由于特朗普在美国总统大选中获胜,以及强劲的经济数据促使交易商降低了对美联储明年降息次数的预期,美元今年已经飙升,有望创下自2015年以来的最大涨幅。

由于特朗普在美国总统大选中获胜,以及强劲的经济数据促使交易商降低了对美联储明年降息次数的预期,美元今年已经飙升,有望创下自2015年以来的最大涨幅。Multiple selling strategists predict that the US dollar will peak as early as the middle of next year and then begin to decline, potentially falling by 6% by the end of next year.

Due to the policies of the newly elected president of the USA, Trump, and the Federal Reserve's interest rate cuts, there may be pressure on the USD in the second half of 2025, leading Wall Street to become dissatisfied with the dollar.

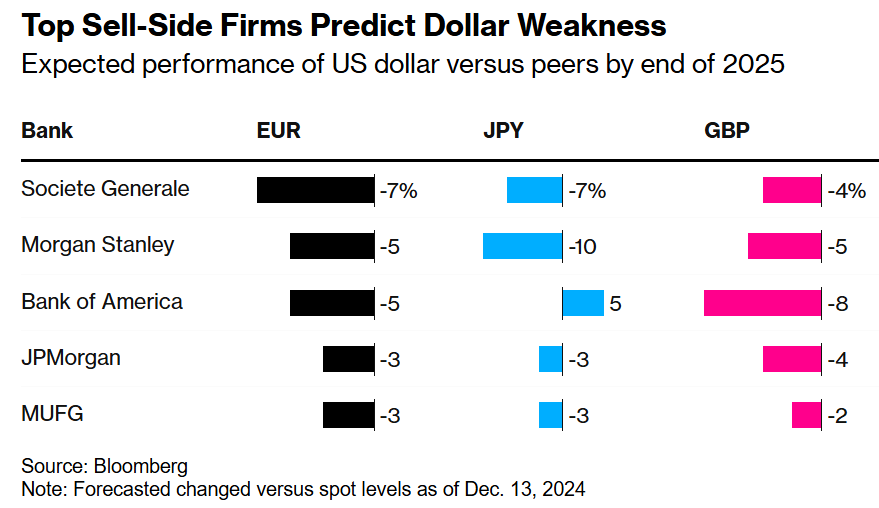

From Morgan Stanley to JPMorgan, about six sell-side strategists now predict that the USD will peak as early as mid-next year and then begin to decline. Industrial Bank believes that the ICE USD Index will drop by 6% by the end of next year.

Due to Trump's victory in the US presidential election and strong economic data encouraging traders to lower their expectations for the Federal Reserve's interest rate cuts next year, the dollar has soared this year, poised to record its biggest increase since 2015.

Due to Trump's victory in the US presidential election and strong economic data encouraging traders to lower their expectations for the Federal Reserve's interest rate cuts next year, the dollar has soared this year, poised to record its biggest increase since 2015.

Kit Juckes, the currency strategy director at Société Générale, expressed that the strength of the USD is "disgusting." "We are driving up the price of an asset that is unsustainable in the long term."

The Bloomberg USD Spot Index has risen about 6.3% so far this year, with most of the increase occurring before and after Election Day in early November.

Trump's tariff and tax reduction policies will stimulate inflation and complicate the Federal Reserve's task of lowering interest rates in the coming months. This expectation has fueled the rise of the dollar, encouraging global investors to shift their funds to the USA.

Analysts like Matthew Hornbach and James Lord from Morgan Stanley believe these threats will boost the dollar, but they wrote that by this time next year, the dollar is expected to eventually fall below its current levels. They added that a combination of decreasing real interest rates in the USA and rising risk appetite will make the dollar the most bearish currency.

Currently, Trump's hawkish rhetoric on trade issues is escalating. Recently, he promised to impose a 25% tariff on goods from Mexico and Canada related to immigration and drugs, causing the exchange rates of the Mexican peso and Canadian dollar to decline. Earlier this month, Trump mocked some emerging economies for challenging the dollar's status as the world's primary currency.

The recent strength of the dollar has led to weakness in non-dollar currencies. After the US election in November last year, the euro fell to a two-year low, nearing parity. The MSCI Inc. Emerging Markets Currency Index is currently at its lowest level in four months.

Citigroup strategists led by Daniel Tobon believe that any resolution to potential trade wars by Trump’s second-term administration will disappoint those bullish on the dollar. Many dollar bulls believe Trump's stance on trade issues inherently supports the dollar, thus establishing long positions.

Data compiled by Bloomberg based on information from the Commodity Futures Trading Commission for the week ending December 10 shows that speculative, non-commercial traders still hold about $24 billion in dollar long positions, close to the highest level since May. This group has remained bullish on the dollar since mid-October, before the election.

Imminent threat.

When it comes to the dollar's trajectory during President Trump's tenure, history can provide some guidance. Eight years ago, after Trump's election, the dollar soared, but as the US economy lost momentum and the European economy rebounded, the Bloomberg Dollar Index recorded its largest annual decline ever in 2017.

Derek Halpenny, an Analyst at MUFG, stated that Wall Street believes the decline will not be significant, but the dollar may peak in the first half of 2025.

Compared to the euphoric rise of the dollar after Trump's victory in November, even the options market has somewhat lowered the bullish expectations for the dollar next year.

The Bloomberg USD benchmark one-year risk reversal index was approximately 1% this week, down from a four-month high about a month ago, indicating that traders still anticipate a rise in the USD, but bullish sentiment has stagnated.

Sophia Drossos, a strategist and economist at Point72 Asset Management, believes that the dollar has already priced in too many bullish factors, and economic growth anywhere outside the USA, especially in Europe, will weaken the dollar's exchange rates against other currencies. The European Central Bank and the Bank of England are cutting interest rates to help alleviate economic downturn risks. Drossos stated, "The foundation for a strong global economy next year is solid."

Top currency strategists expect that the biggest support for the dollar in recent months—the Federal Reserve—will further become a burden by 2025. Morgan Stanley's rate strategists believe that the decline in US yields is expected to be faster than in other parts of the world next year, which will compress the long-standing favorable interest rate differentials for the dollar.

Other experts believe that if Trump's trade policies are implemented, the dollar will face further strengthening risks because, theoretically, tariffs will cause the prices of any imported goods used by US manufacturers to skyrocket.

Barry Eichengreen, an economist at the University of California, Berkeley, who has spent decades studying the global monetary system, said, "If tariffs make Steel and Aluminum more expensive, this will create negative supply shocks for the land Autos industry that uses these imported inputs."

In addition, there are threats from expanding budget deficits and increasing term premiums on US Bonds, which measure the expected risk of holding long-term Treasury securities.

JPMorgan Analyst Meera Chandan, who is the Co-Head of Global Forex Strategy, wrote in the 2025 Outlook: "When the Federal Reserve indeed engages in substantial easing, and the USD loses its relative yield/growth advantage, the weakness of the dollar could be extraordinary."

Editor/lambor