在12月降息25个基点的同时,美联储决策者们可能将为2025年缩减宽松规模做好准备,以应对特朗普政府上台后通胀反弹的预期。

在12月降息25个基点的同时,美联储决策者们可能将为2025年缩减宽松规模做好准备,以应对特朗普政府上台后通胀反弹的预期。① Currently, the industry generally expects that the Federal Reserve will stage a "hawkish rate cut" this week; ② While cutting rates by 25 basis points in December, Federal Reserve policymakers may prepare to reduce the scale of easing by 2025 in response to expectations of a rebound in inflation after the Trump administration takes office.

According to Financial Associated Press on December 17 (Editor: Xiaoxiang), after consecutive five days of significant gains last week, U.S. bond yields fluctuated on Monday (December 16) before the Federal Reserve's rate decision is announced this week, with the market falling into a wait-and-see mode.

Currently, the industry generally expects that the Federal Reserve will stage a "hawkish rate cut" this week:

While cutting rates by 25 basis points in December, Federal Reserve policymakers may prepare to reduce the scale of easing by 2025 in response to expectations of a rebound in inflation after the Trump administration takes office.

The above expectations have already been reflected in the curve structure of the U.S. bond market: market participants are moving away from longer-term government bonds and are more inclined to Hold bonds from the front end to the middle of the curve, specifically bonds ranging from two to five years.

Concerns about high interest rates and rising inflation typically prompt the sale of long-term government bonds, thereby pushing up long-term U.S. bond yields, as investors require a premium to compensate for the risks of holding long-term bonds.

"Hawkish rate cut" expectations dominate.

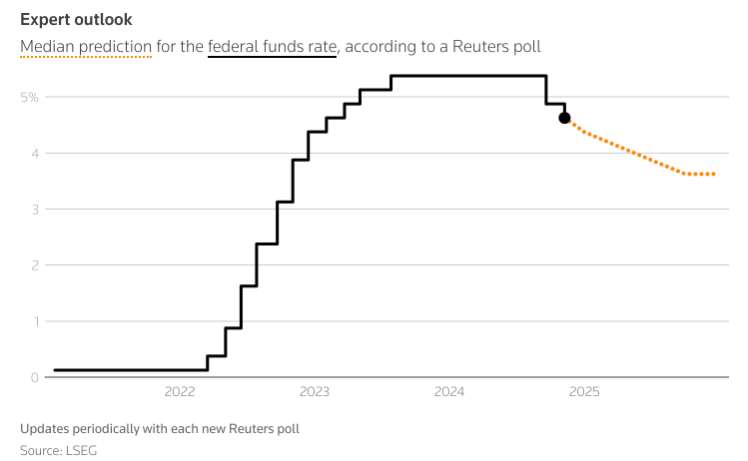

It is widely expected that the Federal Reserve will lower the benchmark rate by 25 basis points, to a target Range of 4.25%-4.50%, at the conclusion of a two-day policy meeting starting on Tuesday. However, compared to the rate cut decision for December itself, what actions the Federal Reserve will take next year may be the more pressing Topic of concern for many.

Currently, some 'hawkish' outlooks are overshadowing the market.

At least one bank—BNP Paribas believes that the Federal Reserve will keep interest rates stable for the entirety of next year and will not return to cutting rates until mid-2026. Other banks, however, think that the Federal Reserve may make two to three cuts of 25 basis points next year. But the possibility of cutting rates four times as indicated by the September dot plot seems quite slim.

George Bory, Chief Investment Strategist for Fixed Income at Allspring Global Investments, stated that hawkish rate cuts align with recent data expectations and will also fit potential policy adjustments that the new government might make. 'The Federal Reserve is trying to prepare the market for a slowdown in the pace of rate cuts and... increase options to track data and be prepared for policy changes.'

Former Cleveland Fed President Loretta Mester recently also stated that the Federal Reserve's prior prediction of four cuts next year 'must be reconsidered,' predicting that the pace of cuts in 2025 will 'slow down,' and 'two to three cuts seem appropriate to me.'

Sam Stovall, Chief Investment Strategist at CFRA Research, pointed out that 'the probability of the Federal Reserve cutting rates on Wednesday is almost 100%, the only outstanding issue is what kind of statements and guidance investors will hear. I expect this will likely be a hawkish cut - this means they will cut rates, but the Fed will discuss how they are still data-dependent, so the number of cuts next year could be fewer than people expect.'

In addition to the overall number of cuts next year potentially being fewer than indicated on the September dot plot, some industry insiders expect another 'hawkish' aspect of the Fed's decision could suggest a pause in rate cuts as early as January.

Goldman Sachs, in a research report released last Sunday, believed that the Federal Reserve may hint at slowing the pace of rate cuts in this week's meeting and 'skip' a rate cut in January. Goldman noted that the key question during the policy statement and the press conference is whether to emphasize a slowdown in the pace of rate cuts or still decide based on data from each meeting. They expected the Federal Reserve to convey both messages and add hints of slowing the pace of easing in the statement.

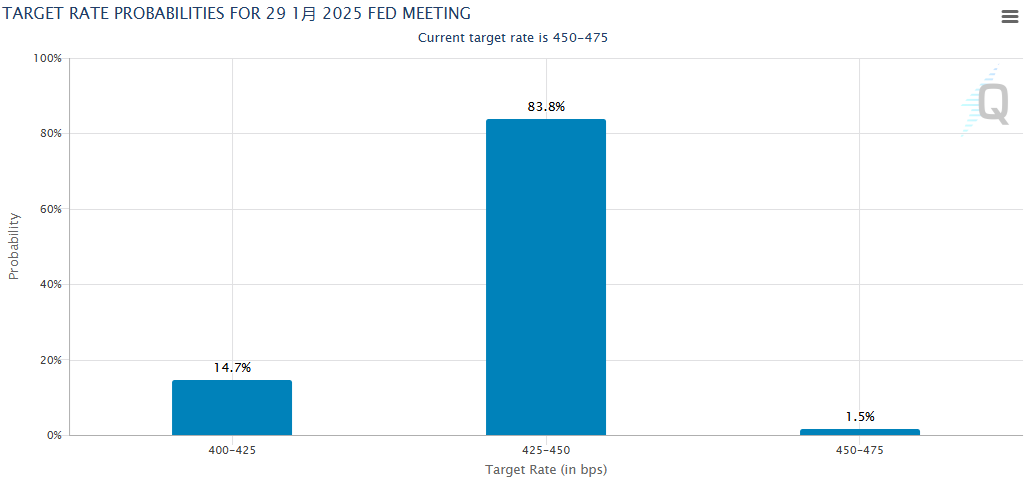

Goldman's view is relatively consistent with market expectations. According to the CME FedWatch Tool, the probability of the Federal Reserve further cutting to 4.00%-4.25% in January is only 14.7%. 'The New Federal Reserve Correspondent' Nick Timiraos also stated on Monday that one option for the Federal Reserve this week is to cut by a quarter percentage point and then strongly hint through new economic forecasts that the central bank is ready to slow the pace of rate cuts.

Chilton Trust’s Chief Investment Officer for Fixed Income, Tim Horan, stated, "I absolutely agree with the idea of the Federal Reserve holding off in January to see how fiscal policy develops before making a decision. Of course, rate cuts are still possible in March and the first half of the year. If the December dot plot average predicts three rate cuts next year, then they might occur in March and June, with another one potentially in September, perhaps not until December; this adjustment towards a neutral policy can take many forms, depending on the rise in risks and uncertainties around fiscal policy."

Has the U.S. bond market made a determination?

In fact, a series of recent changes in the U.S. bond market has anticipated the Federal Reserve's upcoming adjustments to its easing policy.

Over the past year, U.S. bond investors have been extending their durations or purchasing longer-term Assets, as they continue to prepare for the Federal Reserve's easing policy and potential economic recession. As interest rates decline, higher-yield Bonds often become more attractive, leading to price increases.

However, recently, some investors have reduced their durations, opting to focus on short-term Treasury Bonds or maintaining a neutral stance.

Jay Barry, head of Global Interest Rate Strategy at JPMorgan, stated, "Currently, no one really wants to significantly extend durations. This will be a shallow easing cycle."

The U.S. 10-Year Treasury Notes Yield surged by as much as 24 basis points last week, marking the largest weekly increase this year. Data from the Commodity Futures Trading Commission (CFTC) shows that ahead of this week’s Federal Reserve meeting, Asset Management companies reduced their net long positions in longer-term assets like Treasury Futures, while leveraged funds increased their net short positions in such durations.

Bory from Allspring noted that investors are generally steering clear of the long end of the yield curve, as this relies on the supply of U.S. Treasury and long-term inflation expectations.

Market participants expect that with the election of Donald Trump as President of the USA and his plans to cut taxes and impose tariffs on a range of imported products, inflation in the USA will accelerate again. These measures may expand the fiscal deficit, put pressure on the long end of the yield curve, and push up long-term bond yields.

Kathy Jones, Chief Fixed Income Strategist at Charles Schwab, stated: "Tariffs are a potential inflation risk as they can lead to rising import prices. They may ultimately result in a one-time price shock or become a sustained source of inflation."

Societe Generale expects that by the end of next year, the year-on-year increase of the U.S. CPI will reach 2.9%, and by 2026 it will reach 3.9%, partly due to the imposition of tariffs. As inflation rises, the bank expects the Federal Reserve to maintain interest rates unchanged in 2025.

James Egelhof, Chief U.S. Economist at BNP Paribas, stated that given the resilience of the economy and the growing concerns about the monetary policy potentially nearing neutrality, the Federal Reserve has shown an attitude of "reluctance to ease policy." The Federal Reserve will not simply overlook the temporary inflation rebound caused by tariffs.

Get a preview of major financial events and discover investment opportunities early! Open Futubull > Market > U.S. Stocks >Financial Calendar/Selected macroeconomic datato seize investment opportunities!

Get a preview of major financial events and discover investment opportunities early! Open Futubull > Market > U.S. Stocks >Financial Calendar/Selected macroeconomic datato seize investment opportunities!

编辑/jayden