The Blade Air Mobility, Inc. (NASDAQ:BLDE) share price has done very well over the last month, posting an excellent gain of 28%. The last 30 days bring the annual gain to a very sharp 26%.

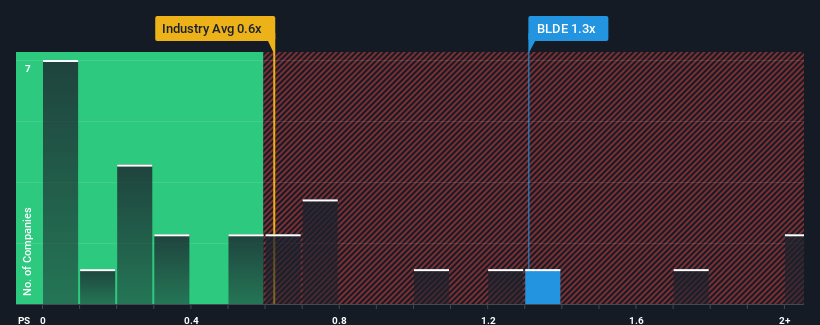

After such a large jump in price, when almost half of the companies in the United States' Airlines industry have price-to-sales ratios (or "P/S") below 0.6x, you may consider Blade Air Mobility as a stock probably not worth researching with its 1.3x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's as high as it is.

What Does Blade Air Mobility's P/S Mean For Shareholders?

Blade Air Mobility certainly has been doing a good job lately as it's been growing revenue more than most other companies. It seems that many are expecting the strong revenue performance to persist, which has raised the P/S. If not, then existing shareholders might be a little nervous about the viability of the share price.

Want the full picture on analyst estimates for the company? Then our free report on Blade Air Mobility will help you uncover what's on the horizon.How Is Blade Air Mobility's Revenue Growth Trending?

In order to justify its P/S ratio, Blade Air Mobility would need to produce impressive growth in excess of the industry.

In order to justify its P/S ratio, Blade Air Mobility would need to produce impressive growth in excess of the industry.

If we review the last year of revenue growth, the company posted a worthy increase of 12%. Spectacularly, three year revenue growth has ballooned by several orders of magnitude, even though the last 12 months were fairly tame in comparison. So we can start by confirming that the company has done a tremendous job of growing revenue over that time.

Shifting to the future, estimates from the five analysts covering the company suggest revenue should grow by 6.1% over the next year. Meanwhile, the rest of the industry is forecast to expand by 80%, which is noticeably more attractive.

With this in consideration, we believe it doesn't make sense that Blade Air Mobility's P/S is outpacing its industry peers. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. There's a good chance these shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the growth outlook.

What We Can Learn From Blade Air Mobility's P/S?

Blade Air Mobility shares have taken a big step in a northerly direction, but its P/S is elevated as a result. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've concluded that Blade Air Mobility currently trades on a much higher than expected P/S since its forecast growth is lower than the wider industry. Right now we aren't comfortable with the high P/S as the predicted future revenues aren't likely to support such positive sentiment for long. At these price levels, investors should remain cautious, particularly if things don't improve.

There are also other vital risk factors to consider before investing and we've discovered 3 warning signs for Blade Air Mobility that you should be aware of.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.