随着美联储会议的临近,大摩称,投资者关注的三个关键议题分别是:

随着美联储会议的临近,大摩称,投资者关注的三个关键议题分别是:

Due to Doves' remarks by Goolsbee hinting that the possibility of interest rate cuts may slow down in 2025, market expectations for rate cuts have tightened. Morgan Stanley believes that the market's expectations for a rate cut in January next year are relatively cautious because Goolsbee's comments were made before the inflation data was released, and the ongoing slowdown in inflation, especially housing inflation, will prompt the Federal Reserve to cut rates consecutively in the December and January meetings.

Expectations of a pause in interest rate cuts next year are rising, long-term US bonds have fallen for five consecutive weeks, experiencing the worst week this year, and the market's expectations for the Federal Reserve's future policies have become more cautious, especially regarding the pace of interest rate cuts in 2025.

On December 14, Eastern Time, Morgan Stanley released a forward-looking report indicating that the median interest rate expectation in the dot plot to be announced by the Federal Reserve this week will remain around 3.375%, which is below the market expectation range of 3.4% to 3.7%. Investors should pay attention to the downward trend in housing inflation, as the Federal Reserve may cut interest rates consecutively in December of this year and January of next year.

As the Federal Reserve meeting approaches, Morgan Stanley states that the three key issues investors focus on are: expectations for the 2025 Federal Reserve rate dot plot, Chairman Powell's statements on the pace of rate cuts, and the decision on overnight reverse repo rates.

As the Federal Reserve meeting approaches, Morgan Stanley states that the three key issues investors focus on are: expectations for the 2025 Federal Reserve rate dot plot, Chairman Powell's statements on the pace of rate cuts, and the decision on overnight reverse repo rates.

Dot plot: The median rate for next year is below market expectations.

Since the end of October, the market-implied bottom range of the Federal Reserve's policy interest rate (that is, the lowest rate expected by the market) has remained between 3.4% and 3.7%. This range is slightly higher than the median point for 2025 in the September economic forecast summary and far higher than the long-term median interest rate.

Morgan Stanley economists expect that the median interest rate expectation in the 2025 dot plot might remain around 3.375% for at least three months. This expectation is lower than the initial lower limit of the market's expected range.

Therefore, the market will view this as a signal of a more accommodative monetary policy, and expectations for interest rates (the market-implied bottom range) may temporarily decrease. This change may receive further confirmation after the dot plot is released and before the press conference.

Powell's press conference: The market has overinterpreted cautious remarks.

After investors digest the FOMC statement and dot plot, attention will shift to Chairman Powell's press conference. Most investors expect Powell to imply that the pace of interest rate cuts will slow down in 2025 while retaining the usual language of 'data dependence', meaning future policy will be determined based on changes in economic data.

Morgan Stanley points out that most investors believe Powell's cautious signals suggest that there may not be a rapid interest rate cut in January next year. Although they understand that policy will change based on economic data, they often overinterpret Powell's hints and may make overly aggressive expectations about interest rate cuts in January 2025, ignoring the uncertainty of 'data dependence'.

The market's reaction can be seen from the two previously released 'good' inflation reports (CPI and PPI). The market's response to the latest inflation data has been relatively indifferent, stemming from investors still being entangled in the previous comments from USA Federal Reserve officials.

For example, next year's voting committee member, dovish figure, and president of the Chicago Federal Reserve, Goolsbee, has frequently stated that as interest rates approach the 'neutral rate', the pace of rate cuts should slow down because the impact of monetary policy on the economy is lagging.

However, at the Chicago Fed's annual economic outlook seminar on December 6, Goolsbee's remarks showed a subtle change. Media reports indicated that he hinted at a series of 'hard-to-decide' meetings in the future, but he believes that interest rates still need to be 'significantly lowered'. At the same time, there are reports that he thinks the pace of interest rate cuts may slow down next year.

This viewpoint has drawn widespread attention from the market, as he is one of the more dovish officials within the Federal Reserve. If such a dovish Federal Reserve official suggests that the pace of rate cuts may slow down next year, investors will naturally interpret the risks as leaning in that direction, anticipating that future rate cuts will be more cautious and slower.

However, Morgan Stanley points out that Goolsbee's last public appearance was before the relatively mild inflation data was released in November, and his views may not fully account for the latest inflation data. Other Federal Reserve officials, such as the comments from Fed Governor Waller in September, indicate that inflation remains a key factor in decision-making.

Waller stated that if economic data continues to be weak, he would be more inclined to adopt more aggressive rate cuts to bring inflation closer to the Federal Reserve's target.

Morgan Stanley noted that if Federal Reserve Chairman Powell does not suggest a slowdown in the rate-cutting pace at least in early meetings of 2025 during the press conference, investors might feel more confident that the probability of a rate cut in January is higher.

Inflation is a key factor: housing inflation will continue to slow down.

Morgan Stanley previously pointed out that due to the decline in housing inflation in the November CPI report, market expectations for a Federal Reserve rate cut in January have increased.

Specifically, the strong performance of core Commodity prices reflects the impact of hurricanes (considered 'noise' in the short term), while the slowdown in rent and owner-equivalent rent (viewed as a 'signal') indicates a downward trend in housing inflation, which brings optimism to the market.

Waller mentioned in an interview after the September meeting that the pace of inflation decline was faster than he expected, which is one reason supporting larger rate cuts. Waller and his team did a simple calculation, stating that if housing inflation grows at an annualized rate of 2% and this rate continues monthly, the core PCE inflation rate would have been below 1% over the past four months.

At the same time, Morgan Stanley economists' forecasts for housing inflation also support this view, as they predict that the housing services inflation rate in the core PCE will be 0.24% monthly. This suggests that housing inflation will continue to slow down in the coming months, providing the Federal Reserve with greater confidence that the trend of declining inflation remains unchanged, allowing the Federal Reserve to cut rates consecutively in the next two policy meetings.

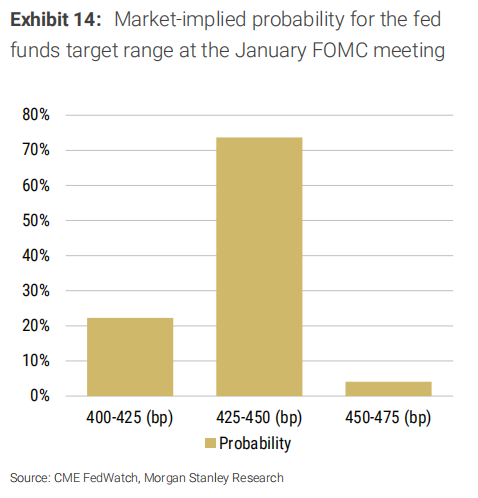

Therefore, considering the latest changes in inflation data, Morgan Stanley stated that current market expectations may underestimate the likelihood of a rate cut in January. Present market pricing indicates that the likelihood of another rate cut in January next year is relatively low, with a probability of about 25%.

Get a sneak peek at important financial events, discover investment opportunities early! Open futubull> Market> USA Stock>Financial Calendar/Selected macroeconomic data, seize the investment opportunities first!

Editor/Rocky