作为行业老二,荣业食品亦不乏一些成长隐忧。

作为行业老二,荣业食品亦不乏一些成长隐忧。How to demonstrate its growth potential to the market has become a pressing issue for Rongye Foods.

After going public, Rongye Foods (WYHG.US) seems to have not gained more favor in the Capital Markets. As of the closing on December 11, the stock fell over 10% during the week, and the price is close to the offering price of 4 dollars.

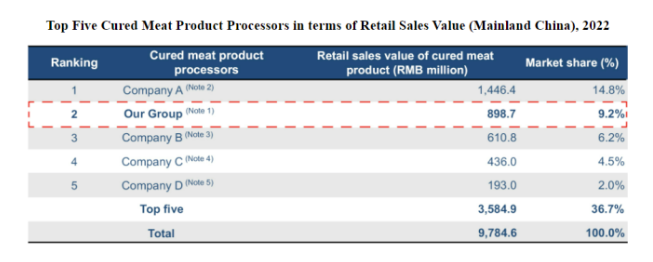

According to a report by Frost & Sullivan, in the fiscal year 2022, based on the retail sales of cured meat products in Mainland China, Rongye Foods ranked second with a market share of 9.2%. According to Rongye Foods, the market concentration of cured products in Mainland China is relatively high, with the top five processors occupying 36.7% of the market share. Among them, Rongye Foods differs by 5.6 percentage points from the company with the first market share, with retail sales of cured meat products differing by 0.548 billion yuan.

As the second in the Industry, Rongye Foods also has some growth concerns.

As the second in the Industry, Rongye Foods also has some growth concerns.

Revenue growth has slowed, with the main Revenue from cured meat products declining.

It is reported that Rongye Foods can be traced back to 1915, enduring four generations, and has a history of over a hundred years. At that time, the company mainly processed and sold cured sausages under the name 'Rongye'. Since 2010, the company has begun its Operation through Rongye Guangdong, continuously developing its Business and building its brand. In addition to 'Rongye', Rongye Foods has also developed snack product brands 'Craft King' and 'Crazy Customer'.

In terms of performance, from 2022 to September 30, 2023, and 2024 (hereinafter referred to as the reporting period), Rongye Food's revenue was 0.131 billion USD, 0.134 billion USD, and 0.105 billion USD respectively; the net income was 11.19398 million USD, 14.0099 million USD, and 11.02 million USD respectively. The revenue growth in 2023 was only 2.29% year-on-year, while net income grew 25.16% year-on-year. It is not difficult to see that the company's revenue growth rate is actually slowing down.

In addition, the company's profit growth rate also seems to have slowed. In 2022 and 2023, the company's gross margin was 44.34 million USD and 47.1 million USD, with a year-on-year increase of 6.22%; the gross margin rate was 33.91% and 35.13%, with an increase of less than 2 percentage points year-on-year.

Rongye Food's revenue mainly comes from the sales of preserved meat products, snack products, and frozen meat products. During the reporting period, the revenue from preserved meat products accounted for 67.58%, 62.11%, and 57.93% respectively. Among them, the revenue from pork sausages accounted for 40.86%, 36.24%, and 36.87% respectively, with gross margins of 30.98%, 33.03%, and 37.23%; the revenue from preserved pork accounted for 14.64%, 16.39%, and 13.04% respectively, with gross margins of 40.29%, 39.71%, and 39.07%.

In addition, the revenue from snack products accounted for 27.45%, 32.55%, and 36.75%, with gross margins of 34.86%, 35.78%, and 26.37%; the revenue from frozen meat products accounted for 4.96%, 5.34%, and 5.32%, with gross margins of 40.75%, 43.22%, and 41.99%.

It can be seen that preserved meat products are Rongye Food's primary products. However, in the first half of 2024, the sales revenue of preserved meat products decreased by 4.61 million USD. Rongye Food pointed out that the decrease in revenue from preserved meat products was mainly due to the average unit selling price falling from 8.53 USD per kilogram to 8.16 USD per kilogram, resulting in a revenue decrease of 2.1 million USD; sales volume dropped from 5739 tons to 5628 tons, leading to a revenue decrease of 0.91 million USD, as well as the impact of exchange rate fluctuations applicable to business reports.

From the above data performance, it is not difficult to see that as a 'time-honored' cured meat enterprise, Rongye Food inevitably encounters a bottleneck in growth.

The increasing sales expenses are still difficult to translate into performance growth, and there is no shortage of operational pressure under the "blueprint".

Through the above analysis, the development path of Rongye Foods has become very clear. While deeply cultivating its core business of Cantonese cured meat products, it is also expanding new product lines to create a diversified product matrix and increasing sales channels to accelerate market penetration.

From an industry perspective, Rongye Foods will benefit from the sustained growth of market demand. According to Frost & Sullivan data, from 2022 to 2027, the market size of cured meat products in mainland China will increase from 52.9 billion RMB to 73.9 billion RMB, with a compound annual growth rate of 6.9%. During the same period, the compound annual growth rates for leisure snacks and frozen meat products are 8.3% and 4.5%, respectively.

The cured meat product market is a part of the cured meat product market, with its retail sales accounting for 18.5% of the entire cured meat product market in 2022. Moreover, within the cured meat product market, the compound annual growth rate of the cured meat product submarket was the highest from 2018 to 2022. According to Frost & Sullivan data, cured meat products have a wide range of applications in various dining options and cooking methods, and are expected to maintain a compound annual growth rate of 8.5% from 2022 to 2027.

While the industry shows significant development potential, Rongye Foods also stands at the forefront of the industry thanks to years of accumulation, forming a certain scale effect.

It is worth noting that Rongye Foods' expenditure on sales expenses should not be overlooked. During the reporting period, the company's sales expenses were 19.6917 million USD (approximately 0.138 billion RMB), 19.5506 million USD, and 9.9698 million USD, a year-on-year growth of -0.72%, 36.38%, accounting for 15.06%, 14.58%, and 14.53% of revenue, respectively.

Rongye Foods pointed out that sales expenses mainly include advertising costs; salaries and commissions for sales and marketing personnel; transportation and delivery fees for e-commerce platforms; space occupancy costs, such as supermarket counters; and service fees for e-commerce platforms like TikTok, JD.com, and PDD Holdings. For the significant increase in sales expenses in the first half of 2024, Rongye Foods indicated that it was mainly due to an increase in advertising costs of 2.81 million USD.

However, as mentioned above, the sales volume and unit price of the company's cured meat products have both decreased. It is evident that despite the continuous rise in selling expenses, it is still difficult to reverse the decline of the company's Block Orders products, indicating existing Operational pressure.

In addition, as the "second in the Industry," Rongye Foods is susceptible to pressure from leading companies. According to the prospectus, the market share of the industry leader in retail sales of cured meat products reaches as high as 14.8%. Although Rongye Foods follows closely, there is a gap of 5.6% in market share; on the other hand, the entry threshold for cured meat products is not high, making it easy for the company to be bullied by "latecomer" companies vying for market share.

In response, Rongye Foods also indicated risks in the prospectus that the meat processing Industry in mainland China is highly competitive. Whether in the procurement of raw meat, processing technology, or sales of processed meat products, there is competition. Additionally, the company also faces competition from several meat processing enterprises in mainland China, some of which may possess more financial and other resources. If the company cannot effectively compete with these companies, it may adversely affect its market share and profitability.

In summary, Rongye Foods' move to the United States undoubtedly adds some chances for it to break the impasse, but it seems that investors are not easily convinced. Under the pressure of declining performance of its Block Orders products, how Rongye Foods demonstrates its growth potential to the market remains an open question.