billion yen through initial public offerings (IPOs) on the Japanese stock market, the highest amount since 2018. Data collected by Bloomberg shows that although the large listings, including those of Japan's subway operator Tokyo Metro and X-ray equipment manufacturer Rigaku Holdings Corp., attracted global investors' attention, the number of IPO transactions has fallen to the lowest level in the Japanese stock market in a decade, indicating that large company listings are dominating Japan's IPO market.

Polarization of storage chips: enterprise-level storage demand is exploding, while consumer-level has not yet shown a clear recovery.

According to statistics and the latest research reports from Wall Street investment institutions covering the storage field, the storage chip market has shown significant differentiation trends this year: the demand for DRAM and NAND at the consumer electronics level is weak, mainly due to the continued sluggish demand for consumer electronics such as smart phones and PCs, while the demand for enterprise-level NAND and high-bandwidth memory (HBM) is experiencing explosive expansion due to the global AI boom.

Investors are paying attention to whether Kioxia will benefit like other storage chip companies from the multitrillion-dollar data center hardware spending that large cloud computing giants such as Microsoft and Amazon are driving globally over the next few years.

Kioxia mainly focuses on NAND flash and 3D NAND storage solutions and is one of the world's leading storage product suppliers, having significant market influence in the enterprise-level storage field (such as datacenters and enterprise-grade SSDs). Since ChatGPT sparked an epic boom in generative AI among global enterprises, the demand for enterprise-grade SSDs has expanded significantly, which is the core logic driving investors' optimism about Kioxia's future performance and consequently raising Kioxia's stock price. However, compared to storage giants like Micron and SK Hynix, current public information shows that Kioxia has not entered the HBM storage market, which is a limiting factor for its market valuation, largely constrained to below 10 billion dollars.

Although NAND flash products do not read and write as fast as DRAM and HBM, their large capacity and low cost make them an ideal choice for long-term data storage. In generative AI computing systems, enterprise-grade SSDs (enterprise flash hardware products based on NAND Flash technology) are usually used to store large-scale training/inference datasets and trained models. When training or re-inference loads are required, the data is quickly loaded into DRAM or HBM for processing.

The demand for enterprise-level NAND (such as datacenter SSDs) is surging due to the rapid expansion of datacenters and cloud computing. Micron announced in its earnings report that revenue from its datacenter SSD business more than tripled year-on-year in fiscal year 2024, setting revenue records for the quarter. According to Wall Street analysts, in the next 2-3 years, enterprise-level NAND and HBM will continue to benefit from AI training/inference systems, updates and fine-tuning of large AI models, and strong demand for cloud AI inference computing power, becoming the main growth points of the storage chip market.

The market begins to expect a recovery in consumer-grade storage demand.

Currently, NAND flash memory—the core storage chip used to store information in Smart Phones and personal computers—has not completely recovered from a long-term price slump, which has been caused by a surplus of inventory due to the decline in demand for global mobile consumer electronics and PCs since the peak demand during the COVID-19 pandemic. One of Kioxia's competitors, Western Digital, recently warned that consumer-grade NAND prices remain weak in the fourth quarter. It is reported that Western Digital and Kioxia operate a manufacturing joint venture in northern Japan.

The surge in AI interest is driving demand for expensive HBM storage systems. These 3D stacked chip systems are extremely difficult to manufacture and require chip manufacturers to use a large portion of their storage chip production capacity resources, making it challenging to significantly increase capacity. This will significantly reduce the risk of future inventory surplus, which has long plagued the storage industry. The CEO of Micron has repeatedly emphasized that the surge in HBM demand means that the pace of HBM capacity expansion will accelerate, which also has profound impacts on the overall supply and prices of DRAM and NAND. This CEO expects that the overall supply of DRAM and NAND will gradually fall short of demand, with prices likely to rise steadily. This is also the logic behind some traders' bullish view on the recovery of Kioxia's NAND flash product prices.

In addition, the trend of integrating large AI models led by Apple Intelligence into consumer electronics at the edge is also expected to drive DRAM and NAND demand into a phase of explosive growth. The AI vision showcased by Apple at WWDC means that starting in 2024, large AI models will gradually begin to integrate into consumer electronics such as PCs, Smart Phones, and smartwatches, and possibly even humanoid robots shortly after, ushering in an era of embodiment for AI intelligence. The demand for storage capacity across major terminals may exhibit exponential growth trends. This is also the core logic behind some research institutions' recent upward revisions of storage chip demand expectations for the next few years, following Apple's WWDC.

According to TrendForce's forecasts, by 2025, sales of DRAM storage products are expected to reach $136.5 billion, indicating a year-on-year growth of 51%; NAND flash sales are expected to reach $87 billion, with a year-on-year growth of 29%.

Amir Anvarzadeh, a Japan stock strategist at Asymmetric Advisors, stated that there are currently no early signs indicating that Kioxia's IPO will "completely ignite the storage market." "Nevertheless, considering its relatively weak industry background, the stock price still surged significantly on its listing day, and the IPO price was positioned in the middle of the pricing range. This fact signifies that the market is relatively optimistic about the recovery of demand for consumer-grade storage chips."