① With the Bank of Canada and several European central banks taking the lead last week in ushering in the year-end interest rate cut tide, a more intensive "Central Bank Super Week" will follow this week; ② Led by the G10 central banks such as the Federal Reserve, the Bank of Japan, and the Bank of England, a rare event will occur this week where as many as 25 central banks will hold meetings in the same week; ③ The economies of these central banks account for nearly two-fifths of the global economy...

Financial Associated Press, December 16 (Editor: Xiao Xiang) With the Bank of Canada and several European central banks taking the lead last week in ushering in the year-end interest rate cut tide, a more intensive "Central Bank Super Week" will follow this week: Led by the G10 central banks such as the Federal Reserve, the Bank of Japan, and the Bank of England, a rare event will occur this week where as many as 25 central banks will hold meetings in the same week, and the economies of these central banks account for nearly two-fifths of the global economy...

Undoubtedly, in the final "Central Bank Super Week" of 2024, these meetings are expected to attract the attention of all investors. Especially in the Forex and CSI Commodity Equity Index markets, where trading occurs around the clock, volatility may erupt quickly, resulting in a series of storms within just a few hours as some key central bank decisions are announced.

The following are the specific release dates for the interest rate decisions of these 25 central banks (based on local time):

The following are the specific release dates for the interest rate decisions of these 25 central banks (based on local time):

Monday (December 16): Bank of Pakistan;

Tuesday (December 17): Bank of Morocco, Hungarian central bank, Chilean central bank;

Wednesday (December 18): Bank of Thailand, Bank of Indonesia, National Bank of Georgia, Bank of Albania, National Bank of North Macedonia, Central Bank of Azerbaijan, Federal Reserve;

Thursday (December 19): Bank of Japan, Sveriges Riksbank, Norwegian central bank, Bangko Sentral ng Pilipinas, National Bank of Moldova, Bank of England, Czech National Bank, Bank of Mexico, Central Bank of Paraguay, Central Bank of Costa Rica;

On Friday (December 20): Central Banks of Mongolia, Russia, Jamaica, and Colombia.

Among these central banks, there are as many as five G10 central banks (the ones bolded above) — accounting for half of the jurisdictions of the 10 major currencies with the largest global trading volumes.

Many analysts have stated that as central bank policymakers weigh different risks for the upcoming year, the ultimate outcome of the monetary policy meetings will likely highlight: the momentum of Global easing policies appears to be increasingly unbalanced. In fact, among these 25 central banks, the three most closely watched — the Federal Reserve, the Bank of England, and the Bank of Japan — may take completely different approaches this week:

The Federal Reserve may cut interest rates this week, the Bank of England may remain unchanged, while the "independent" Bank of Japan will weigh whether to raise rates this month or next month!

This week, the easing camp is "expected to lower rates".

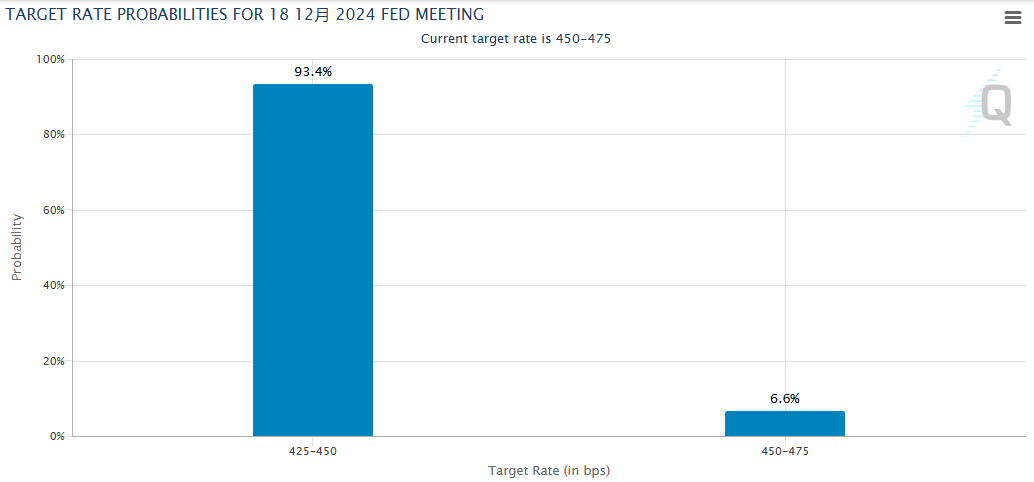

Without a doubt, the Federal Reserve will be the most prominent central bank in this last "Central Bank Super Week" of 2024. Currently, industry expectations generally foresee that the Federal Reserve is likely to achieve a "three consecutive drops" in interest rates this week.

Traders in the interest rates futures market predict a 93% probability that the Federal Reserve will lower rates by 25 basis points at the meeting on December 17-18. However, due to the recent strengthening of US economic data, the risk of the Federal Reserve pausing rate cuts in early 2025 has increased. Powell's remarks at the post-meeting press conference and the latest dot plot forecast will be crucial.

In addition to the Federal Reserve, another G10 central bank expected to lower rates this week is the Swedish central bank. Most economists expect Swedish officials to cut the benchmark rate by 25 basis points this week, following a more gradual approach after last month's 50 basis-point cut. Although Sweden's core inflation rate has recently returned to a six-month high, this is unlikely to prevent the Swedish central bank from taking action to cut rates.

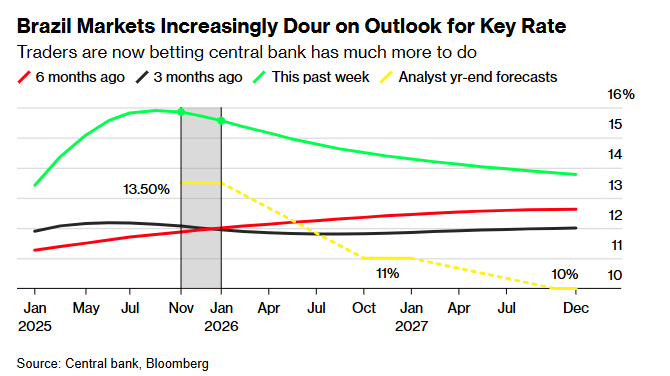

In Emerging Markets, although the Central Bank of Brazil has raised interest rates multiple times (and the rate hikes have been increasing), some of its neighboring countries are still in a loosening cycle. This week, the central banks of Chile, Mexico, and Colombia are all expected to cut interest rates.

Additionally, in Asia, the Central Bank of Pakistan is expected to start cutting interest rates this week as inflation has eased; the central banks of Indonesia and the Philippines are also expected to cut rates by 25 basis points each.

The camp expected to 'hold steady' this week.

This week will apparently see a considerable number of central banks presenting the 'last cut of the year', but there are also many members of the loosening camp that are taking a wait-and-see attitude.

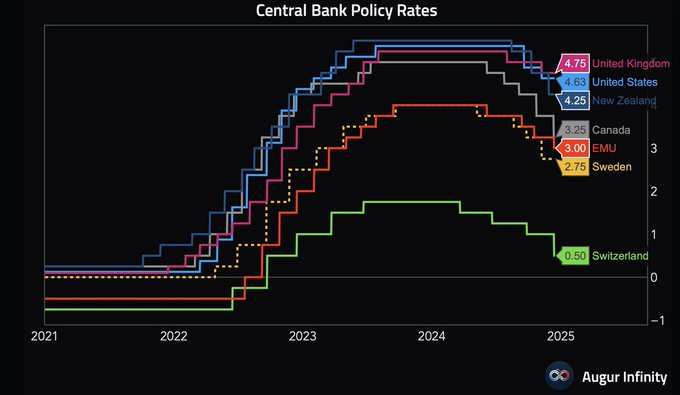

The Bank of the United Kingdom is likely to be the main representative of the 'hold steady' camp. The swap market currently predicts that the Bank of the United Kingdom will almost certainly maintain interest rates at the final monetary policy meeting of the year, adhering to a cautious loosening policy and continuing to proceed down the slow lane for interest rate cuts. The Bank of the United Kingdom has only cut rates twice so far in 2024, which makes the British Pound the only G10 currency that has not depreciated against the US dollar during the year.

In neighboring Norway, the central bank's policymakers are also expected to maintain interest rates at 4.5%. Norway's core inflation ended a year-long trend of slowing last month, mainly driven by domestic commodities, and a key survey by the central bank showed that the outlook for businesses in this energy-rich country appears slightly strong. The Norwegian central bank is likely to confirm its first rate cut of this round of loosening cycle only next year.

Other European central banks expected to hold steady this week also include the Central Bank of Hungary and the Central Bank of the Czech Republic. Due to accelerated inflation and the forint remaining close to a two-year low, the Central Bank of Hungary may keep borrowing costs unchanged. Meanwhile, Czech policymakers are currently considering stopping the loosening policy.

Additionally, the Central Bank of Thailand is also expected to maintain the benchmark interest rate at 2.25% on Wednesday.

Tightening camp.

Finally, under the sweeping wave of global overall easing, there are also some central banks going against the tide—these few central banks are currently in a tightening cycle.

The Bank of Japan, which is still exploring when to further raise interest rates, will undoubtedly be the biggest focus of this "central bank super week" aside from the Federal Reserve. Of course, from the current market expectations, it seems that the Bank of Japan is more likely to take further tightening actions early next year.

According to Japanese media citing informed sources, the Bank of Japan is currently unlikely to raise interest rates at this week's meeting, unless there is a significant risk of yen depreciation, which would drive up import prices. As the December meeting approaches, there is increasing concern that the profitability of Japanese companies, especially exporters, will worsen, following President-elect Trump's promise to raise tariffs.

In contrast to the Bank of Japan, which may not be in a hurry to raise interest rates this week, the Central Bank of Russia, facing significant pressure from the sharp depreciation of the ruble, is likely to raise interest rates again this week. Industry insiders expect that the Central Bank of Russia will raise rates by up to 200 basis points this Friday, reaching a record 23%, as previous data showed that consumer price pressures in the country were still above the 4% target.

Get a sneak peek at important financial events, discover investment opportunities early! Open futubull> Market> USA Stock>Financial Calendar/Selected macroeconomic data, seize the investment opportunities first!

Get a sneak peek at important financial events, discover investment opportunities early! Open futubull> Market> USA Stock>Financial Calendar/Selected macroeconomic data, seize the investment opportunities first!

Editor/lambor