CEO陈福阳(Hock Tan)在稍后财报电话会上预测称,目前的三大科技客户将在2027财年花费600亿至900亿美元购买博通供应的人工智能组件。

CEO陈福阳(Hock Tan)在稍后财报电话会上预测称,目前的三大科技客户将在2027财年花费600亿至900亿美元购买博通供应的人工智能组件。Source: The Intelligent Investor

Author: The Intelligent Investor

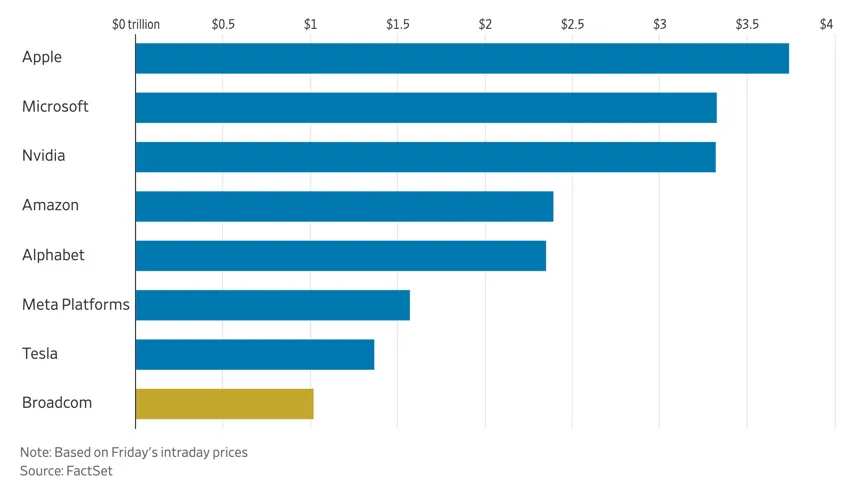

The "Fabulous Seven Giants" in the US stock market welcomed a new member of the "Trillion Club" last Friday,$Broadcom (AVGO.US)$。

This chip manufacturer barely surpassed Wall Street's expectations in its latest quarterly earnings report, but the company had prepared a Christmas surprise in advance.

CEO Hock Tan predicted during the later earnings call that the current three major technology clients will spend between 60 billion and 90 billion dollars on AI Components supplied by Broadcom in the fiscal year 2027.

CEO Hock Tan predicted during the later earnings call that the current three major technology clients will spend between 60 billion and 90 billion dollars on AI Components supplied by Broadcom in the fiscal year 2027.

Given Broadcom's generally not very boastful style, this prediction directly ignited market enthusiasm. The stock rose 24% on Friday, hitting an all-time high, and the market cap surged to 1.05 trillion dollars.

Following the artificial intelligence giant NVIDIA's breakthrough of this milestone last year, the company is the second chip manufacturer to reach this milestone.

Compared to its peers, Broadcom's rise is also somewhat unconventional. In 2009, the company's total Market Cap was only 4 billion USD, growing 250 times over 15 years.

The technology website Digits to Dollars has a very incisive summary, stating that "Broadcom is a publicly traded private equity fund disguised as a semiconductor company."

In comparison to Jensen Huang of NVIDIA and Lisa Su of AMD, Chen Fuyang does not come from a formal background and is particularly low-key. His systematic speeches and interviews are nearly impossible to find.

Understanding him more often comes from each quarterly earnings call.

In a rare brief interview with CNBC this year, Chen Fuyang stated that the enterprise customer market is where the 'big players' are located. 'The demand for accelerators' XPUs and networks is a niche market. Today, these customers invest in GPU or XPU clusters worth hundreds of thousands of dollars, while their target is million-dollar clusters in four years. We work closely with each customer.'

But what exactly is Broadcom? How did it become so large?

We trace back and define it through an article. The main materials for this article are sourced from The Asianometry Newsletter, with some content edited and supplemented by Smart Investor (ID: Capital-nature).

Origin: HP's Spin-Off

The company now known as Broadcom was originally the product of several splits.

In March 1999, the famous California computer manufacturer Hewlett-Packard decided to split the company, divesting all businesses unrelated to computers, IT, and printers, and established a new company—Agilent Technologies.

This newly listed company took over HP's previous testing and measurement, medical products, chemical analysis, and semiconductor businesses, accounting for about 8 billion dollars of HP's total revenue of 47 billion dollars.

Analysts at the time believed that this spin-off was a necessary focus on an overly large business.

Ned Barnhold, the CEO of the new company Agilent, compared the spin-off to "stepping out of the shadows" in an interview.

On Agilent's first day of trading, the stock price surged nearly 70%, becoming one of the largest IPOs in history.

However, during the difficult years following the burst of the Internet bubble and the fiber-optic bubble, the company's performance plummeted, with revenue dropping nearly 50% from its peak in 2000, leading to large-scale layoffs and the sale of entire business units to raise funds.

In June 2005, Agilent Technologies decided to sell its chip division - Semiconductor Products Group. After a brief auction, the private equity firms KKR and Silver Lake ultimately won the deal in August 2005 for $2.65 billion.

At that time, the Singapore government also participated in the investment through its sovereign wealth fund Temasek and the Government of Singapore Investment Corporation (GIC). Since HP Inc established a factory there in 1970, Singapore has been an important partner for HP Inc.

This deal occurred during the golden age of private equity investment - between 2006 and 2007, many of the largest private deals in history were completed just before the global financial crisis. For example, the transactions involving utility company TXU, financial services company First Data, and hospital company HCA all exceeded $20 billion.

Although this Agilent divestiture deal was not large in scale, both KKR and Silver Lake were very optimistic about its growth potential.

HP Inc's semiconductor division can be traced back to 1961, when the electronics giant believed it was necessary to bring component production in-house.

Over time, the division expanded its business into multiple industries, with some important products including FBAR RF filters for mobile phone radios, optical transceivers, and custom chips for HP Inc printers (to lock in users to purchase its cartridges).

However, with the rise of wafer foundries in the 1990s, the economics of having an in-house semiconductor division fundamentally changed.

Despite Agilent's efforts to diversify, the cyclical nature of its business and persistently low profit margins led it to face losses during economic downturns. Additionally, in 2004, 17% of the semiconductor division's revenue still depended on HP Inc. Management eventually realized that this business was not the company's core.

Thus, in December 2005, Avago Technologies was born. This company became the largest private pure-play semiconductor company in the world.

The first CEO of Avago was its original general manager, Dick Chang, who initially joined HP Inc laboratories and later became the head of the semiconductor products division.

However, a few months after the company's establishment, Avago announced the appointment of a new president and CEO—Chen Fuyang.

About Chen Fuyang.

Chen Fuyang is of Chinese descent from Malaysia. He received a scholarship to the Massachusetts Institute of Technology (MIT) at the age of 18, obtained his bachelor's degree, and then went on to Harvard Business School to earn an MBA.

Afterwards, he returned to Malaysia and worked at several companies.

First at Hume Industries, a cement manufacturing company belonging to a large Malaysian conglomerate. Then, he joined a venture capital firm called Pakven Investment. After that, he returned to the USA, where he held financial positions at PepsiCo and General Motors.

In 1992, he joined the personal computer company Commodore International.

At Compaq, Chen Fuyang served as Vice President of Finance and Chief Financial Officer during a difficult period when the iconic computer company faced massive losses and sluggish sales.

After Compaq announced bankruptcy in 1994, Chen Fuyang left the company and joined a chip company called ICS (Integrated Circuit Systems) as Senior Vice President of Finance.

ICS, the company, is also worth mentioning.

It was established in the late 1970s, located in Valley Forge, Pennsylvania.

Initially, it was a design company responsible for designing semiconductor products but did not sell products, mainly providing outsourced design services for large companies like United Technologies and General Electric.

In the late 1980s, ICS developed an innovative product—the Silicon Timing Device, also known as a frequency timing generator.

Every electronic system requires a timing component, and traditional ICs used crystals to accomplish this function. The silicon timer replaced these crystals with a pure silicon solution, a breakthrough of significant importance.

After the product achieved great success, ICS went public in 1991.

In his second year with ICS, Chen Fuyang served as the Chief Financial Officer and the following year also took on the role of Chief Operating Officer.

In 1999, ICS announced that the management team would acquire the company through a leveraged buyout, with a transaction amount of 0.257 billion USD, financed by Private Equity firms Bain Capital and Bear Stearns.

After completing the aforementioned capital operations, Chen Fuyang officially became the CEO of ICS, at which point his exceptional financial skills had already become apparent.

In 2005, ICS merged with another company that produced mixed-signal chips, Integrated Device Technology, in a deal worth 1.7 billion USD.

Chen Fuyang became the chairman of the merged company.

At this time, Silver Lake Partners extended an olive branch to recruit him as the CEO of Agilent Technologies.

Chen Fuyang's 'franchise' concept.

Silver Lake Partners' co-founder and chairman Kenneth Howe commented on Chen Fuyang during an interview with Bloomberg:

He believes that the semiconductor industry has matured, and the operational methods of companies must differ from the rapidly growing era of the past.

Chen Fuyang particularly emphasizes focusing on the company's core franchises, a term he has used on several occasions.

In 1999, when he was still the CEO of ICS, he likened the company to a 'franchise':

In our business, we almost have a nature of 'franchise'. Anyone needing timely solutions would think not only of crystals but also of silicon products. And in the field of silicon products, they would immediately think of Integrated Circuit Systems (ICS). Our market share in the PC market is very high, thus we effectively become the preferred choice.

Many years later, in 2018, he mentioned the concept of 'franchise' again during an interview with The Wall Street Journal:

The core is to create a very excellent portfolio of product franchises to generate tremendous value... Frankly speaking, we will invest heavily to ensure that we are far ahead of the second or third place in the market.

The metaphor of 'franchise' is very vivid: the best competitive state is the absence of competition.

For example, franchises for fast food and car dealers often maintain a small monopoly in local markets.

In the early growth stage of the semiconductor industry, companies like Motorola and National Semiconductor often launched as many products as possible, venturing into various different fields.

But today's market has become more complex. Designers are more focused on overall system solutions rather than individual customized components, and the market is flooded with various options from abroad.

Chen Fuyang's philosophy is that leading semiconductor companies today must establish and maintain their own franchises to become the first choice for designers when they need system components, creating a "small-scale local monopoly."

When he takes over a new business, he reinforces this franchise as much as possible, focusing on cutting-edge products within the franchise and expanding into new vertical markets and application areas.

When discussing the growth strategy of ICS, he stated:

"We will stick to our core business, which is silicon timing solutions. Our strategy is to expand our application areas and increase our market share in digital consumer and communications markets."

This means cutting out those speculative projects that old-school semiconductor companies were once fond of. If a project does not help the core franchise business, it should be decisively abandoned.

This approach has attracted criticism from several detractors.

Reducing R&D spending or selling non-core business units may have long-term effects, as these projects often take time to yield results. And there must always be a source for the franchise business, right?

Chen Fuyang clearly pointed out that he has invested significant resources in the existing franchise business to maximize the 'value of the cash cow.' Unlike companies like Agilent Technologies, which must feed like a hummingbird to achieve significant growth.

The 'Rebirth' of Agilent Technologies.

Agilent Technologies initially was a very diversified company.

By the end of 2005, the company had five end markets, each accounting for more than 10% of sales. This was the complex business pattern left behind by HP Inc.'s 40 years of diversified operations.

After Chen Fuyang took office, he immediately started to sort out the chaotic situation with his team, transforming it into a company focused on analog mixed-signal and optoelectronic franchise businesses.

In March 2006, they sold the storage business for approximately $0.42 billion to PMC Sierra. In May 2006, they sold the printer ASIC business for approximately $0.25 billion to Marvell.

In December of the same year, they sold the CMOS image sensor business for $53 million to Micron Technology.

One year later, in 2007, they sold the infrared business for 20 million dollars to the **** electronics company Lite-On.

These sales transactions not only raised funds to pay off debts but also reduced the company's number of employees from 6,500 in 2005 to 3,600 in 2008.

However, by 2008, the revenue and profit of NOV Inc did not show significant changes compared to the period before the acquisition.

But the company had repaid about 1 billion dollars in net debt, which was sufficient for KKR and Silver Lake to reintroduce the company to the public market in August 2008, only two years after its privatization.

The two private equity firms gradually sold their shares in the years following the IPO, ultimately achieving a 5-fold ROI.

The results were quite good, with both the capital and operational teams achieving a win-win situation. And this was also an important process for Chen Fuyang'smergers and acquisitions.Global Strategy to become increasingly mature and refined.

The timing for the IPO is very fortunate.

In 2007 and 2008, the release of Apple's iPhone sparked a wave of Smart Phone popularity. Analog Devices successfully seized this trend due to its early technological accumulation in FBAR RF filter.

RF filters are crucial yet little-known Components in mobile phones. They help modems separate data signals from noise, thus saving power and enhancing the user experience.

These filters are more like microelectromechanical systems (MEMS), which are miniature 'tuning forks', rather than NVIDIA's GPUs.

However, they are highly specialized and require the use of unique thin-film technology and non-traditional materials like Gallium Arsenide during manufacturing.

In 2008, Analog Devices acquired Infineon's BAW RF acoustic filter business and related patents for 30 million dollars. In 2010, it was the first to launch RF filters suitable for 4G LTE bands.

LTE triggered a mobile data revolution globally, forcing RF filters to support an increasing number of bands, as well as Wi-Fi and Bluetooth functionalities, significantly increasing their complexity and cost.

The RF filter market size grew from 0.1 billion dollars in 2004 to over 1 billion dollars in 2014, and Analog Devices earned a considerable share from it.

At the same time, Smart Phones have become thinner and more energy-efficient, which has prompted the integration of various discrete components in the RF front-end, including power amplifiers, filters, switches, and antennas (excluding modems and transceivers dominated by Qualcomm).

Therefore, the surge in Smart Phones and LTE brought significant profits to Broadcom in the late 2000s and early 2010s.

However, by 2013, the mobile business accounted for 50% of the company's revenue, raising concerns about over-concentration in the business.

Chen Fuyang and Broadcom began to look for new franchising opportunities.

Broadcom's 'Snake Swallowing Elephant'

In December 2013, Broadcom announced the acquisition of LSI Logic for $6.6 billion.

LSI was founded in 1980 by former Fairchild Semiconductor CEO Wilfred Corrigan, a tough-minded British man. It officially began operations in 1981 and secured its first funding of $6 million.

They collaborated with a Japanese foundry to produce wafers and launched an innovative Master Sliced System to help customers replace whole circuit boards with custom chips.

In March 1982, Don Valentine, founder of Sequoia Capital and a former colleague of Corigan at Fairchild Semiconductor, injected 16 million dollars into LSI.

On May 13, 1983, LSI went public on Nasdaq, calculating based on the closing price on the first day of trading, LSI's Market Cap reached 0.588 billion dollars, which allowed Sequoia Capital.return on investmentto approach 10 times, making a huge profit.

What is more worth noting is that in 1992, Huang Renxun, who was then employed at LSI, resigned to start his own business, and it was Corigan who recommended his close ally Valentine to Huang.

With Corigan's strong endorsement, Huang Renxun's business plan did not move Valentine, allowing him to successfully secure an angel investment of 1 million from Sequoia.

And 22 years later, in 2014, Broadcom, led by Chen Fuyang, acquired LSI, but that is a story for later.

The "two major brothers" of the global semiconductor industry had a miraculous resonance at different points in the growth and life line of LSI.

Corrigan has served as the CEO of the company since founding LSI until 2005.

After Corrigan's retirement, the new CEO of LSI transformed the company into a completely fabless model, starting to develop custom silicon chips for data centers to enhance operational efficiency.

LSI had already established a solid footing in this business through hard disk controller chips.

In 2007, they made a merger deal with Agere Systems for 4 billion dollars. By integrating Agere's business, LSI amassed significant strength in enterprise storage systems, networking, and SSD/HDD storage hardware.

At that time, cloud storage startups like Box and Dropbox were valued at billions of dollars, attracting the attention of Chen Fuyang's team. For LSI, the business had stagnated over the past few years, making a buyout a good outcome.

The situation when Anka High acquired LSI resembled a snake swallowing an elephant.

In 2013, Anka High had only 2.5 billion dollars in revenue and a market cap of about 12 billion dollars. However, they acquired LSI for 6.6 billion dollars, of which only 1 billion came from their own funds.

Their partner Silver Lake invested 1 billion dollars, while the remaining 4.6 billion dollars was financed through loans.

Thus, Chen Fuyang and his team restarted the process of cutting costs and repaying debts. In May 2014, they sold LSI's flash memory solutions (including PCI Express solutions and solid-state drive controller chips) to Seagate for $0.45 billion.

In November 2014, they sold LSI's networking chip division Axia to Intel for $0.65 billion. The division's chips helped Internet Plus-Related service providers and datacenters monitor and manage network traffic.

Acquiring Broadcom, becoming Broadcom.

A year later, Avago achieved a larger-scale transaction, acquiring the historic analog chip company Broadcom.

Avago had attempted to acquire Broadcom at the end of 2014 but gave up due to price disagreements. However, LSI's successful acquisition led to a rise in Avago's stock price, providing them with stronger capital strength.

In April 2016, Chen Fuyang contacted Broadcom's management again, proposed a new quote, and finalized the deal within just a month and a half. The acquisition amount of $37 billion set the record for the largest transaction in the tech industry at that time.

Avago paid a 28% premium for Broadcom, as Broadcom's stock price was at a nine-year high at that time.

Broadcom is a name of great influence in the history of semiconductors.

The company was founded in 1991, focusing on the production of analog system-on-chip products for high-speed communication devices such as cable modems and set-top boxes.

In the 1990s, Broadcom experienced rapid growth alongside the rise of cable operators like Comcast and broadband Internet. Entering the 2000s, Broadcom entered a series of new markets, including enterprise switches and network devices.

Broadcom's acquisition was also a case of a snake swallowing an elephant.

A year before the acquisition, Broadcom's revenue was almost double that of Avago. As part of the deal, Avago agreed to use Broadcom's name and added Broadcom co-founder Henry Samueli to the company's Board of Directors.

This deal was somewhat like a strategic marriage: one side was a rising star, while the other was a declining noble family, impoverished but still bearing a long and prestigious family name and castle.

More than a year later, the new Broadcom acquired a storage networking company, Brocade, for approximately 6 billion USD.

The familiar cycle began again: cut costs, repay debts.

Within a few short years, Broadcom rapidly integrated a large number of high-quality assets. This process was like a large company version of buying a house with a mortgage, repairing it, renting it out, and actively repaying the debt.

Acquisition of Qualcomm failed.

After repeating this strategy several times, Chen Fuyang and Broadcom faced a problem: after acquiring Broadcom and Brocade, it became very difficult to find a large enough target to "shake up the market."

But if you don't take action, you are destined to lose all opportunities.

So, Chen Fuyang headed straight for the "prom queen" Qualcomm.

On November 6, 2017, Broadcom made a $103 billion acquisition offer, but it was immediately rejected by Qualcomm's Board of Directors on the grounds that the offer was too low. Broadcom attempted to contact Qualcomm but was rejected, so they directly launched an attack on Qualcomm shareholders, trying to push the deal through a board change.

In January 2018, Qualcomm submitted an appeal to the Committee on Foreign Investment in the United States (CFIUS) in an attempt to block the acquisition.

CFIUS is responsible for reviewing merger and acquisition transactions involving national security and pointed out their concerns: Broadcom's past practices of cutting research and development spending could weaken Qualcomm's competitiveness against Huawei in the 5G technology field.

In response to CFIUS's review, Broadcom decided to relocate its company registration from Singapore back to the USA.

Subsequently, during the previous term, President Trump held a public meeting with Chen Fuyang to discuss the re-registration matter. However, the Trump administration ultimately halted the acquisition.

Looking back, Qualcomm's Market Cap has now exceeded Broadcom's Quote at that time, largely due to the explosion of technology demand during the COVID-19 pandemic.

However, with a Market Cap of less than 180 billion USD compared to Broadcom's strong growth in recent years, it seems that Qualcomm's Shareholders may have some regret if a stock merger had taken place back then.

Moreover, for Qualcomm, an unavoidable reality is that Huawei still dominates the 5G sector.

It is said that when Alexander the Great reached the Indus River, he lamented that there were no more lands to conquer. After being rejected by Qualcomm, Broadcom indeed found it challenging to find suitable large companies to acquire in the silicon chip field.

Completely catching the wave of AI and experiencing tremendous wealth.

Chen Fuyang then turned his attention to Software companies, including CA Technologies, Symantec, and Vmware.

Adopting the same strategy: digging into the franchise business, cutting costs, and repaying the debt incurred from the acquisition.

However, before the outbreak of ChatGPT, people were always questioning: What is the next step? What else can lead them to achieve greater growth?

The answer has actually been hidden within them.

When Broadcom acquired LSI in 2013, it also acquired a small custom silicon chip design division that helped external customers design and produce their own chips for data centers.

When Google began developing their first chip—the Tensor Processing Unit (TPU)—they did not require a large number of chips. So in 2016, they hired Broadcom to assist in designing and producing this chip.

The reason Google did this is simple, because custom silicon chip teams are costly: not only do you have to pay high salaries for top talent, but also huge fees for EDA tools and intellectual property.

In cases where chip volume requirements are not so high, hiring the Broadcom team to design to specifications is more economical, and they can also provide value-added services such as testing and packaging.

In 2016, when the TPU partnership began, the custom silicon chip business was quite small for both parties. That year, Broadcom's TPU revenue was estimated to be only about 50 million dollars.

But over time, this business continued to grow. By 2020, Broadcom's TPU revenue was estimated to have reached 0.75 billion dollars.

In November 2022, the explosive success of ChatGPT ignited the current AI craze, with all companies, from startups to tech giants, joining the generative AI race.

Many companies encountered computing bottlenecks because no one, including OpenAI itself, could have predicted ChatGPT's immense success.

Google realized that its TPU dedicated chips gave it a significant competitive advantage in computing power over companies like Microsoft and Oracle, and thus began purchasing more TPUs.

This undoubtedly greatly benefited Broadcom.

According to previous predictions by Semi Analysis, Google's payments to Broadcom for TPUs are expected to surge significantly in 2024, reaching around $8.5 billion.

This does not include revenue from collaborations between Broadcom and Meta or other tech giants like Microsoft.

However, NVIDIA will not allow Broadcom to enjoy all of this alone.

In February 2024, Reuters reported that NVIDIA is forming its own AI chip design department, planning to use its intellectual property and expertise to prevent customers from developing alternatives, thus protecting its lucrative H200 and B100 AI accelerator markets.

写在最后

So, what exactly is Broadcom?

The company has a range of powerful technology franchise businesses, acquiring new businesses, streamlining and optimizing, focusing on them, and then using the profitability of these businesses to acquire more new franchise businesses.

Their growth basically relies on acquisitions.

This time, one of their franchise businesses has just hit the core of the AI craze. This does not mean they will not go all out to stay there, just as they did in the mobile technology and cloud computing booms.

Believe they will invest at all costs to maintain and expand their leading position in this "gold rush."

Editor/ping