历经十余年的发展后,目前卓越睿新在国内高等教育教学数字化市场所有公司中收入位列第二,2023年市场份额约为3.4%;而在国内高教数字化教学内容制作市场中,公司的规模已无出其右者,2023年的市场份额约为6.2%。

历经十余年的发展后,目前卓越睿新在国内高等教育教学数字化市场所有公司中收入位列第二,2023年市场份额约为3.4%;而在国内高教数字化教学内容制作市场中,公司的规模已无出其右者,2023年的市场份额约为6.2%。After three years of unsuccessful attempts to enter the A-share market, the company, supported by Sina and Baidu, is now vigorously moving to the Hong Kong stock market...

Shanghai Zhuoyue Ruixin Digital Technology Co., Ltd. (hereinafter referred to as 'Zhuoyue Ruixin'), which has been deeply involved in the digitalization of higher education for more than a decade, has recently launched another 'sprint' towards the Hong Kong Stock Exchange.

Recently, Zhuoyue Ruixin submitted a listing application to the Main Board of the Hong Kong Stock Exchange again. Looking back, Zhuoyue Ruixin was established in 2008 and launched the brand 'Wisdom Tree' in 2013. In 2016, Zhuoyue Ruixin received investments from Sina and other investors.

After more than a decade of development, Zhuoyue Ruixin currently ranks second in terms of revenue among all companies in the domestic higher education teaching digitalization market, with a market share of approximately 3.4% in 2023. In the market for digital teaching content production in domestic higher education, the company's scale is unmatched, with a market share of approximately 6.2% in 2023.

After more than a decade of development, Zhuoyue Ruixin currently ranks second in terms of revenue among all companies in the domestic higher education teaching digitalization market, with a market share of approximately 3.4% in 2023. In the market for digital teaching content production in domestic higher education, the company's scale is unmatched, with a market share of approximately 6.2% in 2023.

Although the 'status' in the industry is evidently significant, if one judges through financial data, Zhuoyue Ruixin seems to have vulnerabilities. According to Zhito Finance APP, in recent years, Zhuoyue Ruixin's performance has been unstable, particularly with significant fluctuations in profitability. This is certainly not a 'plus' for Zhuoyue Ruixin, which aims to go public in Hong Kong.

Additionally, it is worth mentioning that Zhuoyue Ruixin has also explored opportunities for listing in China's A-share market. Rewind to January 2021, when the company began accepting guidance for A-share listing. However, after three years of waiting, Zhuoyue Ruixin eventually terminated the guidance agreement in April this year and quickly turned to the Hong Kong stock market. However, after submitting the materials for the first time in May, the company did not make further progress.

The stability of performance still needs to be strengthened.

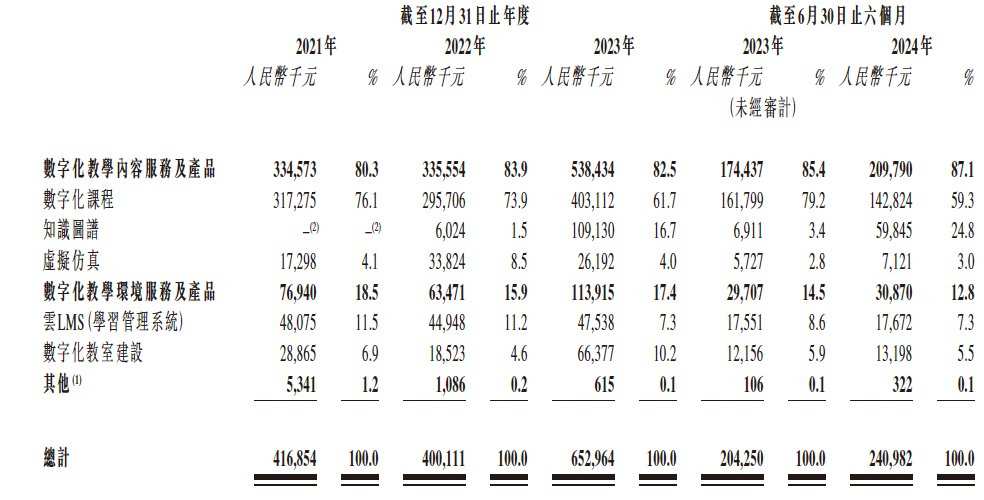

The performance of Excellence and Wisdom, a provider of digital teaching solutions for universities in China, is primarily supported by two major Businesses: digital teaching content services and products, as well as digital teaching environment services and products. Unlike the primarily B2C business model, Excellence and Wisdom’s clients are mainly higher education institutions, including various universities, colleges, and vocational schools. According to the prospectus, from 2021 to the first half of 2024, Excellence and Wisdom developed over 33,000 digital courses.

With scale advantages and first-mover advantages, Excellence and Wisdom's scale has shown a spiral upward trend. From 2021 to 2023, the company's revenues were 0.417 billion yuan, 0.4 billion yuan, and 0.653 billion yuan, respectively. In the first half of this year, the company achieved revenue of 0.241 billion yuan, representing an 18% year-on-year growth.

Looking at the revenue structure, digital teaching content services and products are the main source of income for Excellence and Wisdom. During the reporting period, this Business accounted for 80.3%, 83.9%, 82.5%, and 87.1% of the company's total revenue, respectively. It is reported that Excellence and Wisdom launched virtual simulation development as early as 2020 and introduced knowledge graph development last year. Currently, the company’s digital teaching content services and products cover 12 disciplines and 92 majors recognized by the Ministry of Education.

During the reporting period, the digital teaching environment services and products Business accounted for 18.5%, 15.9%, 17.4%, and 12.8% of Excellence and Wisdom’s revenue, respectively. This Business aims to assist higher education institutions in establishing efficient and integrated digital environments (including online and offline).

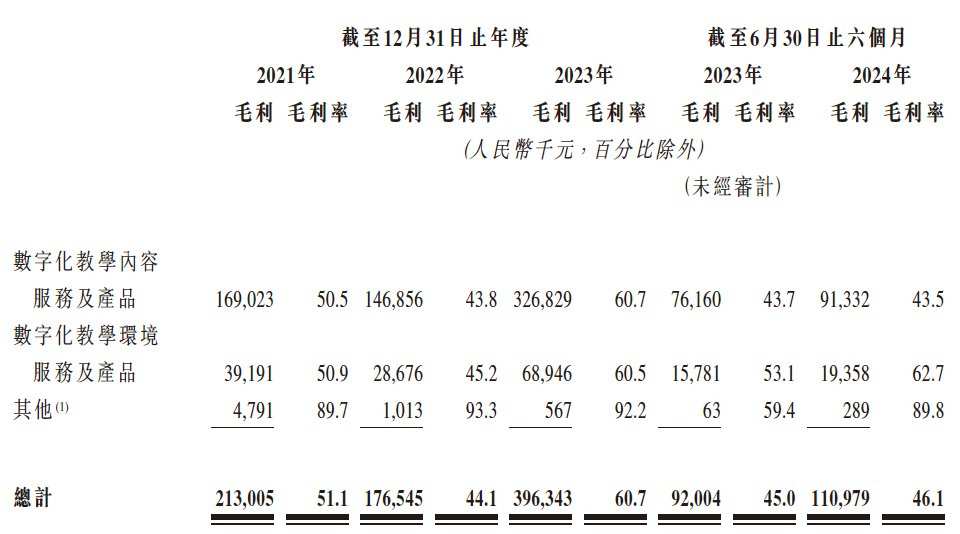

It is worth noting that during the process of a spiral rise in revenue, Excellence and Wisdom's profitability has fluctuated much more dramatically. From 2021 to the first half of 2024, the company's gross margin was 0.213 billion yuan, 0.177 billion yuan, 0.396 billion yuan, and 0.111 billion yuan, corresponding to gross margins of 51.1%, 44.1%, 60.7%, and 46.1%, respectively. During the same period, the company's Net income was 33.74 million yuan, -59.11 million yuan, 81.421 million yuan, and -88.855 million yuan.

In the first half of this year, Excellence and Wisdom’s gross margin recorded a significant pullback compared to the full-year level of 2023, along with substantial Net income losses. This is mainly due to the seasonal patterns in the industry, as the income recognized and services and products delivered by the company in the first half of the year are often less, which can periodically affect profitability.

However, even setting aside the semi-annual data, the profit Indicators of Zhouyue Ruixin in 2022 were also disappointing. It is reported that this was mainly due to the business interruptions caused by the pandemic at that time, as well as increased expenditures in R&D and sales which somewhat eroded profits.

Do the large Internet Plus-Related companies provide enough support for growth?

As mentioned earlier, as early as 2016, Zhouyue Ruixin received investments from external investment institutions including Sina. In fact, reviewing the company's current equity structure, it is not difficult to find that besides Sina, well-known companies like Baidu also back Zhouyue Ruixin.

Successfully attracting investments from a number of large Internet Plus-Related companies is certainly due to Zhouyue Ruixin's own competitive advantages, but may also be related to the high growth potential of the Industry in which it operates. According to Frost & Sullivan's data, the scale of China's higher education digital teaching market grew from 11.1 billion yuan in 2019 to 19.3 billion yuan in 2023, with a compound annual growth rate of 14.8%. It is expected to reach 40 billion yuan by 2028, with a compound annual growth rate of 15.7% from 2023 to 2028.

With strong growth momentum in the Industry, can Zhouyue Ruixin definitely run with "accelerated growth"? The answer may not be so straightforward. Currently, the application of cutting-edge technologies such as AI, virtual simulation, audiovisual, and data security is reshaping higher education, particularly under the influence of breakthrough technologies like AI, the trend of digital intelligence in the Industry is intensifying. Although new technologies can stimulate healthy growth in the Industry, the intensity of competition among peers may also rise accordingly, leading to significant uncertainty in the competitive landscape of the market in the long term.

At this stage, the higher education digital teaching market remains highly fragmented. Public data shows that the combined market share of the top five companies in the Industry in 2023 is less than 15%. Among these top five companies, two are already listed on the Hong Kong stock market. With peers ahead, for the equally ranked Zhouyue Ruixin in the top five, seeking to quickly land on the Hong Kong stock market to explore financing opportunities in international markets would obviously be beneficial for further expanding its influence.

此外,从自身财务状况看,卓越睿新对于资金的“饥渴”程度亦不低。截至2021年-2024年上半年各期末,公司账上现金及现金等价物分别为97.432 million元、0.206 billion元、0.142 billion元、67.719 million元;同期,公司的贸易应收帐款及留置金应收账款分别为0.128 billion元、0.141 billion元、0.215 billion元、0.269 billion元。综合来看,卓越睿新的商业模式便几乎决定了其若想做大做强,势必需要不断借助外部力量来为其提供“子弹”,进而为公司的扩张提供支撑。

由此也不难理解,在冲击A股未果后,纵有新浪、百度“撑腰”,卓越睿新仍要马不停蹄转战港股。不过考虑到当前市场环境下各路投资者对投资标的越发挑剔,卓越睿新若不能提升自身业绩的确定性和稳定性,那想要打动市场恐怕也并非易事罢。