整体看,不论是纵向对比历史,还是横向对比其他资产,

整体看,不论是纵向对比历史,还是横向对比其他资产,Source: China International Capital Corporation's Insights

Authors: Liu Gang, Wang Zilin

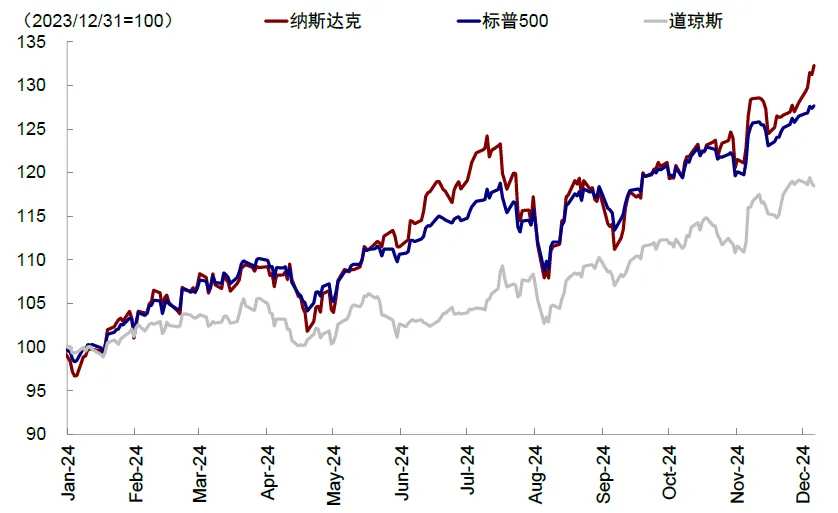

Last week, the Nasdaq index first broke through the 0.02 million mark. Although concerns about high valuations and potential economic stagflation following Trump's presidency remain, the U.S. stock market has continued to surge after the Federal Reserve cut interest rates in September, especially following the November elections, with the three major indices repeatedly hitting new highs. Although the aforementioned concerns have not reversed the upward trend of the U.S. stock market, they are indeed increasing as the market continuously reaches new highs. So, at the current position, how high are the valuations of the U.S. stock market? What level of valuation can the current growth and liquidity environment support? How should the valuation issues of the U.S. stock market be viewed? To address this, we will sort the current valuation situation of the U.S. stock market from four perspectives: vertically comparing historical levels, horizontally comparing with other assets, internally breaking down sectors and industries, and dynamically considering the interest rate environment through a multidimensional segmentation of indicators.

Chart: The three major indices of the U.S. stock market continuously set new highs.

Overall, whether compared vertically to history or horizontally to other assets, it is undoubtedly evident that U.S. stock market valuations are relatively high, even appearing "extreme." However, the above perspectives are merely static thinking that assumes historical trends and relationships with other markets are generally stable and subject to mean reversion. If dynamic considerations of the interest rate and growth environment are taken into account, especially regarding the relative changes in cost and return, the current U.S. stock market valuations are not as "extreme" as they seem, and may even be experiencing a trend change; for example, the earnings contribution from high-valued leaders and the Nasdaq is higher than that from low-valued price sectors. But in the short term, the room for valuation expansion is limited, and earnings are the main driver of market space. In the baseline scenario, we estimate the earnings growth rate of the U.S. stock market to be 10% in 2025, corresponding to an S&P 500 Index level of 6300 to 6400.

Overall, whether compared vertically to history or horizontally to other assets, it is undoubtedly evident that U.S. stock market valuations are relatively high, even appearing "extreme." However, the above perspectives are merely static thinking that assumes historical trends and relationships with other markets are generally stable and subject to mean reversion. If dynamic considerations of the interest rate and growth environment are taken into account, especially regarding the relative changes in cost and return, the current U.S. stock market valuations are not as "extreme" as they seem, and may even be experiencing a trend change; for example, the earnings contribution from high-valued leaders and the Nasdaq is higher than that from low-valued price sectors. But in the short term, the room for valuation expansion is limited, and earnings are the main driver of market space. In the baseline scenario, we estimate the earnings growth rate of the U.S. stock market to be 10% in 2025, corresponding to an S&P 500 Index level of 6300 to 6400.

1. Vertical comparison of historical levels: All dimensions are significantly above the average.

By vertically comparing the valuation levels of the major indices of the U.S. stock market, we find that at the current valuation level, it is significantly higher than the average, for different indices, from different indicators, and in different time period stages. Specifically:

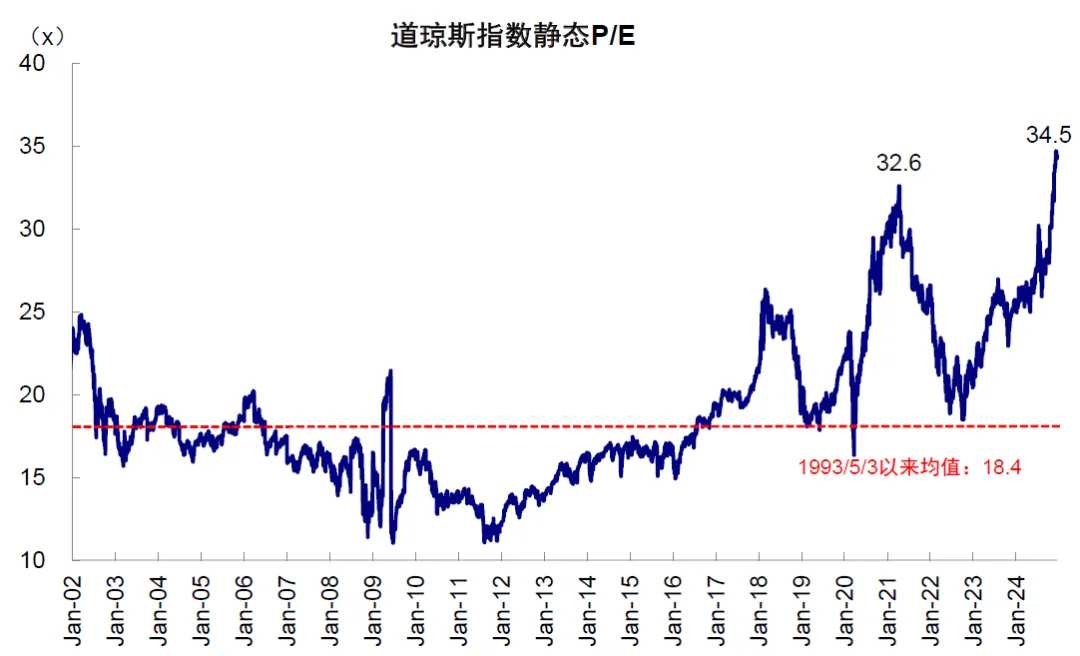

► 从静态估值看,当前标普500静态P/E 27.2倍(前高2021/4/29,32.9倍),远高于1954年以来16.9倍的均值;即使对比1990 年以来更高的估值阶段(均值20倍),目前水平也不便宜,当前估值为1990年以来均值以上1.6倍标准差,处于91%分位。纳斯达克当前静态P/E为47.8倍(前高2020/12/28,81.4倍),高于2001年以来均值1倍标准差,处于90%分位。道琼斯当前静态P/E为34.5倍(前高2021/4/11,32.6倍),高于1993年来均值3.1倍标准差,处于99%分位。不过,静态估值的局限性在于未考虑市场未来的盈利预期,在增长前景向好时存在向上偏误,因此我们进一步考虑动态估值。

图表:纳斯达克指数当前静态P/E为47.8倍

图表:道琼斯指数当前静态P/E为34.5倍

图表:标普500指数当前静态P/E为27.3倍

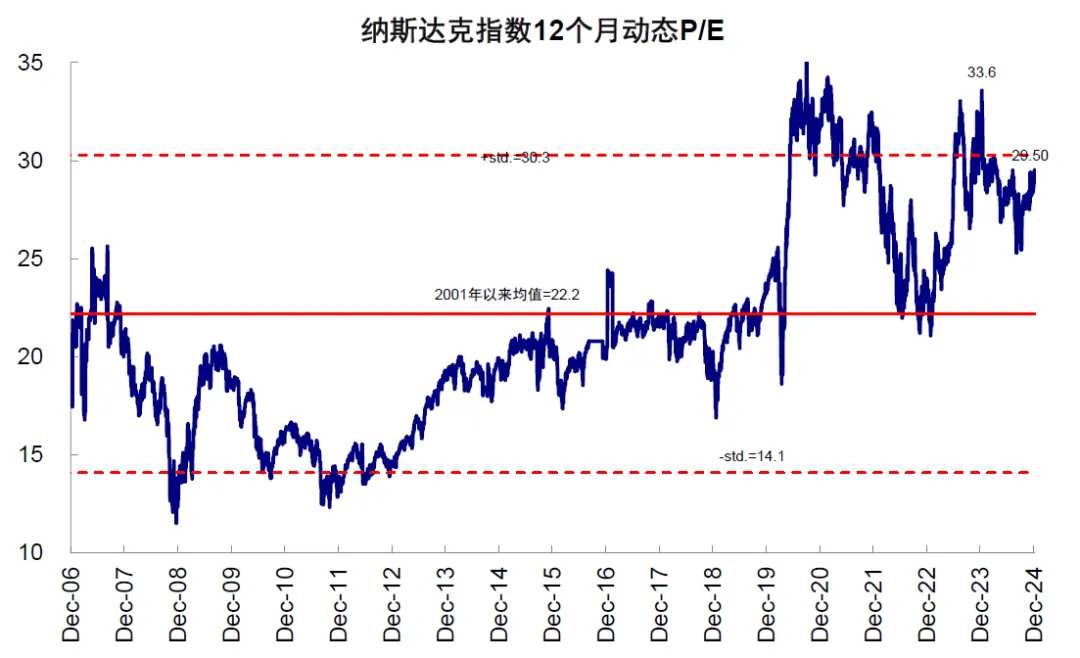

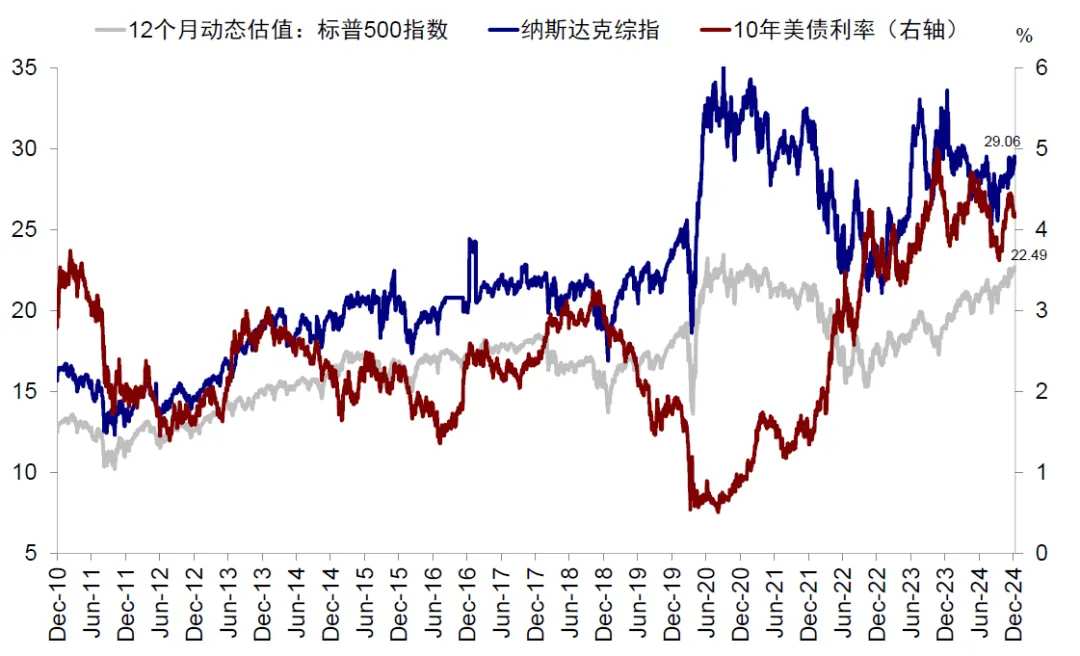

► 从动态估值看,当前标普500动态P/E 22.7倍(前高2020/9/2,23.4倍),同样高于1990年以来16.6倍的均值1.8倍标准差,处于94%的历史分位。此外,道琼斯、纳斯达克、MAAMNG(科技龙头股包括META、苹果、亚马逊、微软、英伟达、谷歌)动态估值(21.2倍、29.5倍、31.4倍 vs. 前高2020/6/8 22.7倍、2023/12/13 33.6倍、2020/8/25 39.6倍)也均已经高于其可得的历史均值水平(16倍、14.8 倍、24.5倍),分别处于95%、89%和84%分位,这表明即便考虑其未来盈利预期,美股估值也不便宜。

Chart: The current dynamic PE of the S&P 500 is 22.7 times, higher than the historical mean by one standard deviation.

Chart: The current dynamic PE of leading Technology stocks is 31.5 times, higher than the historical mean.

Chart: The current dynamic PE of the Dow Jones Industrial Average is 21.2 times, higher than the historical mean.

Chart: The current dynamic PE of the Nasdaq is 29.5 times, higher than the historical mean.

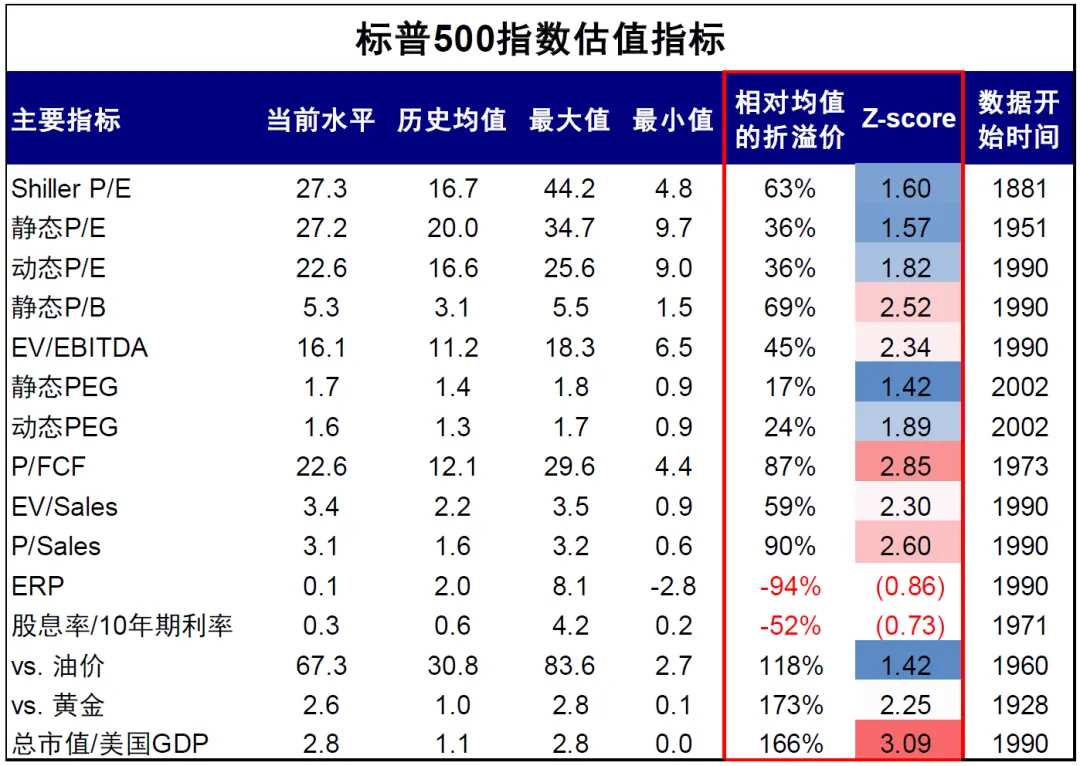

► From other indicators such as P/B, PEG, EV/EBITDA, P/FCF, and P/Sales, the valuation level of the S&P 500 is also higher than the historical average over different time periods, especially for static valuation indicators such as static P/B, EV/EBITDA, and P/FCF, where the deviation from the average has exceeded 2 standard deviations (P/FCF is the highest, exceeding the average by 2.9 standard deviations; static P/B follows, exceeding the average by 2.5 standard deviations). However, considering the dynamic forecast of future earnings and growth, the PEG is also above the average, but the degree of deviation is small, ranging from 1.4 to 1.8 standard deviations.

Chart: Comparison of various valuation indicators for the S&P 500 Index

It should be noted that although the above indicators show that the current valuation is significantly higher than the historical average, the vertical comparison with its historical level implies the assumption of mean reversion in valuation. However, the internal and external economic environments, interest rate environments, and industry trends differ greatly at different times. Therefore, simply comparing macros and market environments is not rigorous and can be misleading. Thus, while it should not be completely trusted, it also shouldn't be disregarded, as it serves more as a reference. Furthermore, high valuations do not necessarily have to be digested through a sharp decline in asset prices; continuous improvement in earnings can also lead to a marginal decline in valuation, such as the upward revision of the MAAMNG Index's earnings expectations in the first half of this year, with dynamic valuations falling below the historical average plus 1 standard deviation.

II. Horizontal comparison with other assets: U.S. stocks are also not cheap.

If the vertical comparison with history uses historical experience as a "reference frame" with mean reversion as a fundamental assumption, then the horizontal comparison with other assets assumes a basic stability in the relationship between the two. A closer examination reveals significant issues with this comparison method, but it does not prevent us from using it as a reference. Specifically, consider:

► Comparing the deviation in global market valuations: Among major global markets, U.S. stocks (MSCI U.S. Index) currently have a valuation (12-month dynamic P/E) that deviates significantly above their historical average (z-score), exceeding the average by 1 standard deviation. In contrast, valuations in Europe, Hong Kong, overseas Chinese stocks, BRICS countries, and South Korea remain below their historical averages.

Chart: Current U.S. stock market valuation levels are above one standard deviation relative to their historical averages.

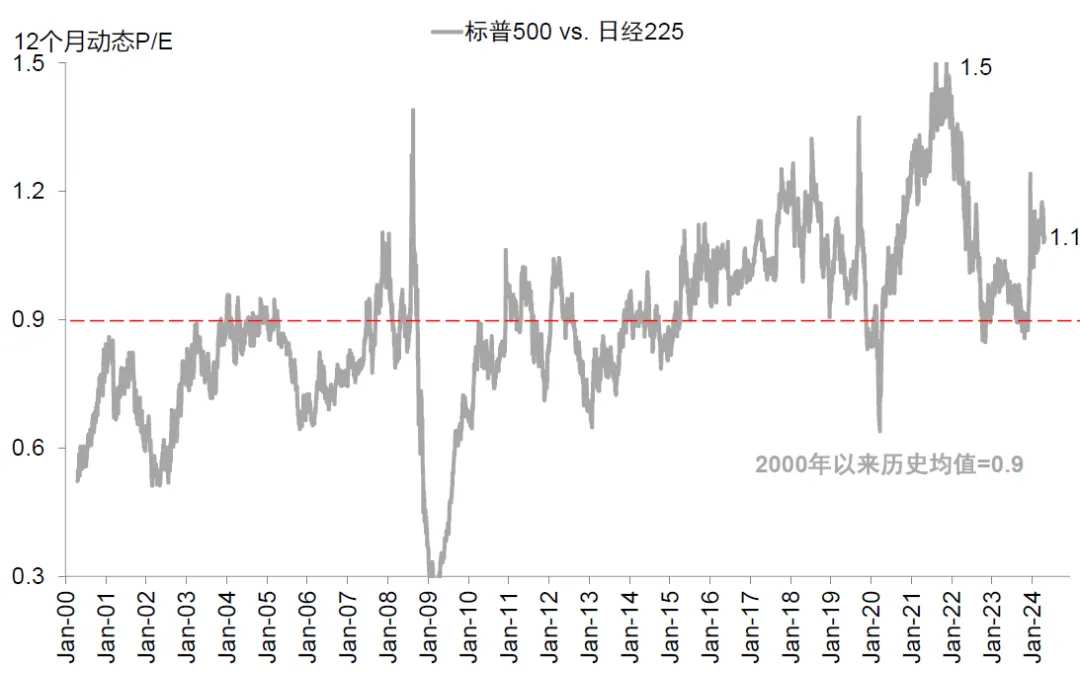

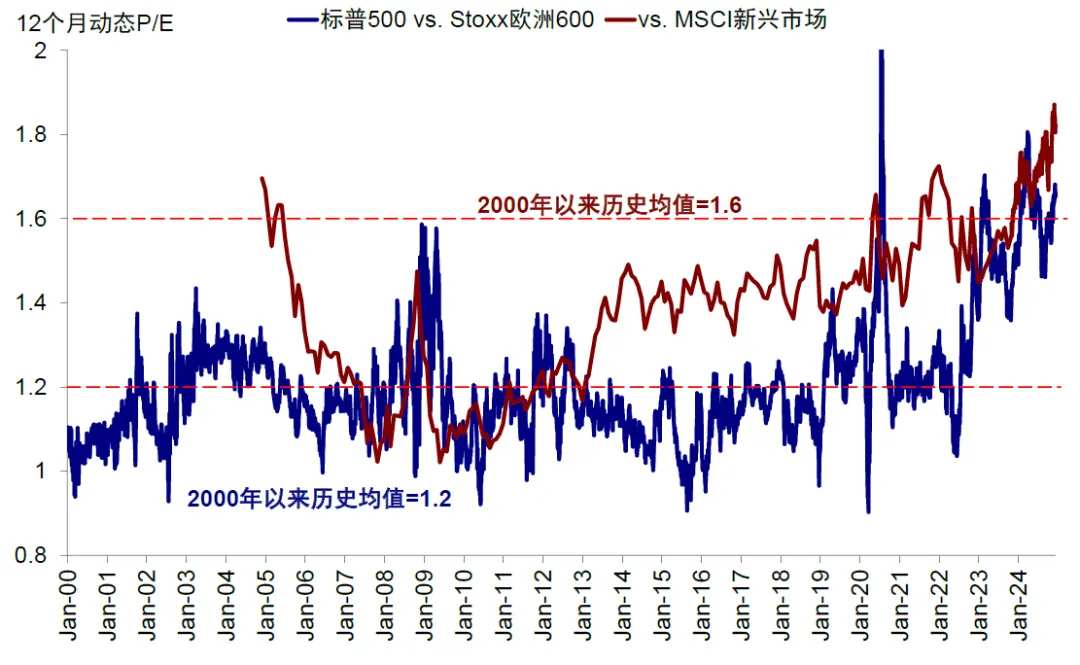

► Comparing the premium and discount of other markets: using Europe, Japan, and Emerging Markets as benchmarks, it is found that the current valuation of U.S. stocks (S&P 500) has premiums of 1.09, 1.65, and 1.82 times compared to the Nikkei 225, Europe Stoxx 600, and MSCI Emerging Markets respectively, all significantly higher than the average premium since 2000 (0.9, 1.2, and 1.6 times respectively). In other words, the degree of overvaluation of U.S. stocks relative to Japan, Europe, and Emerging Markets has also surpassed historical levels, though it remains below the previous peaks of premiums over the Nikkei 225 and Europe Stoxx 600 (1.5 times on November 17, 2021, and 1.8 times on March 28, 2024).

Chart: Using the Japanese market as a benchmark, the valuation of the U.S. stock market is already clearly high.

Chart: Compared to Europe and Emerging Markets' valuations and considering historical premium levels, the relative valuation of U.S. stocks is already significantly high.

► Bonds: The relative strength and weakness of stock and bond valuations can be illustrated by comparing dividend yields and bond yields. Currently, the 12-month dynamic dividend yield of the S&P 500 Index (1.24%) is less than one-third of the U.S. 10-Year Treasury Notes Yield (4.27%), with a dividend yield/bond yield ratio of 0.3 times, the lowest historical level since 2001, only half of the previous low point (October 3, 2018, 0.6 times).

Chart: The current 12-month dynamic dividend yield of the S&P 500 Index is significantly lower than the U.S. 10-Year Treasury Notes Yield.

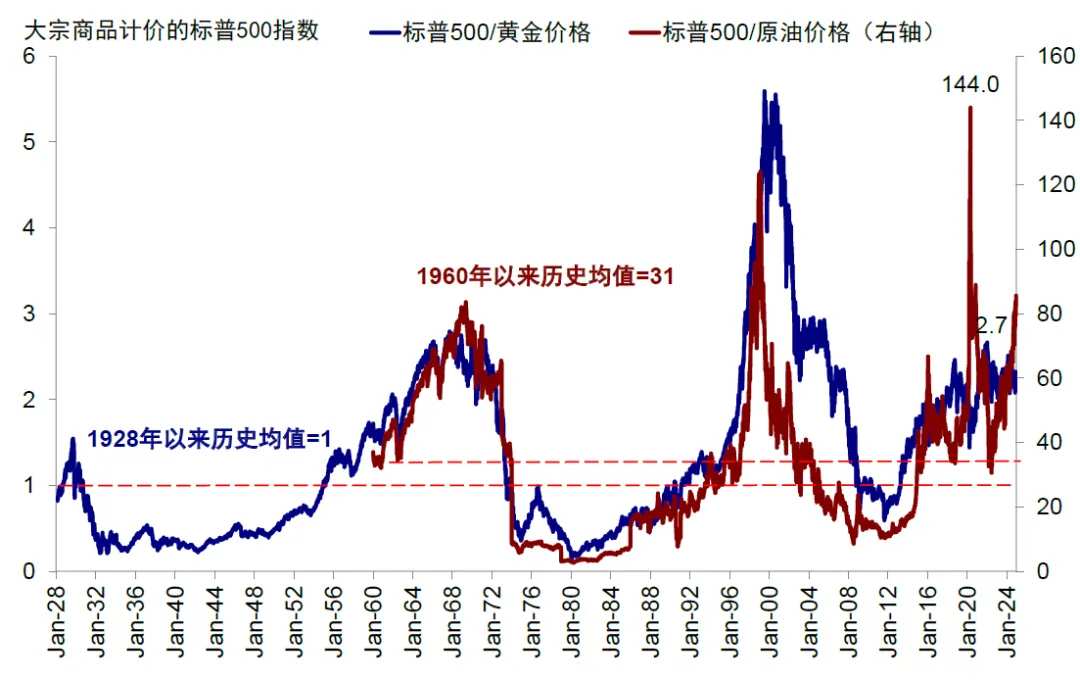

► Gold and Oil Prices: Compared to the CSI Commodity Equity Index, priced in Crude Oil Product and Gold respectively, the current S&P 500 Index level is 67 times the Brent oil price and 2.6 times the gold price, lower than previous highs (144 times the Brent oil price on April 27, 2020, and 2.7 times the gold price on January 3, 2022). Although there is a gap compared to historical extremes, they are both above the average levels of 31 times and 1 time since 1960 and 1928.

Chart: In terms of pricing in Crude Oil Product and Gold, U.S. stocks appear to be overvalued.

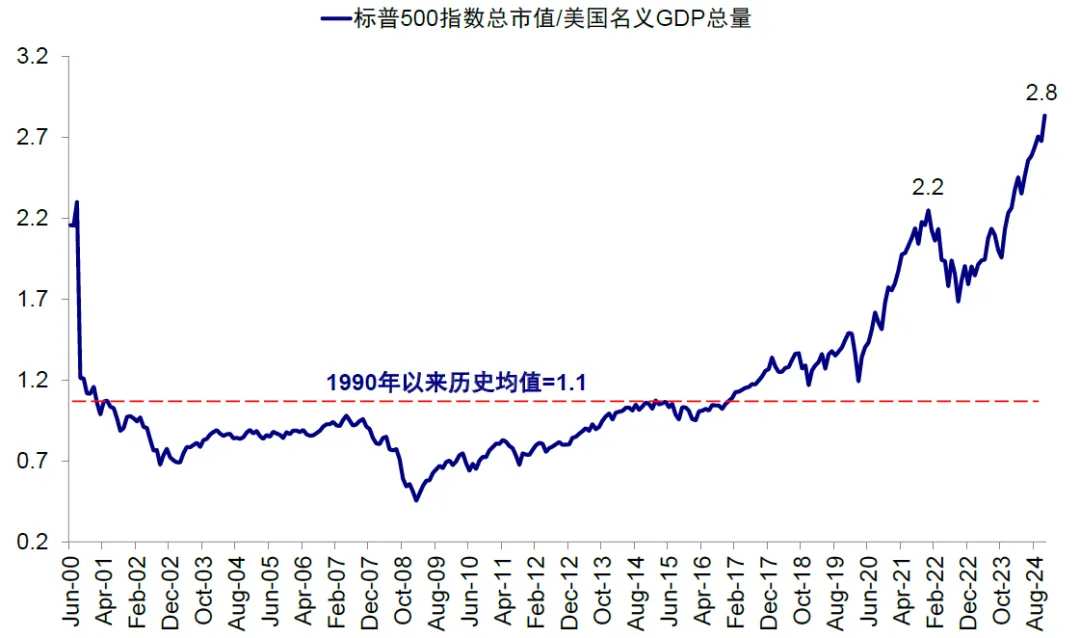

► Economic Scale: Comparing the Market Cap of the S&P 500 to U.S. nominal GDP, or the degree of securitization, this ratio is currently 2.8, the highest since 2000, exceeding the previous high (2.2 times on December 31, 2021). The average since 2000 has only been 1.1 times.

Chart: Total Market Cap compared to U.S. GDP, U.S. stocks also appear to be overvalued.

The limitations of horizontal comparisons with other assets similarly assume that the relative valuation levels among different assets are 'mean reverting,' without considering changes in the paradigms of the strength relationships between different markets and assets. Over the past three years since the pandemic, the 'three macro pillars' that the USA has 'accidentally' formed: large fiscal policy (post-pandemic fiscal stimulus), technological innovation (AI Industry Chain), and global fund rebalancing (Russia-Ukraine situation and China’s economy), have created a continuous and mutual reinforcement mechanism supporting U.S. growth and the U.S. stock market. This has also widened the gap between the USA and non-U.S. assets, as evidenced by the sustained capital inflows and a stronger dollar over the past three years. This situation bears many similarities to the 'Reagan Cycle' 40 years ago, during which the dollar doubled from 1981 to 1985 (from 80 to 160). Therefore, this trend change is something that simple historical levels cannot capture ("2025 Outlook: The Reopening of the Credit Cycle").

III. Internal Structure of U.S. Stocks: There is a clear concentration effect at the top, but high valuations also have earnings support.

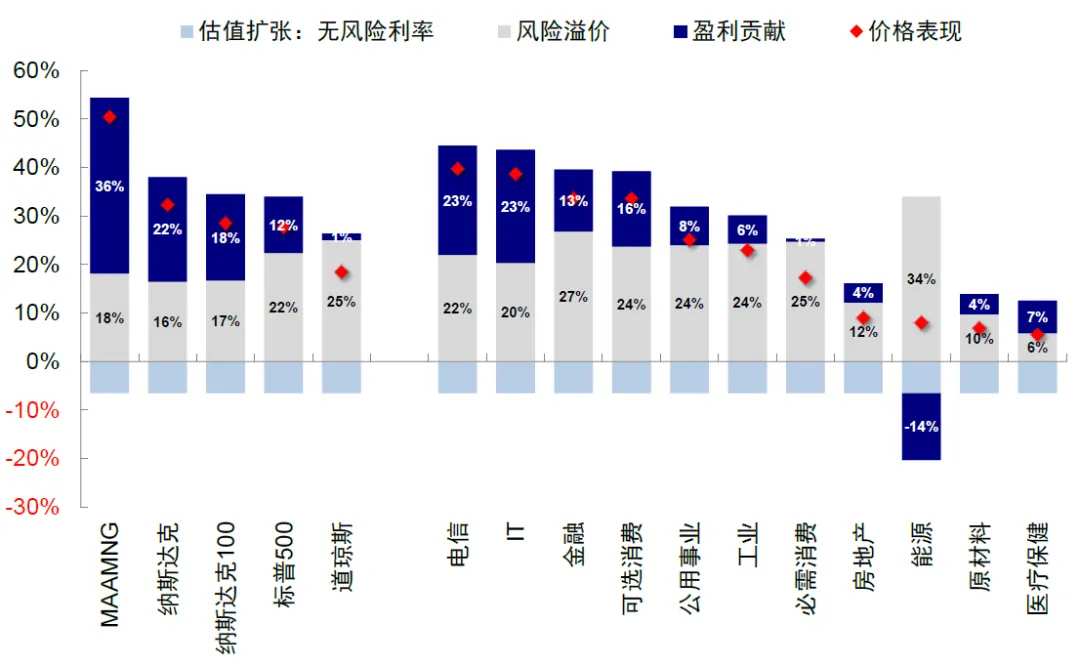

From the perspective of valuation distribution within U.S. stocks, most sectors have valuations that exceed historical mean levels by nearly one standard deviation, especially in growth-oriented sectors where valuations are even higher, and there is a significant concentration effect on Market Cap at the top. However, high valuation sectors have stronger earnings support than low valuation sectors. Specifically,

► Different Styles: From a dynamic valuation perspective, the Nasdaq Index and MAAMNG Index represent growth styles with valuations of 29.5 times and 31.4 times, respectively, while the S&P 500 Index is at 22.6 times and the value-oriented Dow Jones is at 21.2 times.

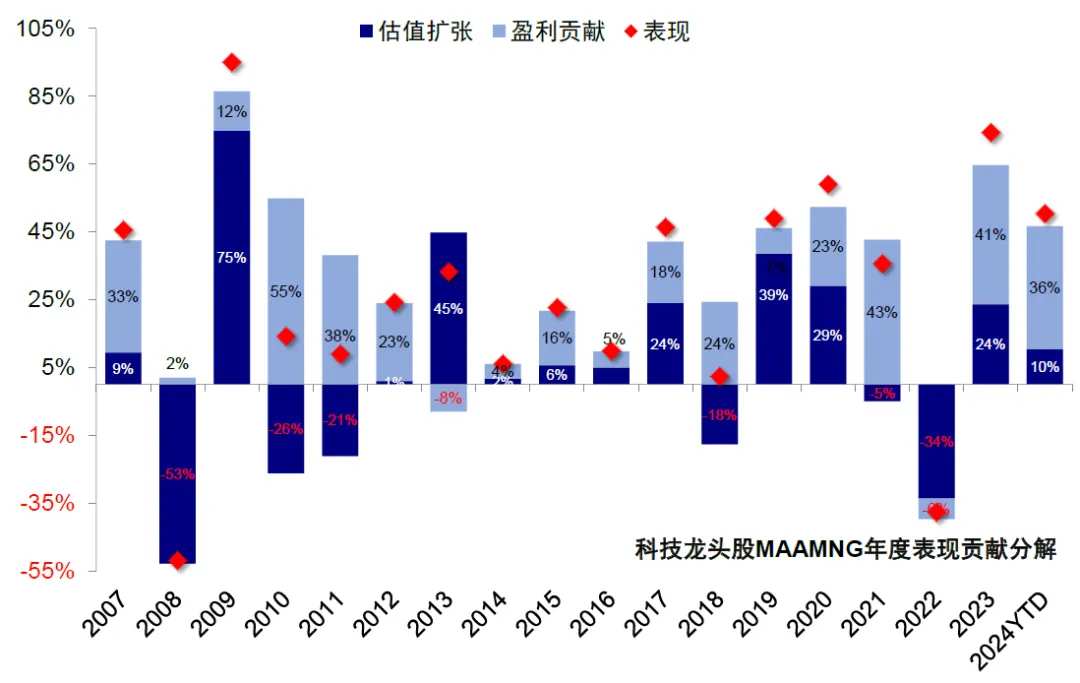

Chart: Looking at different time periods, the most significant valuation expansion this year occurred after September.

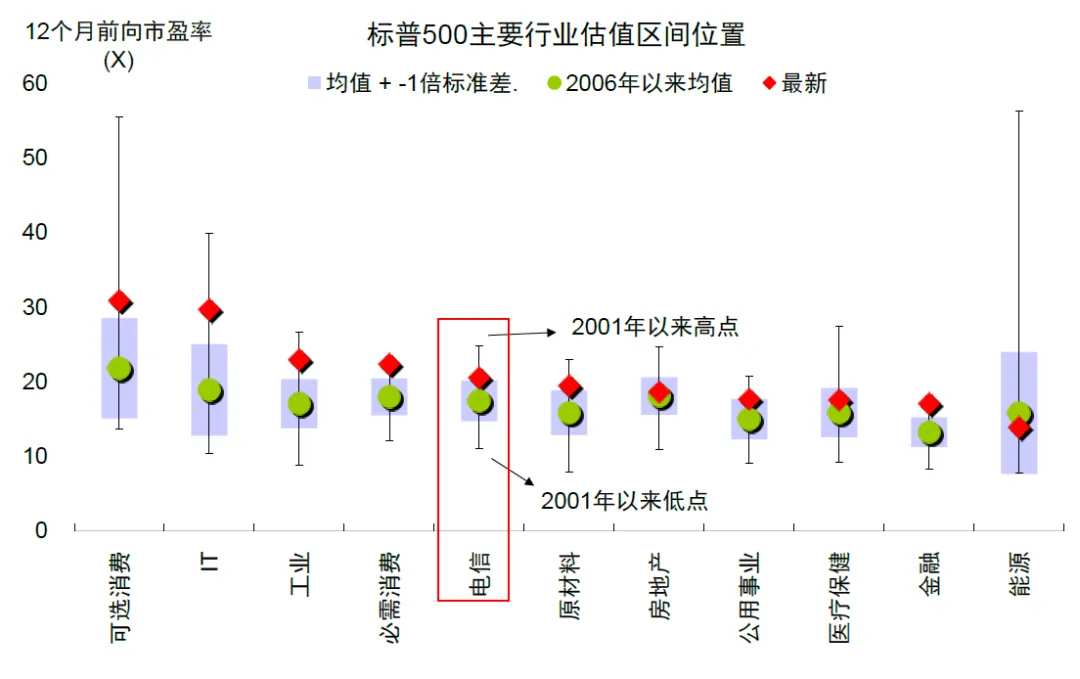

► By Sector: In the S&P 500, except for Energy, all other sectors currently have a 12-month dynamic valuation that has exceeded the mean since 2001, with Consumer Staples, Financials, and IT sectors currently above the 95th percentile, while Energy and Real Estate sectors are below the 60th percentile.

Chart: All industries in the S&P 500, except for Energy, are above the mean.

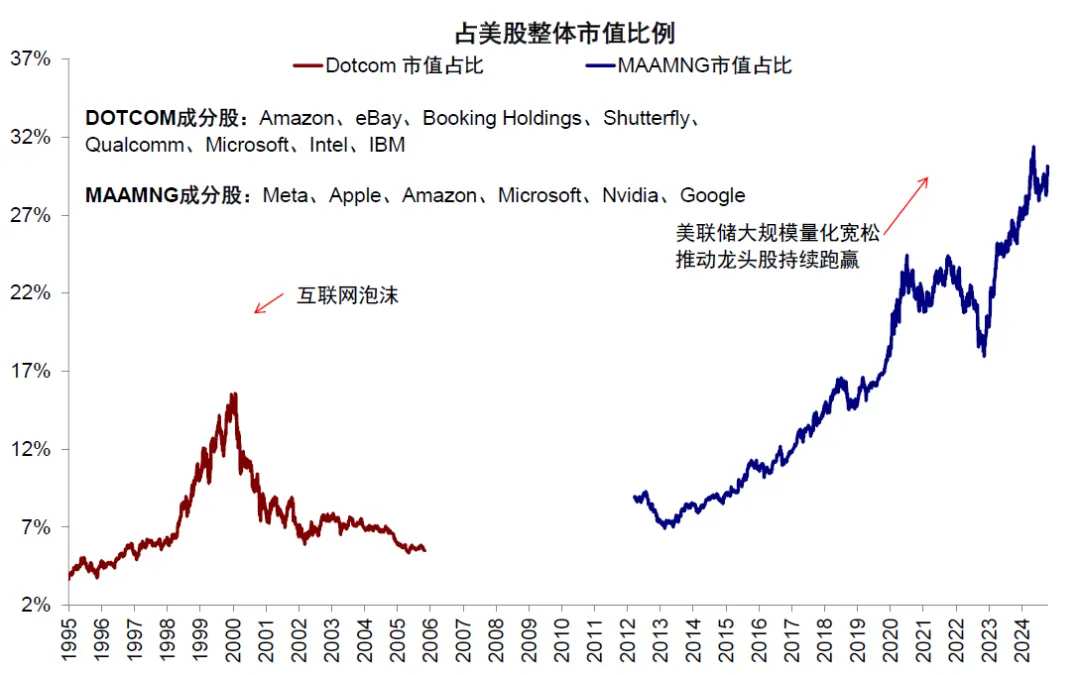

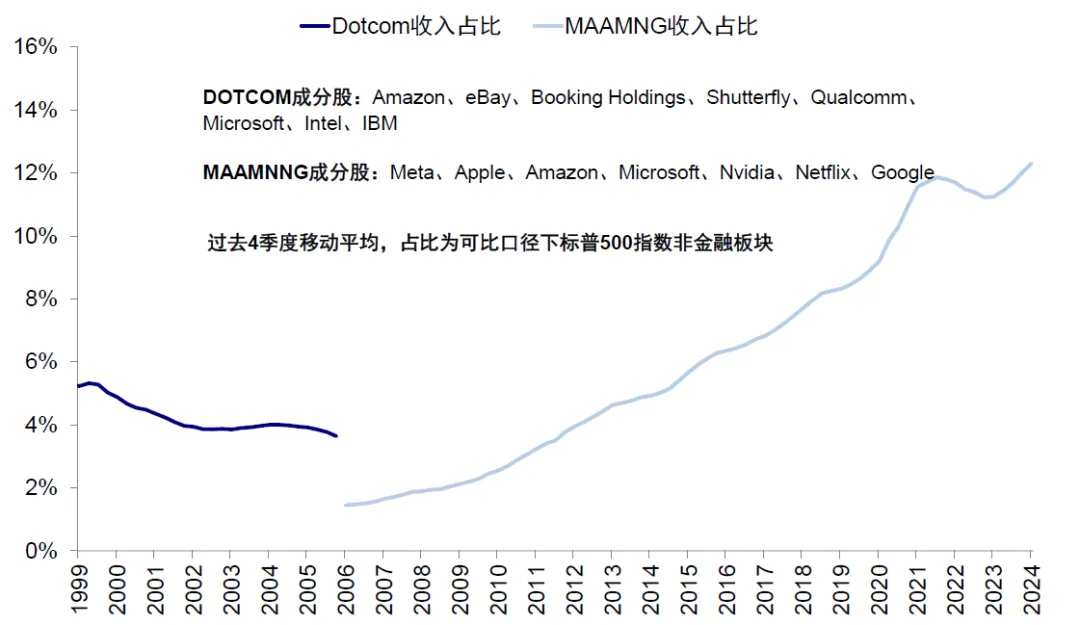

► 头部集中:当前美股头部集中效应较强,比2000年互联网科技泡沫时期市值集中度更高。从动态P/E看,MAAMNG指数为31.4倍,标普500除MAAMNG估值仅为19.6倍,标普500指数为22.6倍。美股头部科技公司(MAAMNG)市值占比达30%(vs. 互联网科技泡沫时期DOTCOM市值占比高点15.6%),但市值集中的背后有一定的收入与盈利能力支撑,科技龙头股收入、经营性现金流以及净利润占整体非金融企业可比口径的比例分别为12.3%、24.1%以及28.4%,相比互联网科技泡沫时期DOTCOM收入、经营性现金流以及净利润占比高点5.3%、9.2%和13.2%高出一倍以上。

图表:标普500除MAAMNG指数当前动态P/E为19.6倍

图表:美股头部科技公司(MAAMNG)市值占总市值比例高达30%

图表:MAAMNG收入占比为12.3%

图表:MAAMNG经营性现金流占比为24.1%

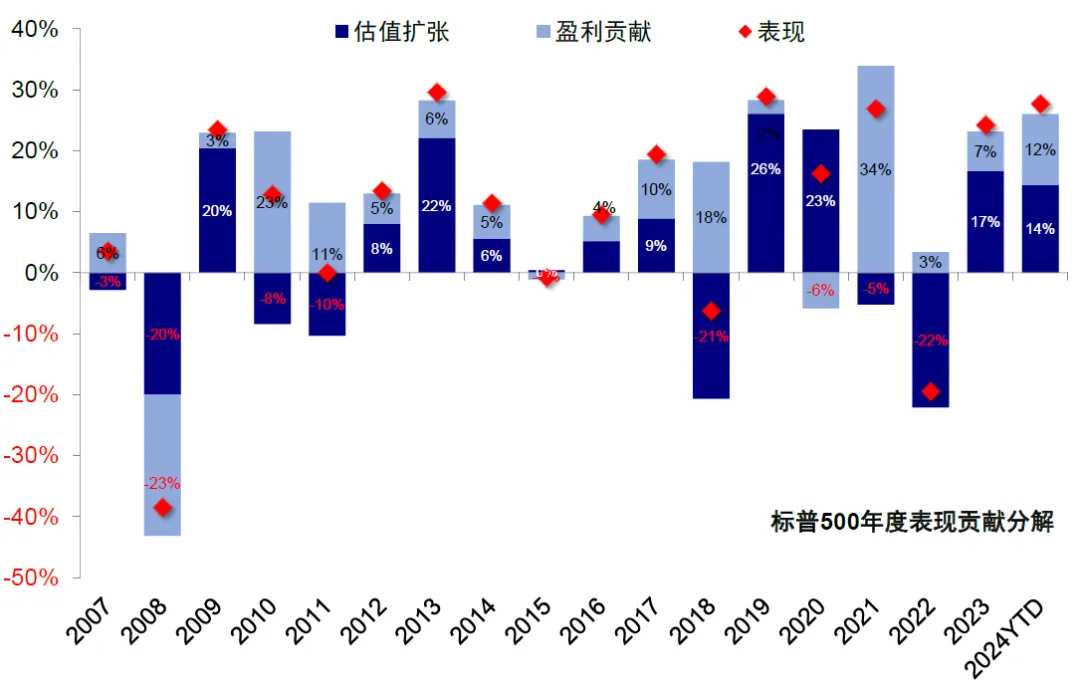

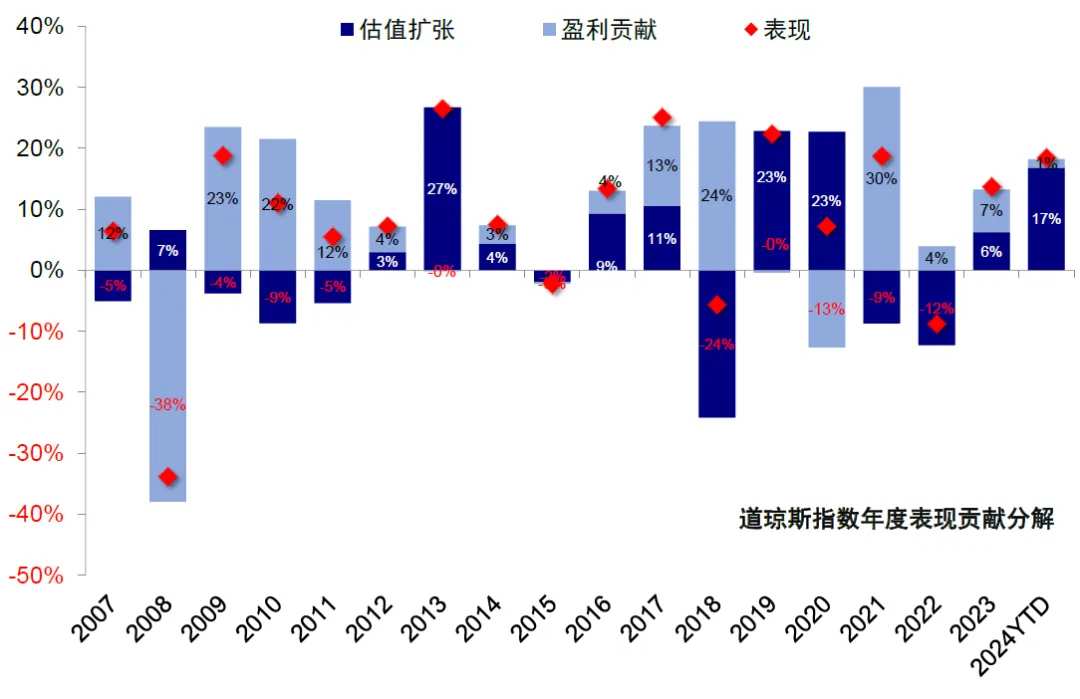

It should be noted that the valuation differences within the U.S. stock market are actually more reflective of profit differences. Dissecting the performance of U.S. stocks this year, there is a clear divergence among different style indices, with growth style driven by profits and value style driven by valuations. For example, of the Nasdaq's 31.1% increase, 21.5 percentage points were contributed by profits, making up nearly seventy percent; the profits of leading Technology stocks in the MAAMNG index contributed over seventy percent (profits 36.4% vs. increase 49.7%); in the S&P 500 Index's 26.5% increase, profits and valuations contributed equally (13.5% vs. 11.5%); while the Dow Jones saw the expansion of valuations dominate (16.1% vs. 1.2%). This is similarly reflected at the sector level, where the cyclical sectors such as energy, real estate, materials, and industrials mainly contributed through valuation expansion, while growth sectors like IT primarily contributed through profits. In terms of the driving force for valuation expansion, it mainly comes from the decline in risk premiums, with the contribution of risk-free rates being negative.

Chart: The performance contribution of cyclical sectors such as energy, real estate, materials, and industrials mainly comes from valuation expansion.

Chart: The performance of leading Technology stocks this year is primarily driven by profits, contributing over seventy percent.

Chart: In the S&P 500 Index performance this year, the contributions of valuation expansion and profits are basically equivalent.

Chart: The performance of the Dow Jones Industrial Average this year is primarily driven by valuation expansion, which has contributed almost entirely to the index's performance.

Chart: The performance of the Nasdaq this year is mainly driven by profit contributions, accounting for nearly seventy percent.

Four, evaluating a 'new perspective' on valuation: The rise in natural interest rates offsets the upward movement of actual rates, which is a core factor allowing valuations to be priced higher.

In the previous text, we compared historical levels vertically and compared other assets horizontally while decomposing the internal structure. We found that U.S. stock valuations are at a high level, but the three methods mentioned above are all 'static thinking.' If we consider the dynamic aspects of interest rates and the growth environment, especially the relative changes in costs and returns, the current U.S. stock valuations are far less extreme than they may appear.

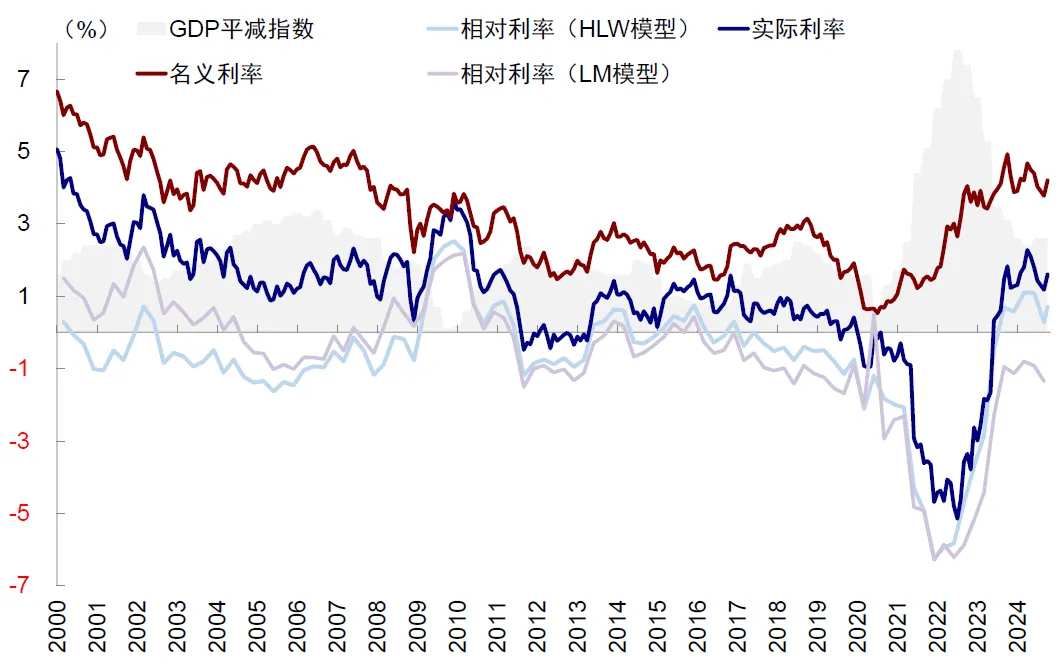

Interest rates are one of the pricing factors for risk assets. According to the DCF model, the discount cost of future cash flows includes two parts: risk-free return and risk premium. We found that using actual interest rates to explain valuation pricing is better than using nominal rates, while using relative interest rates can yield even better results. A very simple example is that if the equity risk premium (ERP) calculated using a static method is almost close to zero, it is completely unreasonable. Experience shows that the dynamic PE of the S&P 500 exhibits a more significant negative correlation with relative interest rates, indicating that relative interest rates can effectively measure funding costs and influence investors' valuation centroids for risk assets.

Chart: The trends of nominal interest rates, actual interest rates, and relative interest rates were basically consistent during the period of stable inflation levels from 2000 to 2020.

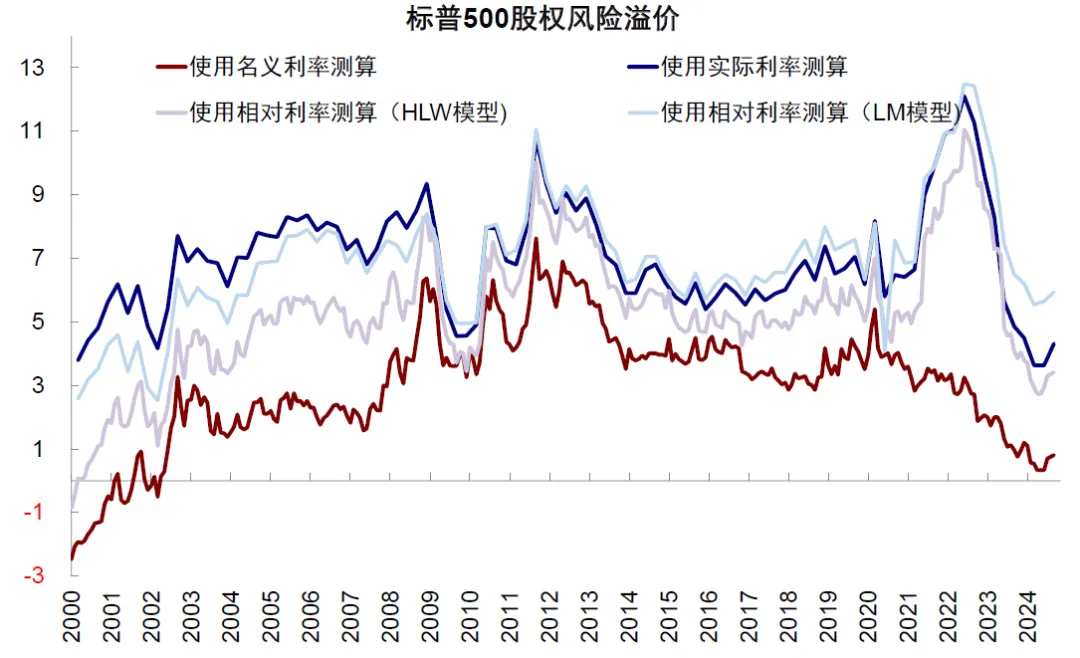

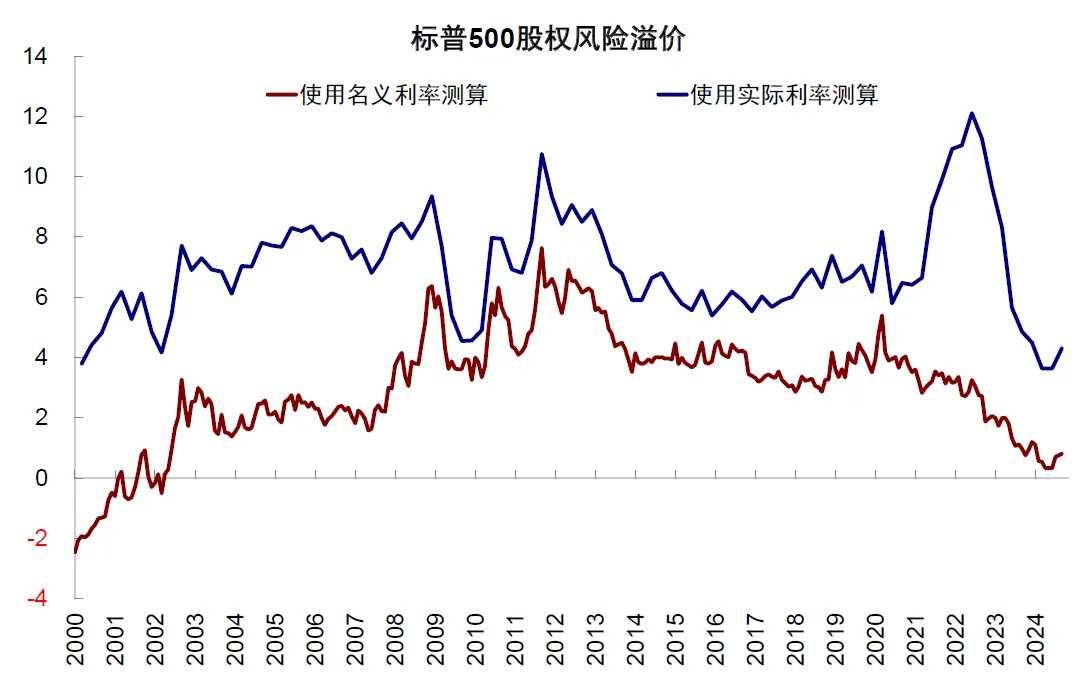

Chart: The risk premium of S&P 500 equities measured by relative interest rates has not dropped to the lowest position since 2000.

Data Source: Bloomberg, China International Capital Corporation Research Department.

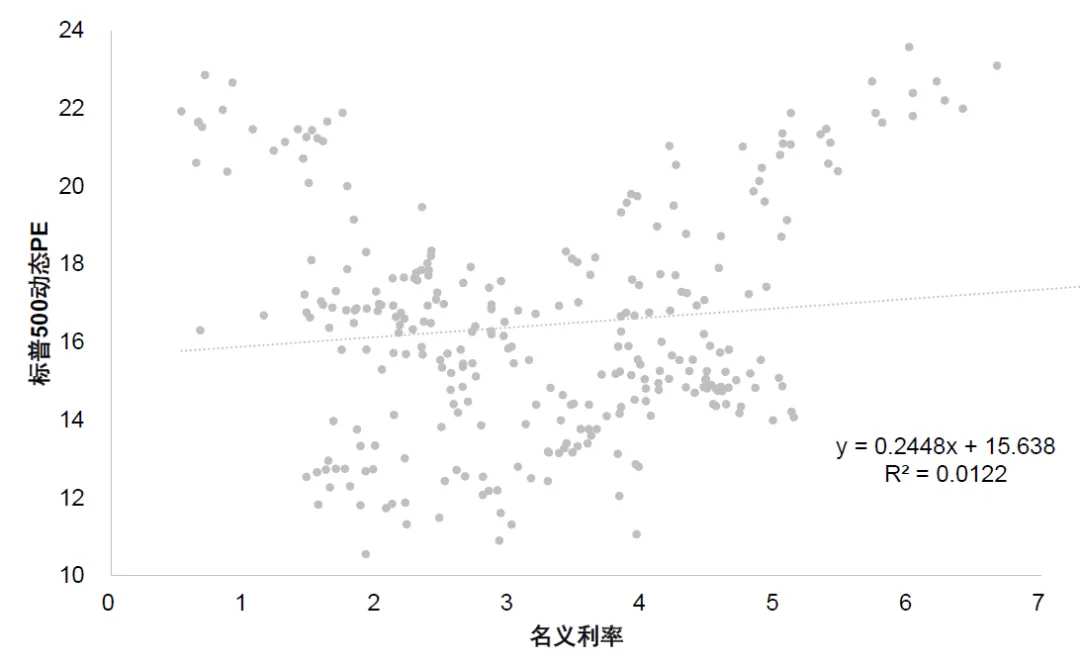

Chart: There is a positive correlation between nominal interest rates and the dynamic valuation of the S&P 500.

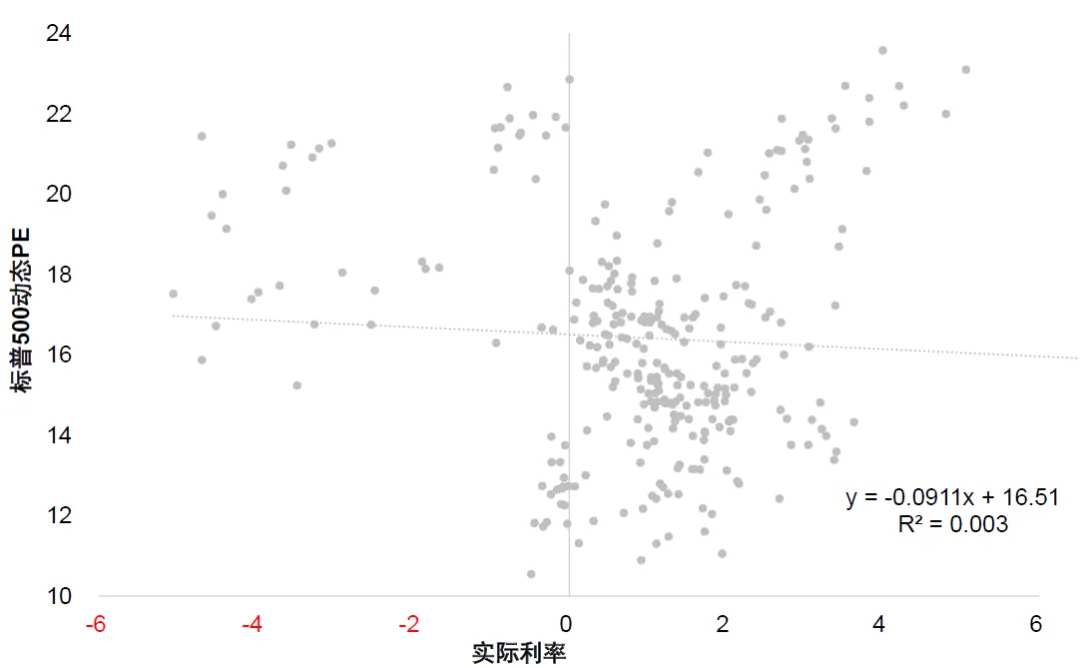

Chart: There is a negative correlation between real interest rates and the dynamic valuation of the S&P 500, but the correlation is not strong.

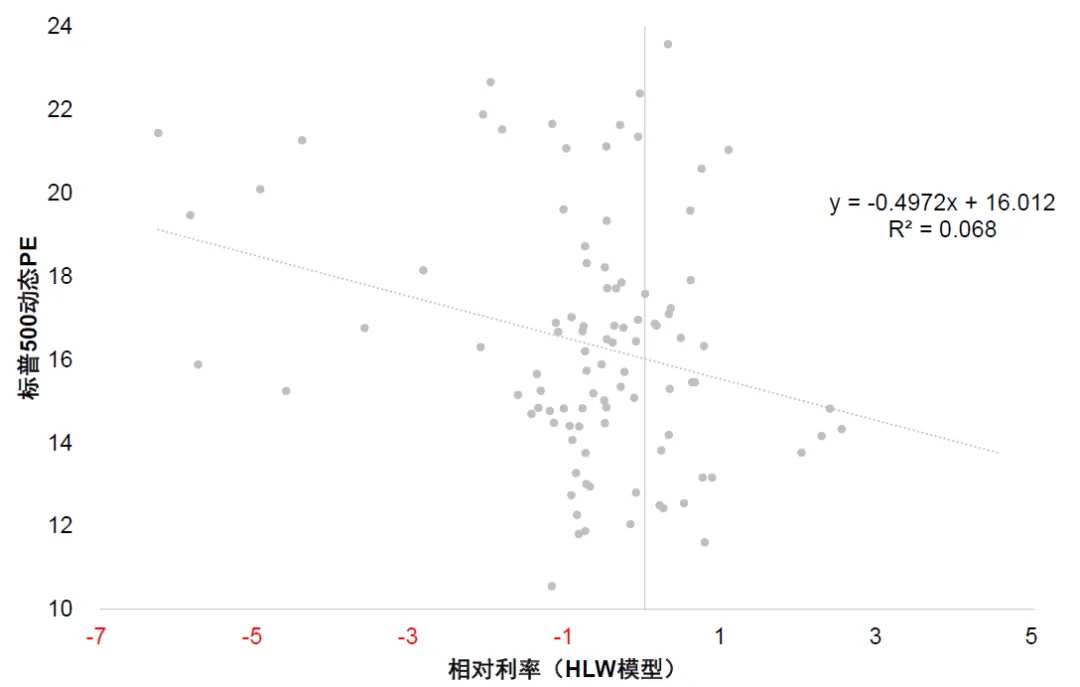

Chart: There is a negative correlation between relative interest rates (HLW model) and the dynamic valuation of the S&P 500, and the correlation is higher than that of nominal and real interest rates.

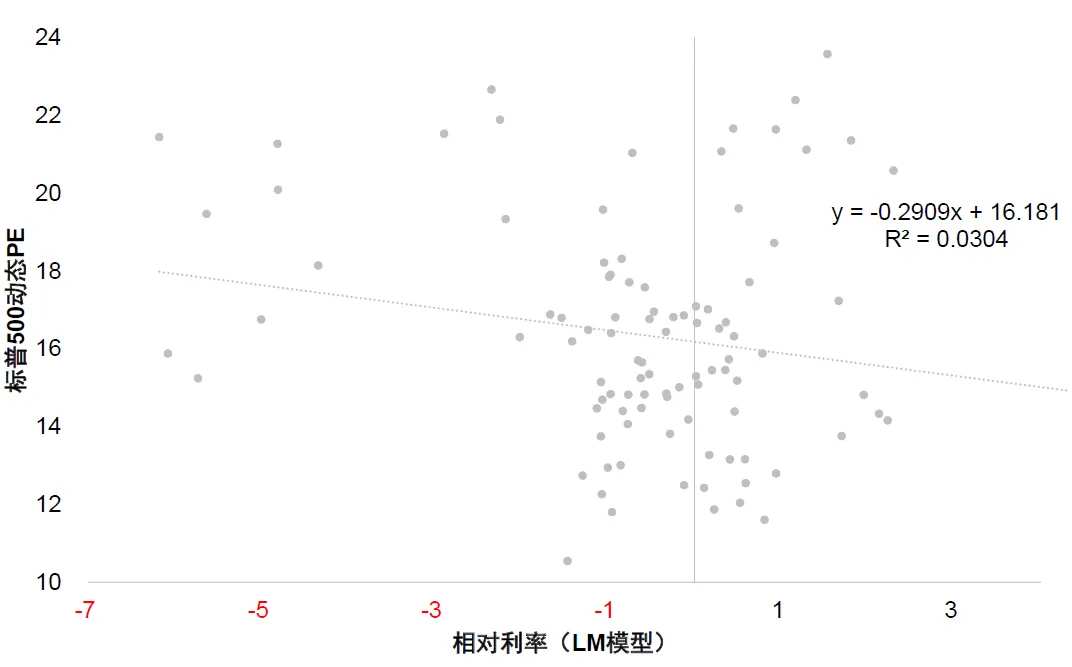

Chart: There is a negative correlation between relative interest rates (LM model) and the dynamic valuation of the S&P 500, with a higher correlation than between nominal interest rates and real interest rates.

The natural interest rate has risen rapidly in the short term (due to fiscal stimulus, AI, and other factors leading output and inflation to exceed trends), especially the gap with the real interest rate is expanding, indicating that the elevation of returns is faster than the rise in costs, which is a core factor allowing valuations to be priced higher. The estimated results of the equity risk premium show that considering the upward movement of the short-term natural interest rate, the natural interest rate calculated by the Richmond Fed LM model has risen to 2.53%, with a gap of only 0.93% from the 1.6% real interest rate, significantly offsetting the rise in the cost as a discount rate, resulting in the equity risk premium of the S&P 500 Index (measured by LM model) being 5.94%, still a considerable distance from the Internet technology revolution in 2000 (2.53%), the quantitative easing during the financial crisis in 2009 (4.96%), and the fiscal stimulus period during the COVID-19 pandemic in 2020 (4.09%), hence it does not appear extreme. Of course, if the rise in the natural interest rate is not sustainable or disproven, such as a reversal in the AI industry trend, then the valuation pricing would naturally revert to traditional static methods, making it even more 'extreme.'

Chart: The mean-reversion characteristics of equity risk premium measured by nominal interest rates and real interest rates are not significant.

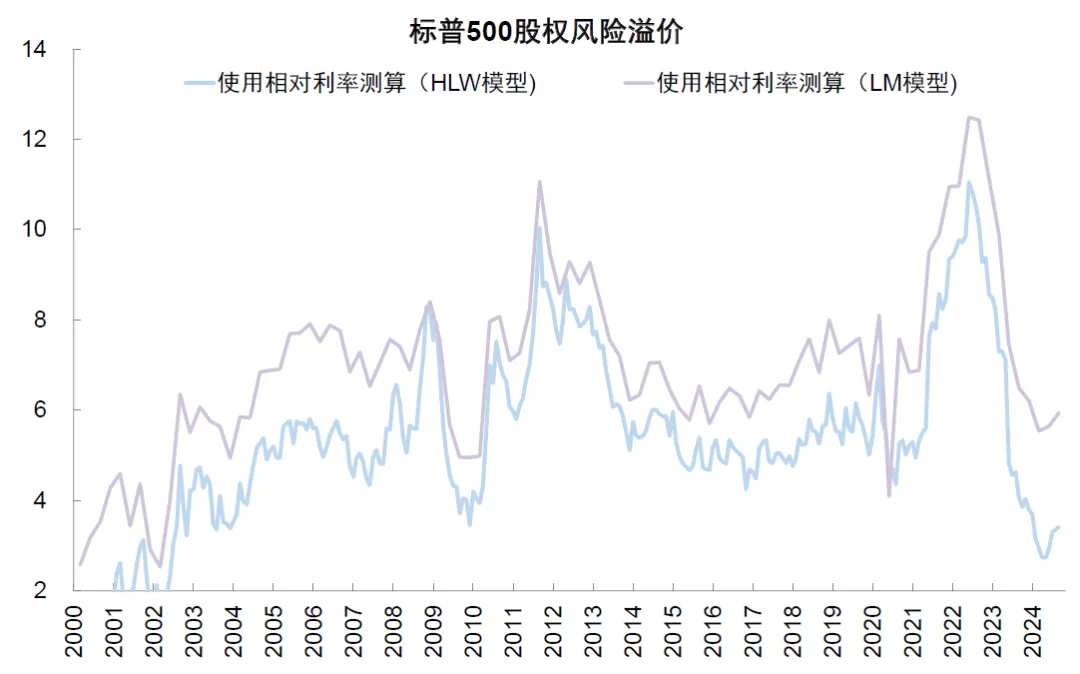

Chart: Considering the upward movement of the short-term natural interest rate, the equity risk premium (measured by LM model) has not yet fallen to historically low levels.

5. Market Space: The expansion potential for valuation is limited, and profitability is key to future trends.

The further expansion of valuation is limited. Under the current inflation situation (we estimate that inflation in the USA will bottom out in mid-2025) and interest rate reduction trajectory (we calculate that the Federal Reserve needs to cut rates 3-4 more times, with a final rate between 3.5% - 3.75%), we expect the reasonable central point for the 10-Year T-Note yield to be around 3.8% to 4%. Meanwhile, the risk premium calculated using relative rates is also at a historical low (the LM model is at the historical 30th percentile, and the HLW model is at the historical 5th percentile), leaving limited space for further decline. We estimate that dynamic valuation may slightly fall back to around 21.

Profitability is the key variable for future trends and determines the future space for the U.S. stock market. In the baseline scenario, considering the growth path of the USA itself (the economy stabilizing and recovering gradually by mid-2025) and the growth expectations for overseas revenues (30-40% of overseas income), we estimate that the profitability growth rate for U.S. stocks in 2025 may reach 10%, slightly higher than this year's 9%. Of course, in our assumptions, the AI industry's trend continues to maintain optimistic sentiment and high profitability. Meanwhile, Trump's tax reform is expected to boost U.S. profitability by 3-4 percentage points, but whether this can be reflected in 2025's profitability depends on the progress of policy promotion. Combining the aforementioned valuation estimates, we expect the S&P 500 Index to be around 6300 to 6400 ('How Much Space is Left for U.S. Stocks?'). However, if domestic demand stimulation and technology industry performance are below expectations or weaken, or if inflationary policies accelerate under Trump's administration leading to heightened concerns about stagflation, in a pessimistic scenario, we estimate the S&P 500 Index to be around 5700 to 5900 ('Path Simulation of Trump’s Policies and Trades').

编辑/jayden