① Shanghai Sanyou Medical Co., Ltd plans to acquire the remaining equity of its holding subsidiary Shuimu Tianpeng. After evaluation, Shuimu Tianpeng appreciated by 0.693 billion yuan, with an appreciation rate of 406.21%. ② Shanghai Sanyou Medical Co., Ltd stated that the acquisition will enhance the company's overall profitability. Before the acquisition, Shanghai Sanyou Medical Co., Ltd had continuously faced declining performance.

According to the Star Daily report on December 17 (Reporter Zheng Bingxun), the orthopedic implant company Shanghai Sanyou Medical Co., Ltd (688085.SH) formally replied to the inquiry from the Shanghai Stock Exchange regarding the acquisition of the holding subsidiary "Beijing Shuimu Tianpeng Medical Technology Co., Ltd" (hereinafter referred to as "Shuimu Tianpeng") on the evening of the 16th. About a week ago, Shanghai Sanyou Medical Co., Ltd had just announced a delayed response to the inquiry.

According to the transaction proposal disclosed by Shanghai Sanyou Medical Co., Ltd, it will purchase a total of 37.1077% equity of Shuimu Tianpeng held by Cao Qun and Xu Nong through the issuance of shares and cash payment, as well as 98.9986% contribution share of "Shanghai Huanzhan Enterprise Management Partnership (Limited Partnership)" (hereinafter referred to as "Shanghai Huanzhan") held by Zhan Songtao and others. At the same time, through its wholly-owned subsidiary Tuoteng Suzhou, it will cash acquire the remaining 1.0014% contribution share of Shanghai Huanzhan.

Before this transaction, Shanghai Sanyou Medical Co., Ltd already held 51.82% equity of Shuimu Tianpeng. After the acquisition, Shanghai Sanyou Medical Co., Ltd's direct shareholding ratio in Shuimu Tianpeng will increase to 88.92%. Shanghai Huanzhan, as the employee stock ownership platform of Shuimu Tianpeng, holds 11.08% equity of Shuimu Tianpeng. This means that after the transaction is completed, Shanghai Sanyou Medical Co., Ltd will directly and indirectly hold 100% equity of Shuimu Tianpeng.

Before this transaction, Shanghai Sanyou Medical Co., Ltd already held 51.82% equity of Shuimu Tianpeng. After the acquisition, Shanghai Sanyou Medical Co., Ltd's direct shareholding ratio in Shuimu Tianpeng will increase to 88.92%. Shanghai Huanzhan, as the employee stock ownership platform of Shuimu Tianpeng, holds 11.08% equity of Shuimu Tianpeng. This means that after the transaction is completed, Shanghai Sanyou Medical Co., Ltd will directly and indirectly hold 100% equity of Shuimu Tianpeng.

The total transaction price is approximately 0.416 billion yuan. To complete the transaction, Shanghai Sanyou Medical Co., Ltd will also raise 0.214 billion yuan through private placement.

It is worth noting that Shuimu Tianpeng has come under scrutiny due to the asset assessment appreciation exceeding 406% in this acquisition, while the performance commitment made by Xu Nong, the actual controller of Shanghai Sanyou Medical Co., Ltd, for several years to come has further raised doubts from the outside.

In the inquiry letter issued by the Shanghai Stock Exchange, the necessity of this transaction, business synergy, and performance commitments became the focus of attention.

Is the acquisition at an appreciation rate of 406% reasonable?

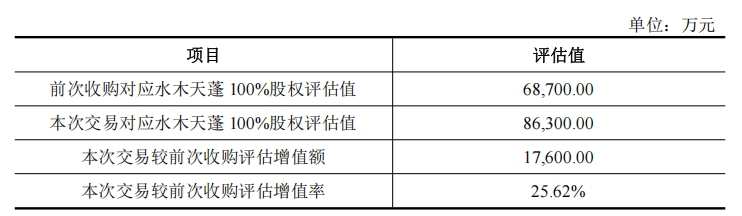

The trade plan shows that as of April 30, 2024, the book value of Shuimu Tianpeng owned by the parent company is 0.17 billion yuan, with a valuation assessed by the income method of 0.863 billion yuan, resulting in an appreciation of 0.693 billion yuan, an appreciation rate of up to 406.21%. During the same period, the valuation for Shanghai Haizhan was 95.5807 million yuan, with no valuation appreciation.

In fact, this is not the first time Shanghai Sanyou Medical Co., Ltd has made a high premium acquisition of Shuimu Tianpeng.

In July 2021, Shuimu Tianpeng initiated its third equity transfer since its establishment, with Shanghai Sanyou Medical Co., Ltd acquiring 49.88% of its equity for 0.343 billion yuan in cash. At that time, the net assets attributed to the parent company's shareholders of Shuimu Tianpeng were 80.7561 million yuan, with an assessed valuation of 0.687 billion yuan, resulting in an appreciation rate of 750.71%.

It can be observed that both acquisitions were made at a high premium, and this time the overall valuation of Shuimu Tianpeng is also 0.176 billion yuan higher than the previous one, with an appreciation rate of 25.62%.

This move attracted the attention of the Shanghai Stock Exchange, which required Shanghai Sanyou Medical Co., Ltd to explain the reasonableness of the assessed appreciation rate in the context of acquiring minority shares compared to the previous assessment.

Shanghai Sanyou Medical Co., Ltd explained that at the time of the previous acquisition, the products of Shuimu Tianpeng were limited to ultrasonic bone power equipment (including mainframe, cutter heads, and other consumables), and since then, Shuimu Tianpeng's ultrasonic hemostatic knife, ultrasonic suction knife, and other products have gradually obtained registration certificates, further opening up market space.

Secondly, according to data from Qianlima Bidding Network, during the previous acquisition, Shuimu Tianpeng's winning bid rate was about 40%-45%, whereas from January to October 2024, Shuimu Tianpeng's winning bid rate was 57.14%, showing a significant increase.

Data shows that Shanghai Sanyou Medical Co., Ltd officially landed on the Star in 2020, mainly engaged in the research and development, production, and sales of orthopedic spinal implant consumables, ultrasonic bone knives, ultrasonic hemostatic knives, and trauma-related implant consumables. Shuimu Tianpeng is one of the leading companies in the field of ultrasonic bone knives, with products used in various clinical departments including orthopedics, neurosurgery, and hepatobiliary surgery.

The Shanghai Stock Exchange requires Shanghai Sanyou Medical Co., Ltd to explain the purpose and necessity of acquiring the remaining equity after already controlling Shuimu Tianpeng, as well as how this acquisition will help improve the financial situation of Shanghai Sanyou Medical Co., Ltd compared to the previous acquisition.

In response, Shanghai Sanyou Medical Co., Ltd stated that when making significant operational decisions, it must be approved by shareholders holding more than two-thirds of the voting rights. Previously, it only held 51.82% of Shuimu Tianpeng's equity, which somewhat reduced decision-making efficiency. Meanwhile, since 2021, Shanghai Sanyou Medical Co., Ltd has maintained a relatively independent sales team from Shuimu Tianpeng, and this acquisition will leverage the promotional experience of Shanghai Sanyou Medical Co., Ltd to assist in the development of Shuimu Tianpeng's consumables business.

Shanghai Sanyou Medical Co., Ltd also stated that compared to the previous acquisition, the current business capacity and financial situation of Shuimu Tianpeng have improved.

Firstly, in 2020, the total assets of Shuimu Tianpeng were 0.108 billion yuan, total liabilities were 26.64 million yuan, and net assets were 81.6516 million yuan. These three indicators as of April 30, 2024, are 0.186 billion yuan, 11.3293 million yuan, and 0.175 billion yuan respectively.

Secondly, in 2020, the revenue and Net income of Shuimu Tianpeng were 52.4279 million yuan and 2.6337 million yuan respectively, which increased to 92.6877 million yuan and 41.6136 million yuan in 2023, representing an increase of 76.79% and 1480.04% respectively.

Shanghai Sanyou Medical Co., Ltd stated that if the acquisition was completed at the beginning of 2023, the company's consolidated Net income for that year would increase from 95.5829 million yuan to 0.115 billion yuan, a year-on-year increase of 20.63%.

However, what Shanghai Sanyou Medical Co., Ltd did not point out is that based on the above calculation method, the total liabilities of Shanghai Sanyou Medical Co., Ltd for the year 2023 would also increase from 0.219 billion yuan to 0.42 billion yuan, an increase of 91.81%. In the first four months of 2024, the total liabilities of Shanghai Sanyou Medical Co., Ltd are expected to increase from 0.268 billion yuan by 75.15% to 0.468 billion yuan, while the consolidated net loss will expand from 3.8939 million yuan to a loss of 5.9514 million yuan.

▌Is the performance commitment confidence or boasting?

The reporter from the Star Daily found that when Shanghai Sanyou Medical Co., Ltd decided to acquire Shuimu Tianpeng at a high premium, its overall performance was experiencing a continuous decline, which may reflect Shanghai Sanyou Medical's attempt to seeking a breakthrough.

After years of rapid growth, Shanghai Sanyou Medical's performance showed signs of weakness in 2022, achieving revenue of 0.649 billion yuan and a Net income of 0.191 billion yuan, with year-on-year growth of 9.40% and 2.39%, respectively, a decline in growth rates of 42.57% and 54.81% compared to 2021. Entering 2023, Shanghai Sanyou Medical's revenue and Net income were 0.46 billion yuan and 95.5829 million yuan, respectively, a significant year-on-year decrease of 29.08% and 49.91%.

Shanghai Sanyou Medical revealed that in 2023, due to the implementation of the national procurement of high-value spinal consumables, the sales price of its spinal products significantly declined, with spinal business revenue achieving 0.354 billion yuan, a year-on-year decrease of 34.20%, which dragged down overall revenue and Net income.

At that time, Shanghai Sanyou Medical stated that 2023 was a year when the company faced significant pressure from the procurement in the orthopedic industry, and due to the large decrease in the terminal hospitalization prices of its major spinal and trauma products after procurement, there was a risk of declining performance.

Clearly, as the national procurement of high-value spinal consumables is implemented nationwide in 2024, Shanghai Sanyou Medical's performance continues to be under pressure. In the first three quarters of 2024, Shanghai Sanyou Medical achieved revenue of 0.333 billion yuan, a year-on-year decrease of 7.30%, and a Net income of 8.5706 million yuan, a year-on-year decrease of 87.07%.

In this context, Shanghai Sanyou Medical stated that acquiring Shuimu Tianpeng would enhance the strategic synergy between the two companies, beneficial for improving the overall profitability of the company.

In fact, regarding this transaction, Xu Nong made a performance commitment for Shuimu Tianpeng.

If the transaction is completed by the end of 2024, the performance commitment for the years 2024-2026 for Shuimu Tianpeng's Net income is 40.1346 million yuan, 47.7337 million yuan, and 55.18 million yuan, respectively. If the completion date of the transaction is delayed to 2025, then Shuimu Tianpeng's Net income for 2025-2027 will be 47.7337 million yuan, 55.18 million yuan, and 65.363 million yuan, respectively.

In terms of corresponding revenue, it is expected that the revenue of Shanghai Sanyou Medical Co., Ltd's Shuimu Tianpeng from 2024 to 2027 will be 0.121 billion yuan, 0.141 billion yuan, 0.168 billion yuan, and 0.198 billion yuan respectively. Further ahead, the revenue in 2029 is expected to be 0.282 billion yuan. Therefore, from 2024 to 2029, Shuimu Tianpeng is expected to achieve a compound annual growth rate of 18.44%.

However, from 2019 to 2023, the compound annual growth rate of the global ultrasonic osteotome market was only 4.22%, while in China it was 9.36%.

The Shanghai Stock Exchange requires Shanghai Sanyou Medical Co., Ltd to explain why the anticipated operating income growth rate of Shuimu Tianpeng exceeds the industry growth rate, as well as the prudence and feasibility of the related forecasts.

Shanghai Sanyou Medical Co., Ltd replied that from January to November 2024, Shuimu Tianpeng has achieved sales revenue of 90.5366 million yuan, with a completion rate of 74.78%. Data from the past five years (2019-2023) shows that the fourth quarter has been the peak sales season, with December's sales accounting for 30%-45%.

Conservatively estimated, the total sales revenue of Shuimu Tianpeng for 2024 is 0.113 billion yuan, with a completion rate of 93.63%. If optimistic, the total sales could reach 0.127 billion yuan, with a completion rate of 105.09%.

In addition, according to information from Qianlima Bidding Network, the market share of Shuimu Tianpeng in 2022 and 2023 was 51.08% and 46.20% respectively, leading the industry.

At the same time, from 2020 to 2023, Shuimu Tianpeng achieved revenues of 52.4279 million yuan, 65.4092 million yuan, 73.8387 million yuan, and 92.6877 million yuan, with a compound annual growth rate of 20.92%, higher than the industry's average annual compound growth rate of 10.97% during the same period.

Shanghai Sanyou Medical Co., Ltd also revealed that the overall market penetration and growth rate of the ultrasonic osteotome is relatively low. As academic education and clinical promotion develop, the ultrasonic osteotome will gradually replace traditional osteotomy tools, leading to significant market potential in the future.

According to New Thinking's prediction, the overall market size for ultrasonic bone knives in China (including equipment and consumables) is expected to grow from 0.246 billion yuan in 2023 to 0.801 billion yuan in 2028, with a compound growth rate of 26.63%. Shanghai Sanyou Medical Co., Ltd believes that the industry's growth rate exceeds their estimated 18.44%, reflecting a prudent principle.